FX News Today

Asian Market Wrap: Bond markets are back under pressure and 10-year JGB yields erased yesterday’s decline and jumped 5.8 bp to 0.110% as markets test BoJ’s willingness to let the 10-year climb as high as 0.2%. 10-year Treasury yields are up 1.5 bp at 2.975%. The USD strengthened amid reports that the US is retching up its trade threat to propose raising its planned 10% tariffs on USD 200 bln in Chinese imports to 25%. This followed earlier source stories suggesting that the US and China were trying to restart talks. Concerns about US-China trade relations saw Chinese indices underperforming, with Hang Seng and CSI 300 down by -0.09% and -0.39% respectively, elsewhere markets moved mostly higher, led by Japanese indices, with the Topix rebounding 1.04%, as the Yen weakened against the Dollar and positive results from Apple Inc helped to stabilize tech stocks. US futures are now also mostly up, led by the NASDAQ, but European futures are under pressure in opening trade, as the BoE meeting comes into view amid the wide rise in yields and concerns about US-China trade relations. Oil prices are down on the day and the September WTI future is trading at USD 68.42 per barrel.

FX Update: The Dollar has traded moderately firmer into the London interbank open, with the USDIndex showing a 0.2% gain at 94.65, a 2-day high. EURUSD concurrently posted a 2-day low, at 1.1675, which is near the midway mark of a broadly sideways range that’s been evolving since early June. USDJPY rose for a second day and printed a 12-day high at 111.98. PBoC set the USDCNY reference rate higher once again, to 6.8293, which is the lowest for the Yuan since May 2017, after 6.8165 yesterday. The Trump administration said that it is thinking of hiking the 10% tariff in place on $200 bln worth of Chinese imports to 25%, which looks like a ploy ahead of a recommencement of trade talks. In data, Japan’s final manufacturing PMI for July was unexpectedly revised higher, to 52.3 from 51.6 reported in the flash estimate, but this still marked a slowing in trend while the pace of expansion in new orders dropped off notably. China’s July manufacturing, meanwhile, undershot expectations at 50.8, down from 51.5, with weakness blamed on the Sino – US trade standoff. Focus today will be on PMI releases in Europe and North America. The Fed will today conclude its 2-day FOMC policy meeting today, which should be a non-event for markets with no changes expected to policy and only minor changes likely on the statement compared to the Fed’s June policy statement.

Charts of the Day

Main Macro Events Today

- Eurozone & German Manufacturing PMI – Expectations – The EU Manufacturing PMI is expected to be confirmed at 55.1, in line with the preliminary number, while the German one is expected to remain unchanged at 57.3.

- UK Manufacturing PMI – Expectations –anticipated at 54.0 in the headline (median 54.2) after 54.4 in June.

- US ADP Non-Farm Employment Change and ISM Manufacturing PMI – Expectations – The manufacturing ISM is projected to fall to 59.0 in July, from June’s 60.2, and down only slightly from the 14-year high of 60.8 from February, and would still reflect a robust rate of expansion.

- Canada Manufacturing PMI – Expectations –The Markit manufacturing PMI for July may show some slippage in activity after climbing 0.9 points to a record high of 57.1 in June, with strength in new orders.

- FOMC Statement and Federal Funds Rate – Fed is widely expected to leave policy unchanged, with the announcement set for today at 18:00 GMT.

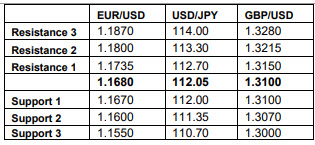

Support and Resistance levels

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/08/01 14:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Andria Pichidi

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.