FX News Today

Asian Market Wrap: 10-year Treasury yields lost earlier gains and are unchanged at 2.877%, 10-year JGB yields are up 0.3 bp at 0.027%, while yields elsewhere mostly declined as stocks struggled for direction with trade concerns continuing to hang over markets. Japanese indexes moved up from lows and are at -0.21% and -0.07% respectively. The Hang Seng meanwhile is down -0.73% and the CSI 300 down -1.59% as the Yuan continued to weaken offshore amid fears that China’s liquidity squeeze will lead to corporate bond defaults in 2H, and the drive for deleveraging is limiting lending and pushing up borrowing costs. Energy companies were supported by an ongoing rise in oil prices. The front-end USOil future rose to a high of USD 70.98, and is currently at USD 70.71 per barrel, amid reports the US is pushing allies to halt imports of Iranian crude. US stock futures are also down.

FX Update: USDJPY has traded moderately lower, back under 110.00, after posting a three-session peak at 110.22. The pair was lifted by post-Tokyo fix demand, rising to 110.20, before selling overwhelmed and turned the Dollar lower. The Yen is also firmer against other currencies as stock markets ebb back again after yesterday’s reprieve. AUDJPY, a cross with relatively high beta characteristics that has been sensitive to the deepening trade spat, is down over 0.3%, earlier printing an eight-day low at 80.81. As for USDJPY, the pair is about at the halfway mark of the broadly sideways range that’s been seen over the last six weeks. USDJPY has Resistance at 110.20-22, levels which encompass recent daily highs. The net directionless path is illustrated by the flat profiles of both the 20- and 50-day moving averages, which are presently sandwiching prevailing levels, being respectively situated at 110.05 and 109.65. Fundamentally the picture would be a bullish one (divergent Fed versus BoJ policy paths) were it not for the safe-haven premium being installed in the Japanese currency amid the backdrop of rising trade protectionism.

Charts of the Day

Main Macro Events Today

- BoE Governor Carney Speech – Scheduled Press Conference following the the publication of the Financial Stability Report at 08:30 GMT

- US Durable Goods Orders – Expectations – Likely to inch up to -1.0% in May from -1.6% in April. Core Orders expected to sink to 0.5% from 0.9% last time

- FOMC Members Quarles and Rosengren Speech

- BoC Governor Poloz Speech – Scheduled for 19:00 (text released 15 minutes earlier) speech regarding Transparency and Understanding

- RBNZ Interest Rate Decision & Statement – No Change to rates expected and “timing of any change dependent on how the economy develops” no change in statement

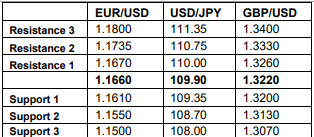

Support and Resistance Levels

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/06/27 14:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Stuart Cowell

Senior Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.