The market was pushed and pulled by geopolitical risks and uncertainties, earnings ups and downs, Fed tightening angst and recession risks.

USDIndex bounced to 106.38 currently steady at 106, Yields spiked sharply higher with selling persisting into the close (10yr 2.746% having challenged 2.51% overnight) dragged by hawkish Fedspeak and the safe arrival of Pelosi. The safe-haven Yen continued its slide. US Stocks ended in the red. Asian markets mixed as China has its warheads trained on Taiwan but on the flipside markets are trying to weigh growth risks and the Fed outlook (Hang Seng & Nikkei 0.5%, CSI 300 -0.2%). European FUTS also lower (-0.6%). Oil at $94, Gold holds over $1750 and BTC down under $23k.

Fed’s Mester said below trend growth is not a bad outcome, and it is necessary to get inflation under control. Fed President Daly said the FOMC is likely to raise rates and keep them high for a while, in her comments in a LinkedIn interview – ‘Nowhere Near’ Finished With Inflation Fight.

Data: A surprisingly strong bounce in German exports left the German trade balance with a solid surplus. China Services PMI readings also looked pretty strong – acceleration in activity. Swiss CPI inflation held steady at 3.4% y/y.

- USDIndex managed to climb back over 106.000 but it was weaker overnight, holding the 105.000 handle for a third straight day. YEN has given up some of its haven bid & EUR and GBP have also slumped.

- Equities – USA30 tumbled -1.23% (32.4K), USA500 off -0.67% (4.1K) and USA100 -0.16% lower (below 13K).

- Yields 10-year has already corrected -3.5 bp at 2.71% today and the 10-year Bund yield is down -1.8 bp at 0.79%.

- Oil – steady at $94.00 from $96.30 ahead of the OPEC+. It is likely to keep output unchanged in September, or raise it slightly.

- Gold – rose in the morning to $1768 after a sharp decline yesterday.

- Bitcoin directionless, at 22.98K.

- FX Markets – EURUSD dip to 1.0155 zone, USDJPY is at 133.18, as haven flows into the Yen have receded. Cable turns below 1.2200 again.

Today – OPEC+ meeting, EU Retail Sales and US ISM Services. Earnings: CVS Health, Booking Holdings, Moderna, Regeneron etc.

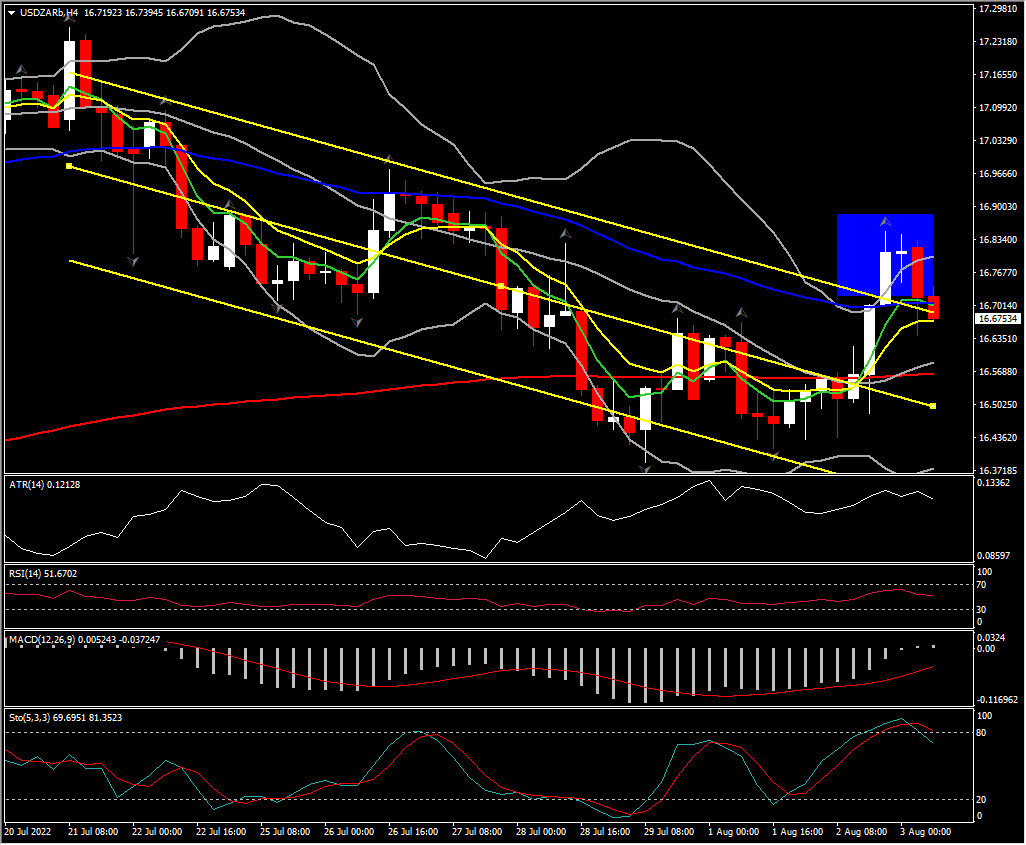

Biggest FX Mover @ (06:30 GMT) USDZAR (-0.70%) posted an evening start pattern this morning at 16.70. MAs flattened, MACD lines held negative , RSI 53, OS & falling, H4 ATR 0.12128, Daily ATR 0.26199.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.