There were no surprises from the FOMC. As universally expected, the Fed increased the funds rate 25 bps to a 5.25% to 5.50% band. This is the highest since early 2001. Wall Street was mixed all session. The US30 was up for a 13th consecutive session, the best streak since January 1987. A gain today would be an all-time record going all the way back to June 1897. The policy statement and Chair Powell’s press conference did not provide a clear rate path into the end of the year, but stressed that the decision will be dependent on upcoming data, of which there are two more CPI reports and two more payroll reports to be assessed.

ECB Preview: the ECB is widely expected to deliver another 25 basis point hike today, while keeping all options open for September. This will mean the presser should be a tad more dovish than in June, when Lagarde effectively committed to further tightening this month. However, while there are now more signs that previous rate hikes are feeding through the system, and that core is plateauing, inflation remains far above the ECB’s target and keeping all options on the table for September also means that further tightening after the summer break remains a possibility.

- FX – The USDIndex sagged modestly to 100.40, down from the week’s high at 101.37. USDJPY broke the 140 low, reflecting traders’ unease ahead of the Bank of Japan meeting Friday that some think will include a policy change. GBP spiked to 1.2984 and EUR at 1.1127.

- Stocks – The US30 closed with 0.23% gains and fractional losses in the US500 and US100 as investors also monitored various earnings results. The GER40 gapped up to 16,194 as the German GfK consumer confidence resumes uptrend. #Meta ads revenue rebounded and despite the metaverse related rising costs. #Samsung reports 95% drop in profit, expects demand to recover.

- Commodities – USOil steady at 3-day territory.

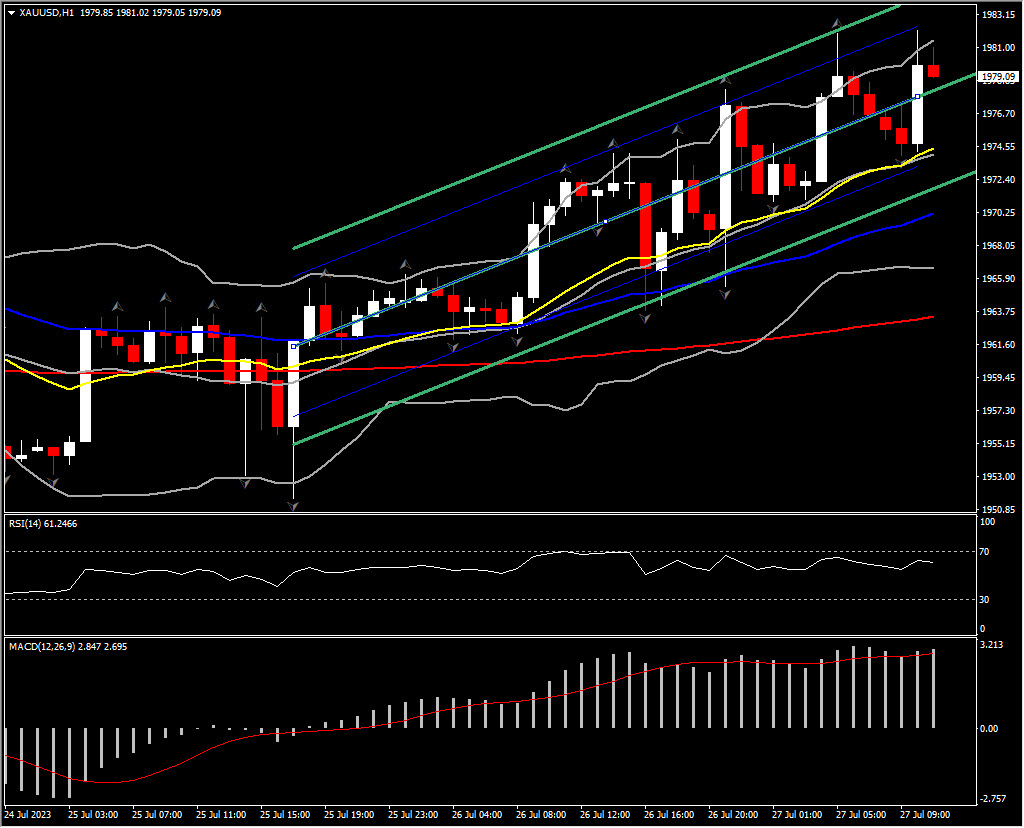

- Gold – extended to $1982.

Today: ECB Rate Decision and Press Conference, US Durable goods and GDP. Earnings: McDonald’s, Mastercard, Intel, AbbVie, Shell, Comcast etc.

Biggest Mover: (@6:30 GMT) XAUUSD (-0.64%) topped at $1982 with RSI and MACD positively configured while ATR(H1) is at 4.28 and ATR(D) is at 16.55.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.