FX News Today

- FOMC minutes did not provide strong clues on the direction of rates.

- However, the lack of a signal that the Fed’s July rate cut was the start of an easing cycle was enough to eventually weigh on Treasuries.

- Asian stock markets struggled as investors continued to digest the implications of yesterday’s Fed minutes and trading conditions remained quieter than usual ahead of Powell’s speech at Jackson Hole tomorrow.

- Yields closed at their highs of the session after holding cheap levels all session. The curve narrowed below 1 bp as the short end underperformed.

- US President Trump continued to criticize the Fed Chairman, while suggesting the US may strike a deal on trade, but that didn’t prevent US futures from heading south overnight.

- Topix and Nikkei are currently down -0.13% and -0.09% respectively, despite improvements in PMI readings that were counterbalanced by an as expected decline in the All Industry Index.

- The WTI future meanwhile fell back to $55.45 per barrel.

- Brexit: Merkel gives Johnson 30 days to solve Backstop conundrum.

- Johnson is today expected in Paris, where the tone is likely to be harsher than in Berlin, although both Merkel and Macron have stressed that they are ready for a no-deal Brexit if there is no agreement.

- The UK curve remains inverted out to the 10-year area.

Charts of the Day

Technician’s Corner

- USDJPY printed a two-day low, at 106.28.The biggest mover, not surprisingly, has been AUDJPY, a forex market barometer of shifting risk-appetite patterns in global markets. The cross was showing a 0.5% loss heading into the London interbank open, and was testing one-week lows at 71.90. Next Support stands at 71.76 and 71.60. Resistance is at the pivot 72.20 level.

Main Macro Events Today

- Jackson Hole Symposium – Day 1

- Services and Manufacturing PMI (EUR, GMT 07:30-08:00) – July PMI readings highlighted manufacturing weakness. This picture is likely to be seen again in the preliminary readings for August, as Manufacturing PMI has been forecast at 46.3 from 46.5 last month, still down from 47.6 in June, and indicates a deepening recession in a sector that has been hit very hard by global trade tensions and no-deal Brexit risks. Meanwhile, Services PMI is expected to fall to 52.7 from 53.2.

- Services and Manufacturing PMI (USD, GMT 13:45) – Preliminary Manufacturing is expected to grow in August, to 51.0 from 50.4, as Services PMI is likely to fall to 51.7 from 53.

- New Zealand Retail Sales (NZD, GMT 22:45) – Usually considered an index of consumer confidence and overall consumption in the economy, higher retail sales point to higher consumption and hence higher economic growth which is good for the currency.

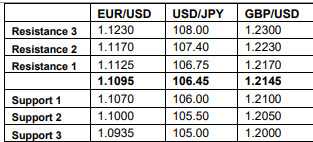

Support and Resistance levels

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.