FX News Today

European Fixed Income Outlook: Markets are likely to begin the session on a stable footing given the steadying in stock markets in Asia, and lift in European and U.S. equity futures, which follows a paring of losses on Wall Street yesterday. Sino-U.S. trade tensions are still likely to remain a worry for investors given how entrench both the Trump administration and Beijing appear to be. In Europe today, the data calendar perks up a with the UK CBI industrial trends survey after German PPI data due. The central bankers conference in Sintra continues, and Brexit issues also remain in focus ahead of the next crucial EU summit. Germany auctions 30-year Bunds.

FX and Asia Markets Update: A pause in risk-off sentiment has seen stock markets recover some lost ground in Asia and the yen weaken as markets unwound some of the Japanese currency’s safe haven premium. Dollar bloc currencies have rebounded, with AUDJPY, a cross that often correlates inversely with pronounced directional swings in global stock markets, has rallied by 0.5%. Emerging market currencies have also lifted after many posted new year lows yesterday. USDJPY lifted to a two-day high of 110.25, putting a little distance in from yesterday’s 10-day low at 109.55 and returning the pairing to about the midway point of the range that’s been seen since the beginning of last week. EURUSD has been trading in a narrow range in the upper 1.1500s, capped below 1.1600 level. In stock markets, Wall Street pare the worst of intra-day losses yesterday, while Asian bourses gained, with the main Chinese indexes more than recovering intra-day losses. Despite the lift in stock markets, the Sino-U.S. trade spat is likely to remain a concern for investors, with both the Trump administration and Beijing looking entrenched in opposing positions.

Charts of the Day

Main Macro Events Today

- Speeches: ECB President Draghi, RBA Gov. Lowe, BOJ Gov. Kuroda and Fed’s Chair Powell.

- US Existing Home Sales and Current Account – Expectations –The current account deficit is expected to widen to -$129.0 bln in Q1, from -$128.2 bln in Q4. Existing home sales are projected to rebound 2.6% to 5.540 mln unit rate, following a weak start to Q2 with a 2.5% tumble in April to 5.460 mln.

- US Crude Oil Inventories

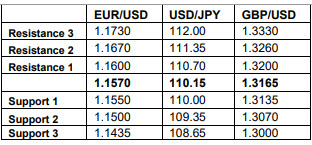

Support and Resistance Levels

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/06/20 14:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Andria Pichidi

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.