A week that will be marked by meetings and decisions of practically all the world’s most important central banks is off to a slow start, with US futures fractionally up (+0.08% / +0.15%) after Friday’s drubbing. It was a decisive day for the weekly trend, sending both the US500 and US100 into negative territory for the second time in a row: only the US30 managed to close the week at +0.1%. The tech sector was the hardest hit, -2.2%, led by the Oracle debacle, -10%. On the other front, Utilities outperformed, +2.8%. This was on Friday, when the Nasdaq sank -1.75% and the US500 posted -1.22%: two factors contributed to this bad performance. First, the Michigan Consumer Sentiment Index, which came out at 67.7, below expectations and well below its historical average, which is close to 86. This Index accounts for 2/3 of the US economy and is therefore a valuable indicator of the overall state of affairs there. The other major event that certainly helped the declines to be heavy was the UAW strike, for the first time simultaneously at the Ford, GM and Stellantis plants: the demands are for wage increases of up to 40% and the impact of such news on the perception of future inflation can be worrying. Today is poor in data, but from tonight Central Banks Week kicks off with the minutes of the latest RBA meeting and from Wednesday night onwards all the big central banks will cascade. The FED decision will be made on Wednesday evening.

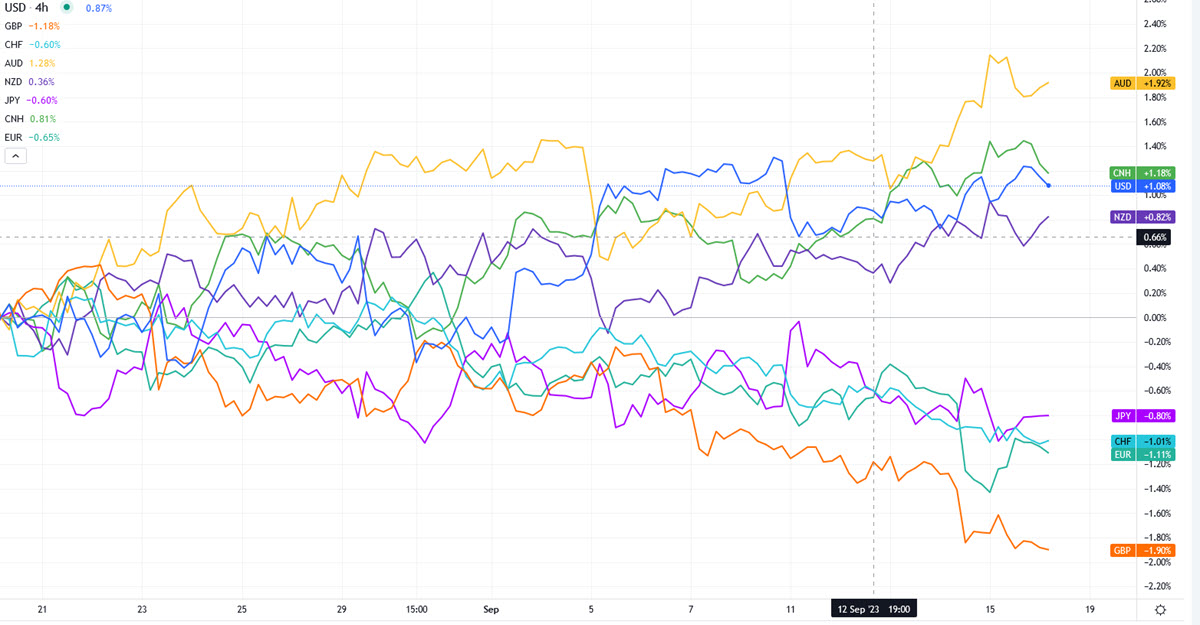

Since the 3rd week of August, Antipodeans + CNH have relatively outperformed

- FX – USDIndex -0.12% at 104.86; Antipodeans are relatively stronger with AUDUSD +0.23% and NZDUSD +0.31%, this comes also on the back of USDCNH <7.30 (7.28 now). GBPUSD sits at 1.24, EURUSD +0.13% at 1.0673.

- Stocks – US Futures fractionally higher (US500 + 0.15%, US100 +0.22%, US30 +0.12%); GER40 futures are turning negative right now (-0.03% at 15869), CAC is -0.05%. Last Friday, META and NVDA sunk >-3%, Microsoft -2.50%.

- Commodities – USOil is trading close to 10-month high at $91.60, UKOil puts $95 in sight.

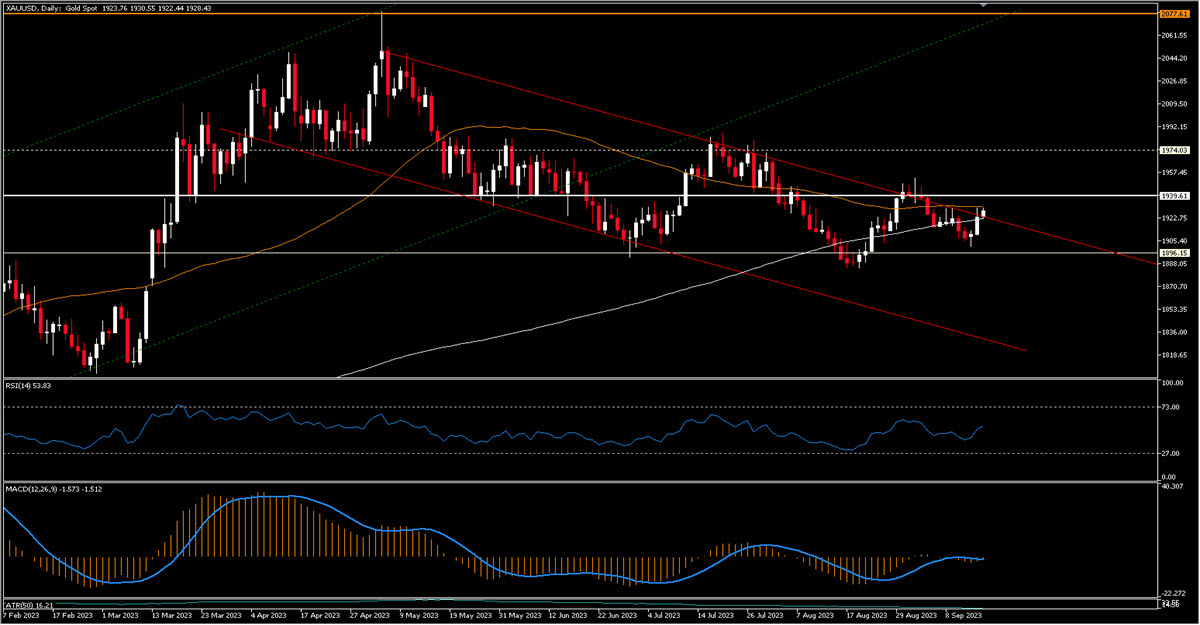

- GOLD – +0.32% at $1929, XAG +0.73% at $23.20.

Today: highlights include US NAHB Housing Market Index, Bundesbank Monthly Report, remarks from Saudi Arabia’s Energy Minister, ECB de Guindos & Panetta.

Key Movers: XAUUSD (+0.22% @ $1928.09) is in a very tight range between its 50d and 200d MAs and close to the upper bound of a descending channel.

Click here to access our Economic Calendar

Marco Turatti

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.