UK100, Daily

The Brexit negotiation process continues to drag on with what can be best described as disappointing progress, and prospects for a smooth exit are looking dim at this juncture with the EU leaders’ summit last week proving to be anything but the milestone juncture it had only recently been billed as. The Pound is trading over 13% below levels that were prevailing into the Brexit vote in June 2016, and while other factors have been at play, much of this lower trading band reflects a built-in “Brexit discount” to the market’s valuation of the currency.

EU chief Tusk said that the most difficult Brexit issues remained unresolved. Both the EU and UK are looking to have two fundamental pillars agreed on by the EU Summit on October 18-19. One is the Withdrawal Agreement, which concerns final divorce terms — citizens’ rights, final financial settlement, and a solution to avoid a hard Irish border. The other pillar is to lay out the “framework for the future relationship,” which will provide terms for a new trade agreement and for some other issues, such as security co-operation. When both sides agree — which is still by no means a certainty — the post-Brexit interim period will be signed off on, whereby the UK will remain in both the single market and customs union (but without member rights) from the legal Brexit day, 19 March 2019, through to the end of 2020.

Hence as political jitters in the UK continue to hang over markets, the UK100 headed south by -0.98%, at the start of the 3rd Quarter. Despite the Index managing to recover most of last Monday’s losses, the negative outlook remains as the Index opened today with a gap at nearly 400 pips below Friday’s close.

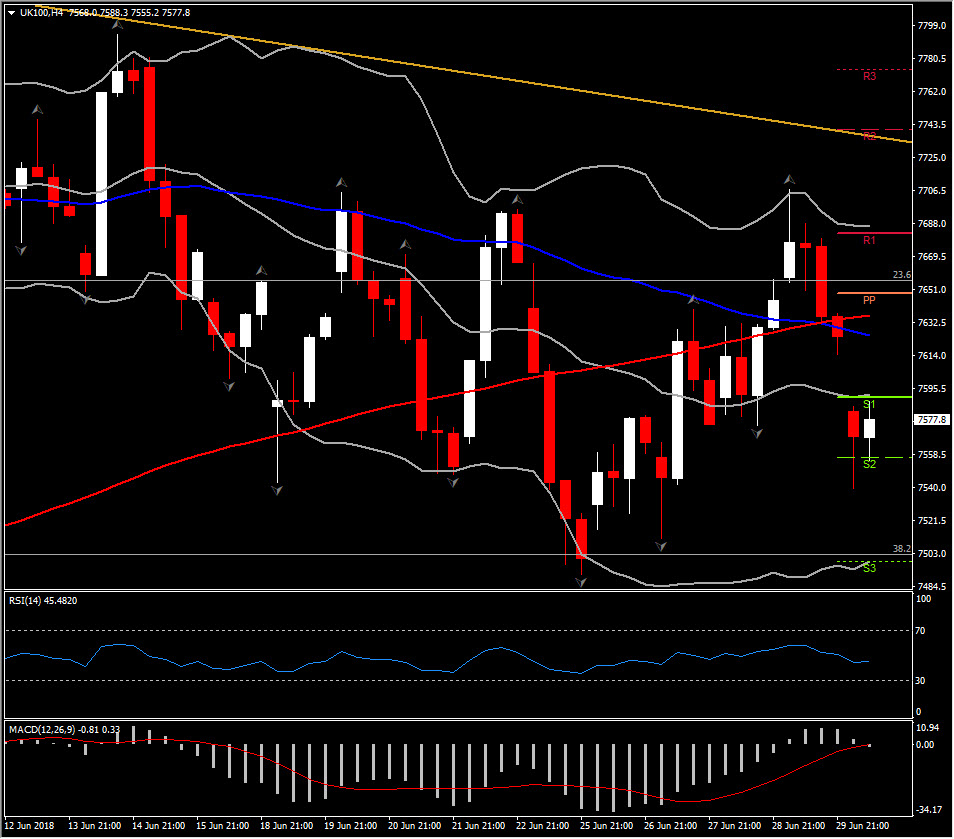

Although the UK100 is moving within a down-channel since May’s peak, the weekly long wicked candles suggest there is still bias to the upside. Still the bears remain in control as the FTSE continues forming weekly consecutive lower lows and lower highs. The Daily momentum indicators however present a neutral picture as both MACD and RSI remain close to neutral zone. Daily Support holds at 7,510.00 and Resistance comes at Friday’s peak, at 7,706.00

In the shortterm, the release of the UK Manufacturing PMI today, which unexpectedly improved slightly over the month, prevents the UK100 from selling off and underperforming against the GER30. So far today the pair has managed to hold above S2 at 7,555.00, suggesting that the morning’s gap is likely to be filled if the price moves above the S1 at 7,590.00. However as the overall outlook is negative, any swing higher could be a sell opportunity.

Intraday momentum indicators are mixed, as the RSI is stuck below 50 and MACD at neutral zone.

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/07/03 14:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Andria Pichidi

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.