EURUSD, H1

ECB left policy rates unchanged, but as expected, the guidance on rates was pushed back with the central bank now saying that rates will remain unchanged at least until the middle of next year “and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below but close to 2% over the medium term”. The reinvestment of current asset holdings will continue until well past the timing of the first rate hike. New TLTRO loans will come at 0.1 basis points above the average rate of the repo rates applied over the life of the loans. This gives the ECB flexibility, but there was no tiering of the deposit rate, which is also a benchmark for TLTROs for those banks whose eligible net lending exceeds the benchmark.

The unchanged initial claims reading in the first week of June, following an upwardly revised 218k (was 215k) level at the end of May, followed a lean 212k in the prior two weeks that included the May BLS survey week. There is a firm path for claims since the elevated 230k figures in the weeks of Easter and Good Friday, though claims remain above the three-week stretch of 49-year lows that culminated with a 193k figure in the April BLS survey week. Claims are entering June above averages of 217k in May, 215k in April, and 214k in March, but below prior averages of 222k in February and 224k in January. We saw a cycle-low 212k average last September. The 212k May BLS survey week reading overshot the 193k April figure, but undershot prior survey week readings of 216k in March, 213k in February, and 217k in January. Expectations for the May nonfarm payroll tomorrow have a consensus around 183k, with upside risk from tight claims in May, a climb in most confidence measures from winter lows, and a stabilization in most May producer sentiment measures, but with downside risk from the 27k May ADP rise reported yesterday. The vehicle sector looks poised to support job growth in May, given a 6% vehicle sales bounce that reversed a 6% April drop, and an expected 2% assembly rate rise after a 4% April drop to an 11-month low of 10.6 mln.

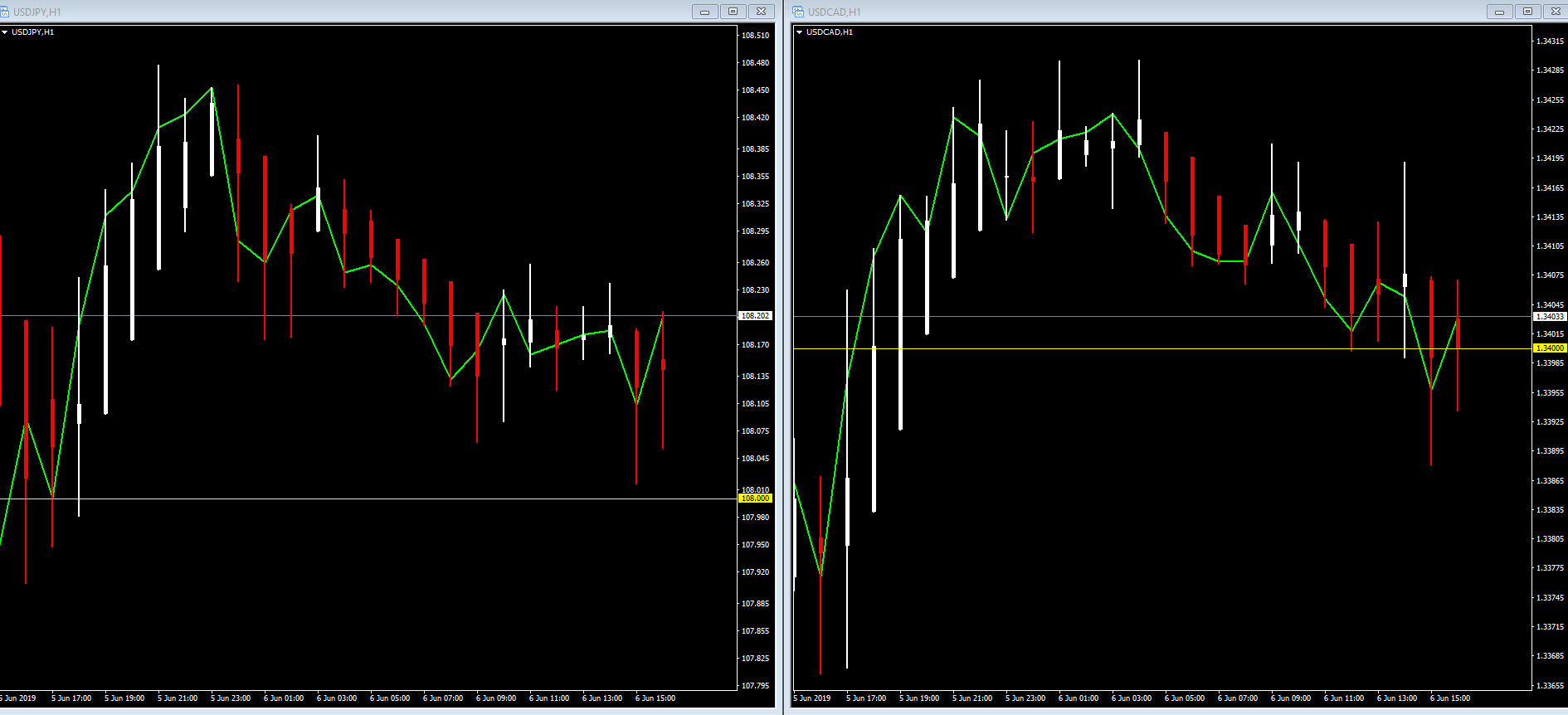

The Greenback continued to ease with EURUSD spiking to an 8 week high over 1.1300, USDJPY testing 108.00 again and USDCAD breaking 1.3400 and moving lower.

Click here to access the Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leverage Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.