FX News Today

Asian Market Wrap: 10-year Treasury yields are up 0.5 bp at 2.9025, 10-year JGBs up 0. 1bp at 0.025%, both are down from session highs, but holding on to some of their gains as stock market sentiment settles ahead of key PMI readings in the Eurozone and the US today. Stock market sentiment remains muted, after yesterday’s sell off on Wall Street, but indices are up from early lows. Topix and Nikkei are still down -0.46% and -0.63% respectively, Hang Seng and CSI 300 managed to claw back some of yesterday’s losses and are up 0.19% and 0.40%. Trade concerns continue to linger and in Europe Italian political jitters remain a major concern, but US Stock Futures are improving. USOIL rallied and is at $66.26. OPEC and its allies reached a preliminary agreement to boost production despite opposition from Iran. The calendar had national CPI for Japan, which saw the annual reading rising to 0.7% from 0.6%. The Manufacturing PMI Index, meanwhile, rose to 53.1 from 52.8 and the All Industry Activity Index also improved.

FX Update: The Dollar has traded moderately softer so far today, extending a theme that has been seen since yesterday following the release of the Philly Fed index, which came in much weaker than expected. Amid this backdrop, the Euro has corrected some of its recent losses against most other currencies, which has likely reflected short covering, although in a market still wary about the Italian Government’s Eurosceptic bias. EURUSD has recovered back above 1.1600, posting a 3-day high at 1.1638. The pair had yesterday printed an 11-month low at 1.1508. USDJPY has settled near the 110.0 level, consolidating yesterday’s losses after the pair posted a 5-day high at 1110.75. Today, the focus will be on PMI survey data out of both Europe and the US, the evolving trade war, and the OPEC-plus-Russia meeting in Vienna, the run-in to which has exposed signs of discord among some members, which has pushed oil prices up.

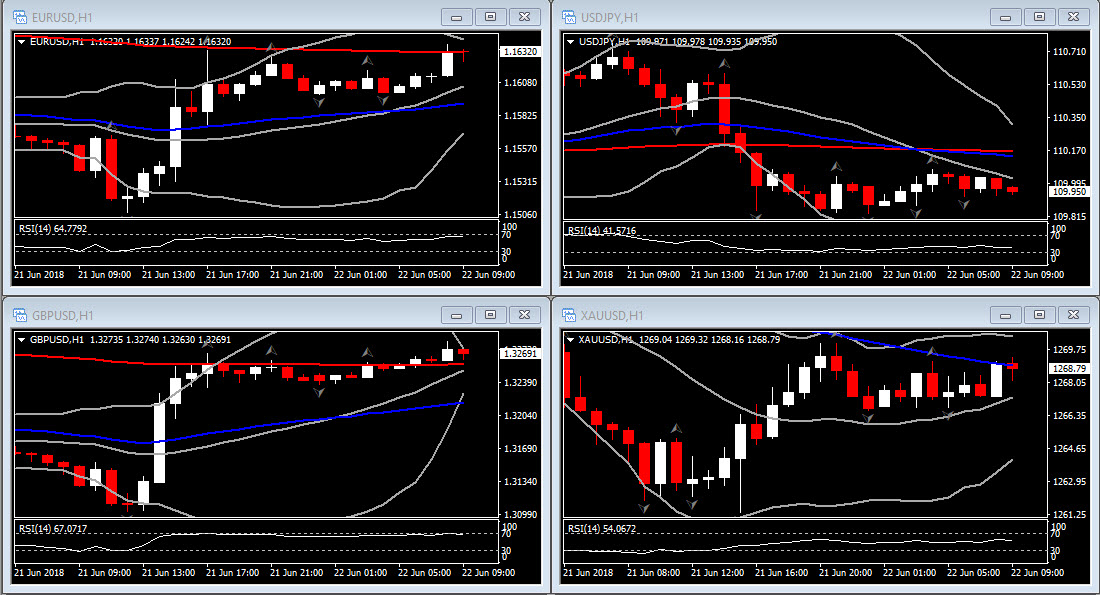

Charts of the Day

Main Macro Events Today

- German PMI – Expectations – June Manufacturing PMI should fall at 56.2 from 56.9 in the previous month. The Services reading is expected to remain unchanged at 52.1

- Eurozone PMI – Expectations – June Manufacturing PMI is expected at 55.1 down from 55.5 in the previous month, as trade concerns continue to bite. The Services reading is expected to hold up slightly better and fall back to 53.5 from 53.8 in the May.

- Canadian CPI and Retail Sales – Expectations – CPI is expected to grow 0.4% (m/m, nsa) in May after the 0.3% rise in April. The CPI is projected to grow at a 2.5% y/y pace in May, accelerating from the 2.2% clip in April. The Retail Sales are expected to rise only 0.1% in April after the 0.6% gain in March.

- US Services PMI – Expectations – is seen falling slightly to 56.4 in June.

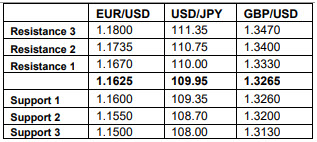

Support and Resistance Levels

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/06/26 14:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Andria Pichidi

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.