All eyes will be on the FOMC outcome where a 50 bp increase is fully priced in. Hence, attention will be on the dots and what they imply about the rate trajectory, as well as the tone in Chair Powell’s press conference and then the GDP, unemployment rate, and PCE chain price projections for clues on the policy trajectory.

Powell already warned that the funds rate forecasts will be revised up. The key is how many and by how much. Upward revisions are anticipated in some of the dots to a 5% handle, as suggested by Powell. We also assume a shift higher from uber-hawk Bullard at a minimum to a 5% handle in 2023, and potentially from the hawkish Waller too. Interestingly, with CPI released today just a day before the policy decision, another below consensus report could support the doves and the more moderates on the Committee.

The CPI is expected to post gains of 0.3% for the headline and 0.3% for the core in November, following respective October increases of 0.4% and 0.3%. CPI gasoline prices look poised to fall -2% to restrain the headline pace. A dissipating upward pressure on core prices into 2023 is forecasted as disruptions from global supply chain bottlenecks and the war in Ukraine subside. As-expected monthly price prints would result in deceleration in the y/y headline increases to 7.3% from 7.7% in October, versus a 40-year high of 9.1% in June. The core y/y gain should slow to 6.1% from 6.3% in October and a 40-year high of 6.6% in September.

If CPI is in line with expectations and while the high end of the ranges may move up, the funds rate medians are likely to remain unchanged from September at 4.6% and 3.9% for 2024. Risk, however, is for an upshift to 4.9% next year. Also, Chair Powell will likely reiterate a hawkish tone to offset the moderate in the rate hike, sticking to the belief that the bigger risk currently is not tightening enough now and allowing inflation to get out of control. However, he also gave a nod to the fear of overtightening camp in his Brookings speech after the FOMC minutes to the November meeting noted worries over the cumulative effects of rate hikes and the lagged effects on the economy. The policy statement could give a clue on the rate trajectory if there is a change from last month which stated, “the Committee anticipates that ongoing increases in the target range will be appropriate.”

If Fed’s actions are proven successful against inflation leaving the room with few more hikes ahead in case that inflation peaked, historically has been seen pressuring US Dollar as it hints that recession is avoided. However, this time things are a bit different as there is a combination of contradictions for the market participants to handle, such recession fears even as the Fed raises rates, overextended valuations, high earnings projections for 2023 (US stocks are still very expensive going into 2023). Hence, all these along with the geopolitics could backfire.

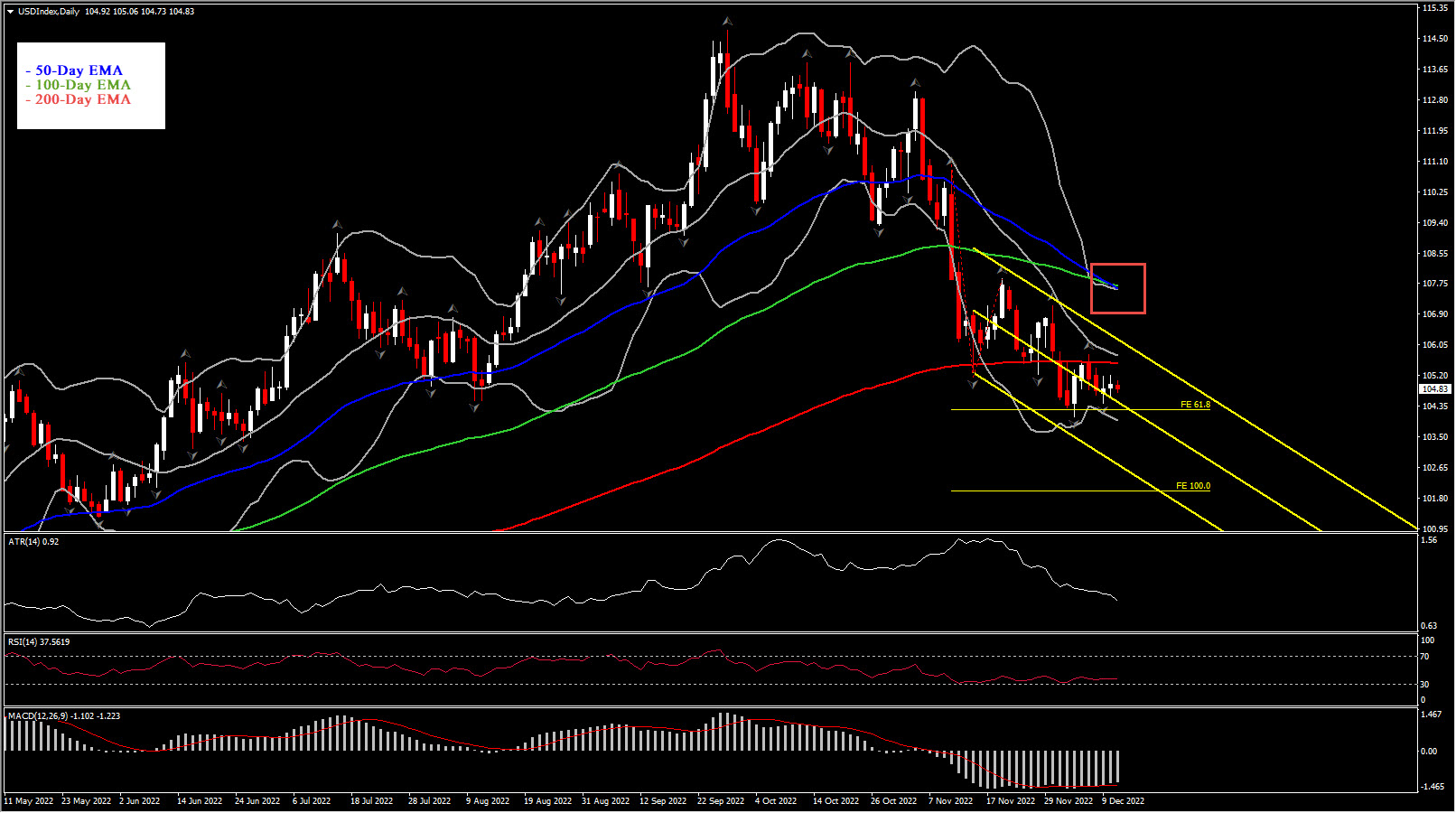

USDIndex Outlook

Taking a technical look, it is clear the USDIndex as we moving to the year’s end has stuck near a very important Support level, which could prove to be a good test for the USD Index latest drift, from 20-years highs 114.70 to 104 area.

To the downside, bearish bias may increase 104 or lower, the June bottom of 103.30 could curb any further declines and open the door to 101-102 area, with the latter being the confluence of 50% Fib level from 2020 bottom to 2022 peak, and the 100 FE from the latest swing in November. Eyes also turn to a potential confirmation of a bearish cross between 50- and 100-day EMA, which could add more to the asset’s negative outlook.

To the upside, the 200-day SMA and the 106 level remain strong Ressistance area for the asset to challenge. Breaking above those, the price could then ascend to test the July’s peak at 109.00 which is the latest upper fractal.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.