- The USD Index has collapsed from over 107.80 on Monday to 105.50 today.

FOMC Mins. – Confirmed that a “substantial majority” believed slowing in the pace of increases would likely soon be appropriate. That largely confirms what has been priced in, with a 50 bp increase fully priced in for December and “significant uncertainty” about the ultimate level of the funds rate. “Various participants” (Bullard , Mester, etc no doubt) noted that with few signs of inflation abating and demand and supply still out of balance, they suspected the ultimate level of the funds rate would have to be “somewhat higher” than previously seen. Powell seemed to confirm this at the press conference.

Earlier Weekly Claims jumped to a 240k and the Continuing Claims hit a high not seen since March. Whilst Durable Goods were stronger than expected, PMI data missed. The mixed news gave a lift to stocks, weighed on the Dollar and saw yields drop too. US10-yr closed at 3.69%, with the 2/10 yr inversion at -79 bps.

- EUR – rallied to over 1.0400 an 8-day high at 1.0448 earlier.

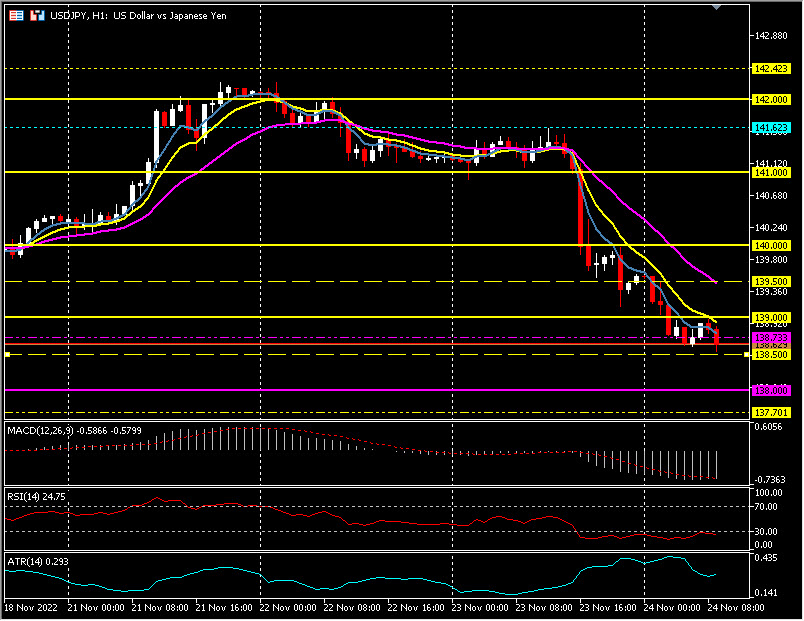

- JPY – eased all the way down to 138.50 zone from over 141.60 yesterday. JPY PMI missed and moved back into contraction at 49.4 from 50.7.

- GBP – Sterling rallied on the weaker USD breaking & breaching the key 1.2000 slevel and testing 1.2080.

- Stocks – Wall Street closed in the green (NASDAQ +0.99%) TSLA +7.82% (upgrade from CITI to Neutral from Sell). In the UK Manchester United shares rallied +26.8% on news the Glazier family could be willing to sell some or all of their holdings). US500 +23.68 (+0.59%) 4027, FUTS trades at 4042 now. – https://themarketear.com/

- USOil – Sank from $81.50 and trades at $77.50 now. G7 proposed price cap higher than expected. Inventories declined by 3.7m barrels this week more than the 2.6m expected but much less than last week’s outsized 5.4m barrel drawdown.

- Gold – Tested down to $1725 before recovering $1750 to trade at $1755 now.

- BTC – Sentiment woes continue, but holds $16.6k today capped at $16.8k.

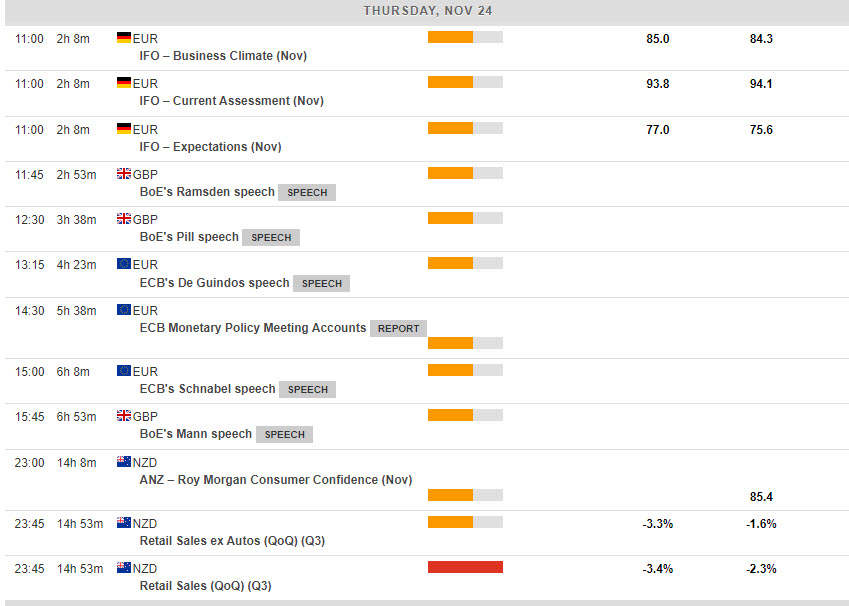

Today – German Ifo, ECB Minutes, (Riksbank, CBRT & SARB Policy Announcements), Speeches from BoE’s Pill, Ramsden, Mann, ECB’s Schnabel & de Guindos.

Biggest FX Mover @ (07:30 GMT) USDJPY (-0.60%) continued to decline from the test of 142.00 earlier this week. Trades at 138.50. MAs aligning lower, MACD histogram & signal line negative & falling, RSI 24.75 & OS, H1 ATR 0.293, Daily ATR 2.230.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.