FX News Today

- EU to give Johnson one week to improve Brexit proposal. According to a Bloomberg, the EU’s chief negotiator Barnier told a private meeting of European senior diplomats that Boris Johnson’s latest blueprint for the Irish border fell far short of his conditions for a deal. The U.K. was given a week to improve on the plans.

- European Outlook: Bund futures are fractionally higher ahead of the official open in Europe while Treasuries held yesterday’s gains. EGBs bounced back yesterday but the combined sell off in Gilts and FTSE 100 especially on Wednesday highlights that Brexit risks also raise stagflation concerns and has the potential to send all U.K. assets lower. DAX and FTSE 100 futures are higher, with the DAX future underperforming slightly, as the main index returns from yesterday’s holiday. EUR-USD is trading at 1.0969 as markets look ahead to the U.S. payroll report today, which will dominate the session, especially amid the lack of data releases in Europe.

Charts of the day

Technician’s Corner

- EURUSD opened the session at lows near 1.0950, and was steady into the U.S. services ISM. From there, a three-year low outcome saw the pairing vault to 1.0999 highs, as the Dollar overall, and Treasury yields headed lower. The pairing steadied between the highs and 1.0975 through the remainder of the session. Major Dollar pairings are liable to turn sideways through the overnight session, as traders anticipate the U.S. employment report on Friday. The jobs report may go some way in solidifying the growth outlook and the Fed’s policy path, and hence, future USD direction.

- USDJPY bounced from near one-month lows of 106.87 seen into the N.Y. open, topping at 107.12 into the ISM data. The pairing slid to new trend lows of 106.48 after the data, taking its cue from a sharply lower Wall Street and a dive in Treasury yields. Heightened odds for another Fed rate cut at the end of October will likely keep a cap on the pairing for the time being.

Main Macro Events Today

- U.S. Employment Preview: It’s all about the September employment report. The data will go some way in solidifying the markets’ growth outlook and the Fed’s policy path after a rash of weaker than expected numbers on manufacturing and services fueled worries over a recession. But the markets have already priced in a Fed rate cut at the October 29, 30 FOMC, so this report isn’t likely to alter that outlook measurably. Expectations are for a 145k rise in non-farm payrolls, versus the previous 130k, though recent data suggests downside risks. Hourly earnings are seen rising 0.3% from 0.4% in August, while the unemployment rate should dip a tenth to 3.6% (lowest since the 3.5% for December 1969).

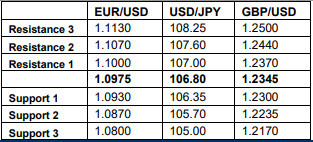

Support and Resistance levels

Click here to access the Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.