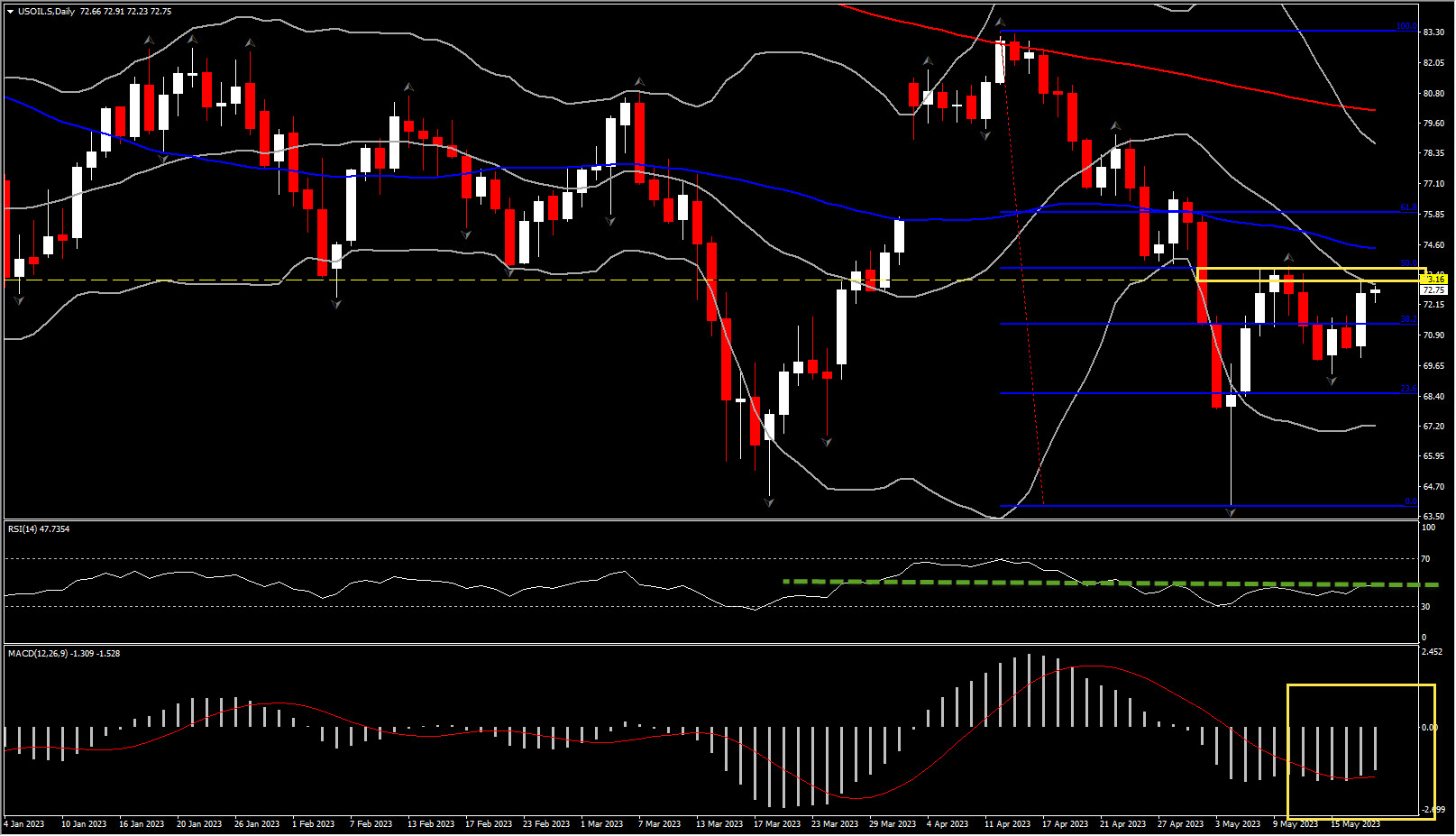

The ascent in the Oil prices has stalled for now and USOIL is a tad lower on the day currently at $72.66 per barrel, UKOIL at $76.78. Markets are increasingly confident that an agreement on the US debt ceiling can be found, which has helped to bolster risk appetite. Oil continues to trade in a narrow range, however, as markets weigh central bank and demand outlooks. OPEC and IEA may have lifted their demand forecasts for this year also based on strengthening demand from China, but data releases so far suggest that the post-Covid bounce in activity is weaker than markets had been hoping.

Meanwhile Russian oil continues to hit world markets as Russia’s oil exports continue to rise. IEA data showed that Russia’s oil exports rose by another 50,000 barrels a day in April to a post invasion high of 8.3 million barrels per day, far exceeding the 7.7 million b/d in 2022. Revenues still dropped 27% y/y in April, despite the expansion, highlighting that Russia has to accept heavy discounts as it finds new buyers and routes. Almost 80% of the country’s crude shipments now flow to China and India, according to the IEA.

Meanwhile, the EU is debating whether to crack down on Indian refiners reselling Russian oil as refined fuels, including diesel. Josep Borrell, the EU’s high representative for foreign policy, told the Financial Times that “if diesel or gasoline is entering Europe coming from India and being produced with Russian oil, that is certainly a circumvention of sanctions and member states have to take measures“. India has become one of the biggest buyers of Russian crude oil and its refiners are earning large margins by buying heavily discounted crude and selling full-priced fuels into Europe. The trade is legal, but has helped Russia to support earnings from its oil sales, despite sanctions.

Nevertheless, recession fears continue to linger. China’s data round once again fell short of expectations, adding to signs that the expected bounce in energy demand will take longer to materialize than anticipated. The output cuts implemented by OPEC+ haven’t boosted prices in this environment but may have helped to put a floor under oil futures, which have essentially moved sideways since May 3 when the WTI contract hit a low of $63.64 per barrel.

However, OPEC still expects China’s recovery to gather pace and boost demand later in the year. The IEA also said that world fuel consumption will increase by 2.2 million barrels a day this year, which is about 200K a day more than forecast previously. Total consumption would hit a record 102 million as China’s demand hits an all time high following the scrapping of Covid restrictions.

Markets may be disappointed by the speed of China’s recovery, but the IEA as well as OPEC suggested that the recovery was actually stronger than they had anticipated preciously. The head of the IEA’s oil market division said in a Bloomberg interview “we are seeing really strong demand, especially in Asia”.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.