Gold price surge fuelled by macro forces

The macroeconomic backdrop suggests that central banks are preparing to ease monetary policy further, due to weakening consumer prices and slowing economic growth. Gold prices are inversely correlated with the value of the US dollar and interest rates.

Gold prices rose past $2,600 per ounce last Friday, reaching a new record high, as expectations of interest rate cuts and rising geopolitical tensions boosted the precious metal’s appeal. The Fed implemented its first rate cut since the start of 2020 on Wednesday, with a 50 bps reduction to 5%, while Fed officials projected that the benchmark rate will drop another half percentage point by the end of the year. Meanwhile, gold’s status as a safe haven asset has been further strengthened by rising tensions in the Middle East.

Hezbollah Deputy Secretary-General Naim Qassem said on Sunday, during the funeral of a top commander killed in an Israeli raid in Beirut on Friday, that the organisation has entered a ‘new phase’ in its battle with Israel. Qassem emphasised that the conflict with Israel is now an ‘endless battle.’

Earlier, a Hezbollah legislator said that the group was prepared for ‘any scenario,’ including war with Israel, following the killing of a senior commander in Beirut and dozens of his members in a Lebanon-wide communications device explosion, widely attributed to Israel.

Elsewhere, dovish central bank comments on Friday boosted demand for gold as a hedge, as BOJ Governor Ueda said the BOJ could raise interest rates gradually and ECB Governing Council member Rehn said the ECB has a ‘clear easing direction for its monetary policy.’ Fed Governor Waller also said, ‘Inflation is running slower than I thought.’

Precious metals prices retreated from their best levels on Friday before the close, as the dollar strengthened slightly. In addition, higher global bond yields on Friday had a negative impact on precious metals. Silver was also under pressure on Friday, after copper prices gave up an early rally to a 2-month high and turned lower, triggering long-term liquidation in silver.

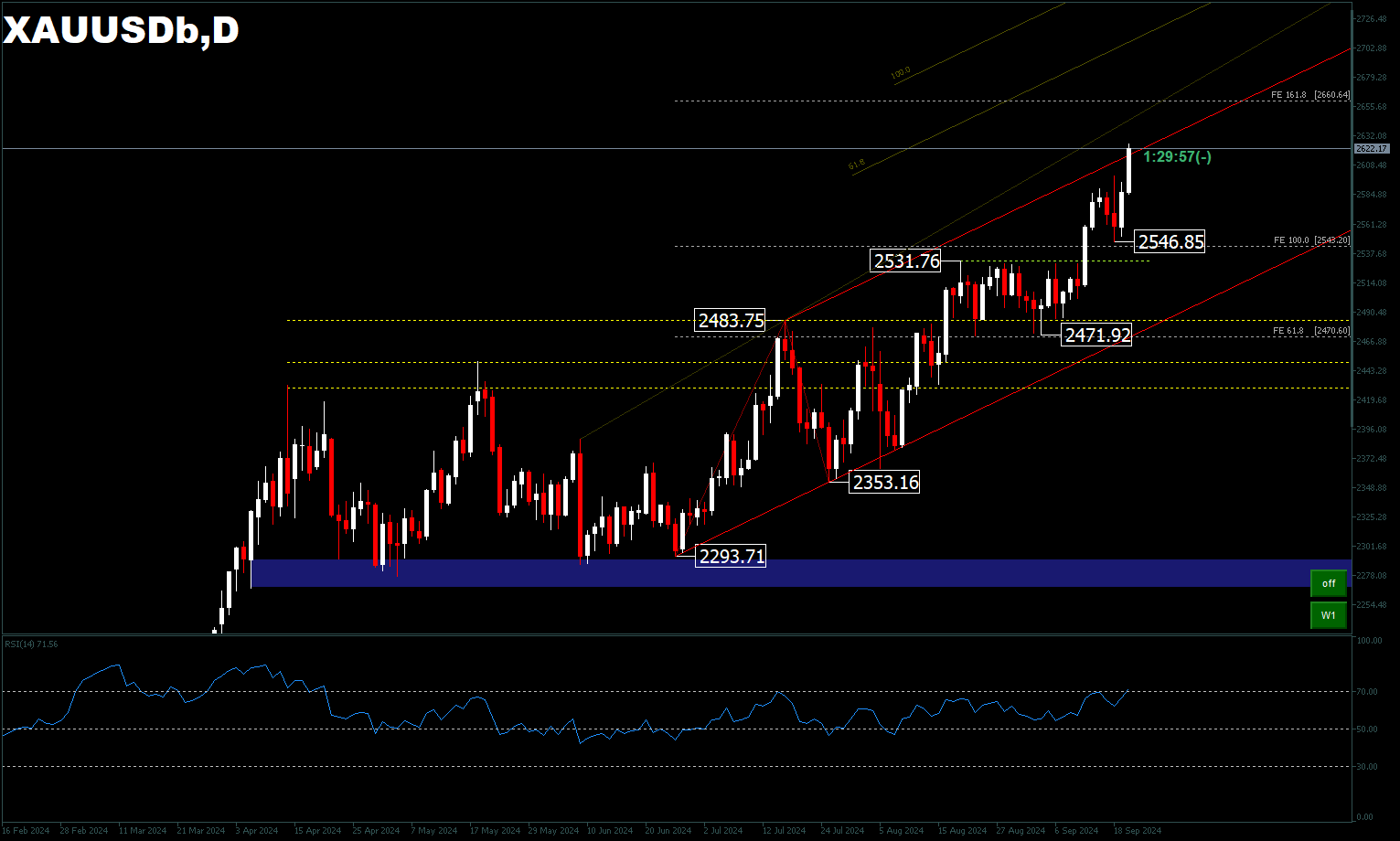

From a technical perspective, XAUUSD extended its wave extension to $2625.78 last week. In the daily period, the RSI is currently in the overbought zone, which suggests strong upside momentum for gold prices in the short-term. Further rallies are projected for FE161.8% [$2660.64] from $2293.71 – $2483.75 and $2353.16 pullback.

On the downside, the price level of $2531.76 will be the level considered by the buyers. While a drop below $2471.92 will be the starting point of the short-term correction.

XAGUSD [Silver] – Silver rose above $31 per ounce in mid-September, hitting its highest level in two months following the interest rate cut from the Federal Reserve this week. The US central bank kicked off its easing campaign with a 50 basis points rate cut in September and signalled further rate cuts, with two more quarter-point cuts for the rest of the year. The moves raised hopes of a soft landing for the US economy as inflation returns to the bank’s target, while increasing the likelihood of policy easing in other developed economies.

Meanwhile, top consumer China unexpectedly kept key lending rates unchanged the previous week, even as the Fed’s aggressive rate cuts provided room for policy easing. However, markets still expect China to introduce more stimulus to prop up the economy, following a series of disappointing economic data for August.

On a more optimistic note, rising silver demand in China is emerging as a potential catalyst for price recovery. The Shanghai Metal Exchange reported that silver prices in China are around 10% higher than in Western markets, highlighting strong domestic demand. This surge is attributed to China’s booming solar panel industry and technology sector, which has driven silver imports to exceed 400 tonnes in June and July; double the previous year’s monthly average of 200 tonnes.

Strong demand from China has raised concerns about a potential ‘silver squeeze’ as global production struggles to keep pace with rising demand. This imbalance could lead to higher silver prices, especially in industries such as electronics and solar energy that rely heavily on the metal. If silver remains in short supply, the market could face the challenge of further price increases.

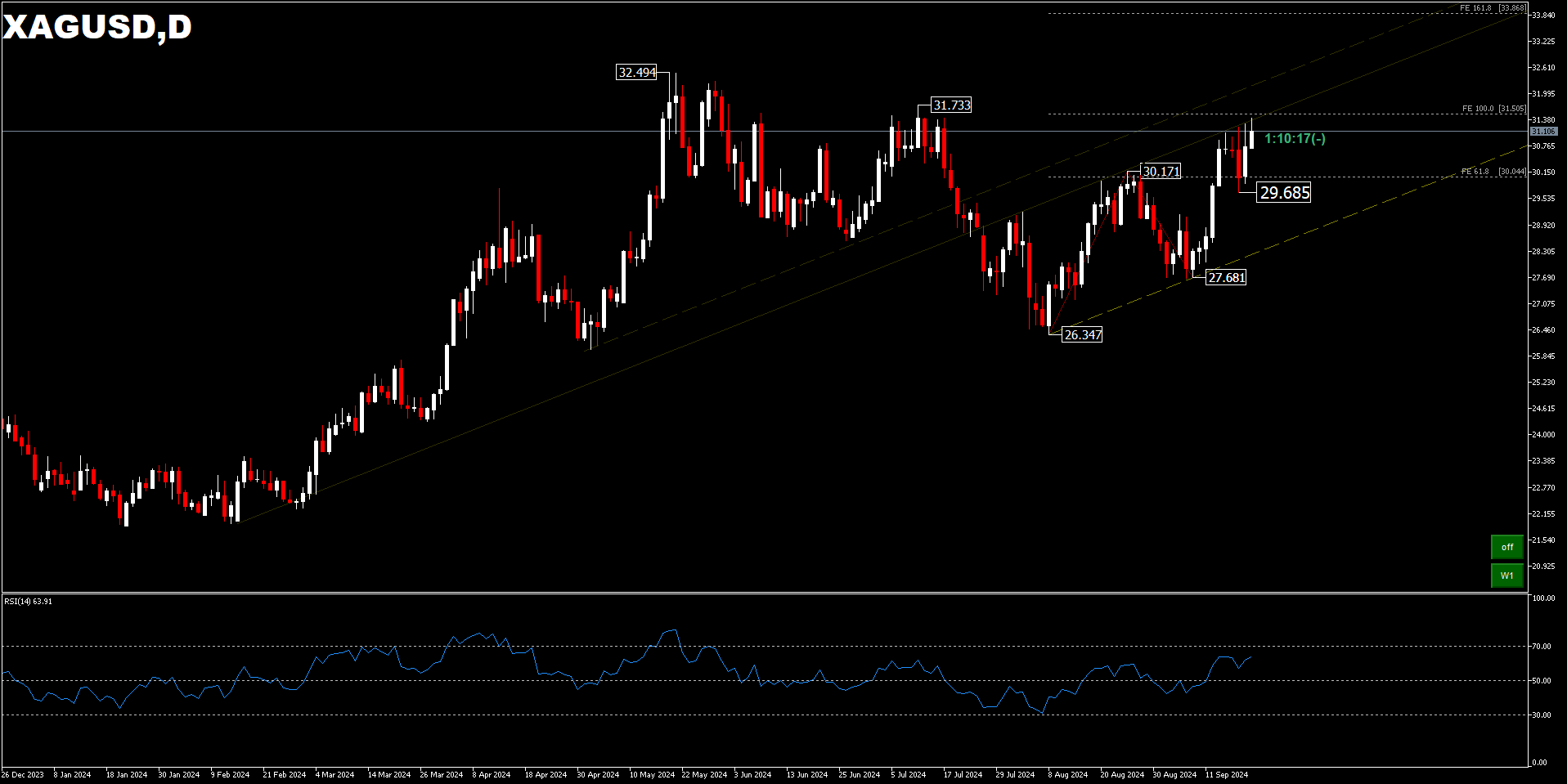

From a technical perspective, XAGUSD on a daily period is yet to show a tired bullish trend. The RSI is currently yet to reach the overbought zone and a continued rally above $31.73 and $32.49 resistance is projected for FE161.8% [$33.86] of $26.34 – $30.17 and $27.68 pullback.

On the downside, as long as the $32.49 resistance holds, the market will likely still see the $30.17 price level as a level worth defending. However, a drop below $29.68, then silver prices will enter a consolidation phase first.

Copper – Copper futures prices rose above $4.3 per pound in mid-September, reaching the highest level in two months as the US Federal Reserve’s interest rate cut improved the global economic outlook, fuelling a rally in risk assets. The market also awaited potential support from China’s economy as the top copper consumer, after weaker-than-expected industrial output, retail sales and fixed asset investment underscored manufacturing’s downward trajectory without more stimulus. On the supply side, energy shortages in Zambia depressed output from one of the world’s top copper ore suppliers.

China, as a significant supplier and consumer of copper, plays an important role in shaping trends in this important metal market. The surge in copper prices earlier this year was fuelled by a decline in Chinese production, triggered by a sharp drop in copper processing costs. However, sluggish Chinese economic data in recent months, coupled with global market turmoil amid fears of a US recession, caused copper prices to hit a five-month low in August [$3.9].

Although market sentiment has recently recovered, which has caused copper prices to rebound over the past week, the ongoing sluggishness in China’s property sector is expected to continue to weigh on demand. However, the weakening US dollar may help offset some of this decline.

In the long term, copper is likely to remain in an uptrend. Copper is an important resource for renewable energy, electric vehicles (EVs) and artificial intelligence (AI) technology. S&P Global has forecast that copper demand will double, reaching 50 million metric tonnes by 2035, with the most significant demand expected to come from the US, China, Europe and India.

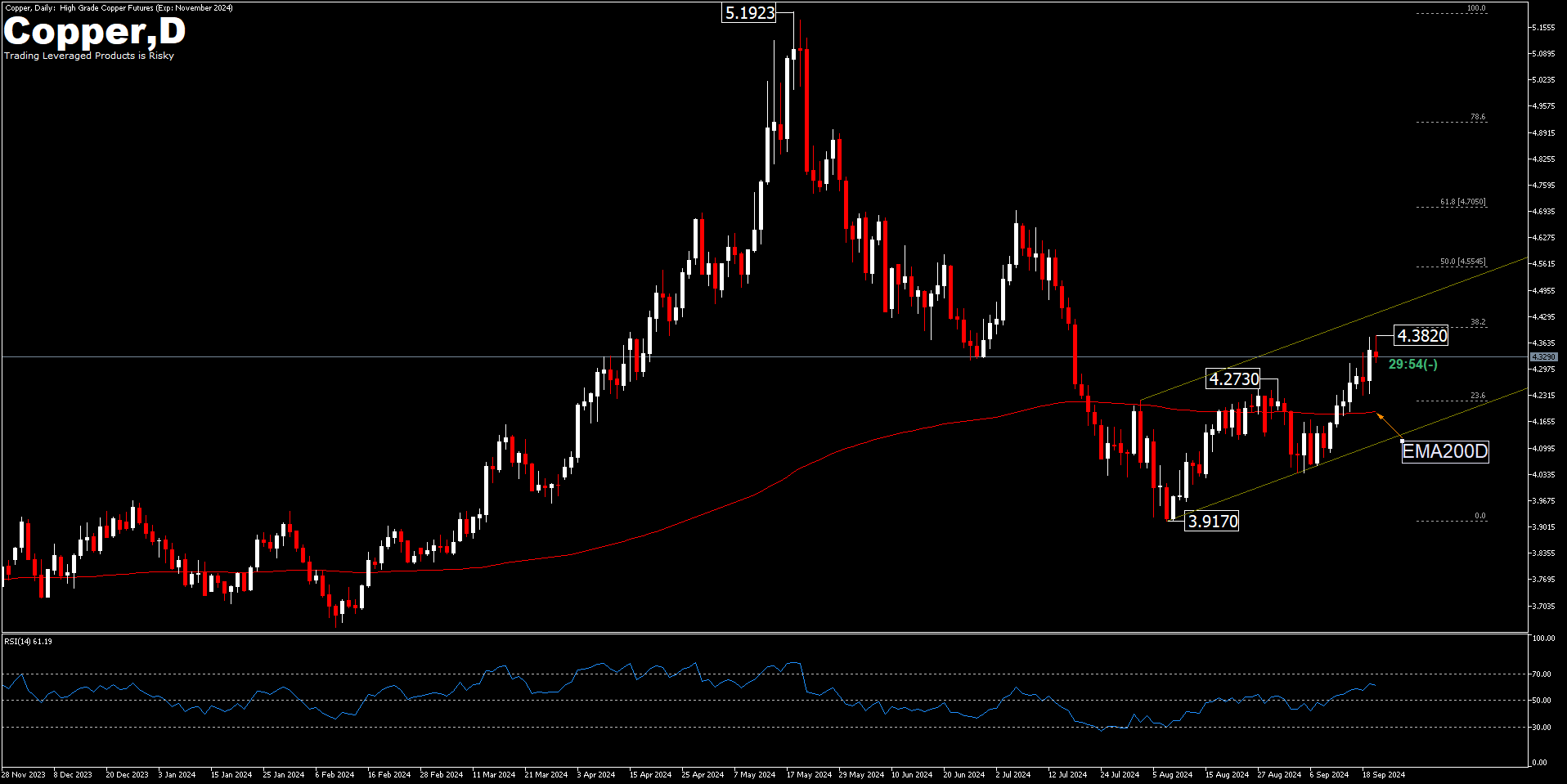

From a technical perspective, Copper on the daily period is yet to show a tired bullish trend. The RSI is yet to reach the overbought zone and a continued rally above the $4.27 resistance could still move to test the 38.2%; 50.0% to 61.8% retracement levels located at $4.40; $4.55 and $4.70 respectively.

Click here to access our Economic Calendar

Ady Phangestu

Market Analyst – HF Educational Office – Indonesia

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.