Apple.Inc

#Apple, the acclaimed American luxury technology company with a capitalization of $2.802 billion, is expected to announce its Q1 2022 “holiday earnings” report on Thursday, January 27 after the market close.

Apple is in the #3 “Hold” rank of Zacks within the computer industry range in the top 40% with position #102/#254 and in the TOP 38% with position #6/#16 within the sector.

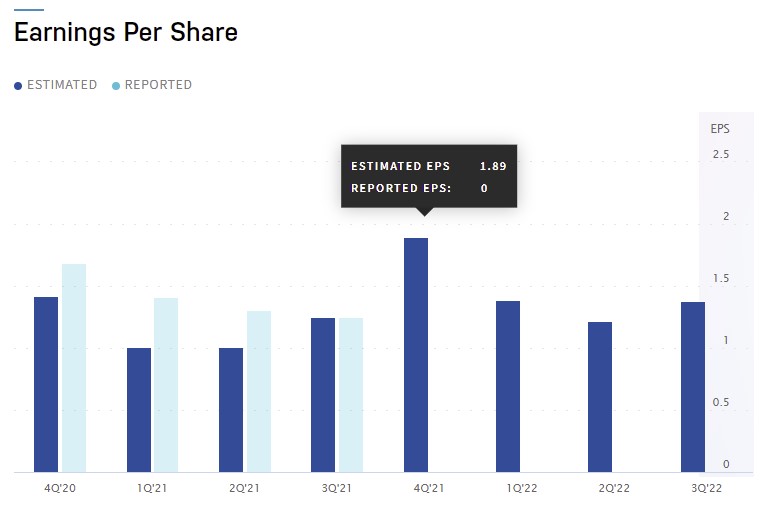

The report expects an EPS of $1.89 which would represent an annual growth of more than 12% from the $1.68 reported in the same quarter last year , although the most accurate EPS is at $1.94 with an ESP of 2.89%. Revenues are positioned at $118.43 billion, which would be a growth of 6.28% year-on-year.

“Apple expects strong year-over-year revenue growth ” – Tim Cook, Apple CEO.

Investors have a lot to weigh for this report and the current year. To start with, there is the great news that Apple will be the first company to reach $3 trillion in capitalization soon, thanks to the increased demand for products and services due to the pandemic ranging from the increase in home working to entertainment and consumer savings from virus lockdowns. Another piece of good news for this report is that it encompasses Apple’s very significant holiday purchases, estimated at 1.8 billion App Store users (mostly games) and a record daily spend of over $540 million for the new year, coupled with the expansion of the areas of Apple Pay, Apple TV, Apple Books, Apple Music and Apple Arcade. In addition, Apple announced the largest set of device launches in its history for the fall of this year, which includes 4 new iPhones (SE and version 14) with 5G technology, new versions of Airpods pro, iMac Pro, the new Mac pro, Macbook Air, Pro (completely redesigned for this summer) and a new mini version, the iPad Pro, 3 new Apple Watch, the implementation of its software such as iOS16-Sydney and macOS13-Rome as well as the rumor of the creation of products of virtual reality including headsets, which would open the doors to Apple within this relatively new segment; this was planned after the purchase of the virtual reality company NextVR.Inc, and there are rumors of the creation of a VR helmet.

Among the bad situations that the company faces is the constant doubt about the development of Covid (which has currently been increasing in virality but not in mortality) which in turn casts doubt on the recovery of the supply chain since the shortage of chips and semiconductors (industries that also face a struggle for supplies and skilled labor, mainly in Taiwan) has been a strong limitation for the manufacture of their products (mainly but not limited to Macbooks, iPhones and iPad minis) and therefore the delivery to consumers, who in some cases must wait up to 6 weeks to receive their item, which has caused Apple to lose more than $6 billion in revenue. Nor can we ignore the political issues between the US-China and antitrust laws, without forgetting that Apple’s production is still centralized in China.

All this raises the question of whether the new launches can be sustainable with the lack of chips, despite the transition that Apple is making from Intel chips to making their own silicon with ARM architecture, with their implementations in the current M1 Pro/Max and the arrival of the M2 expected this year.

Apple-H4

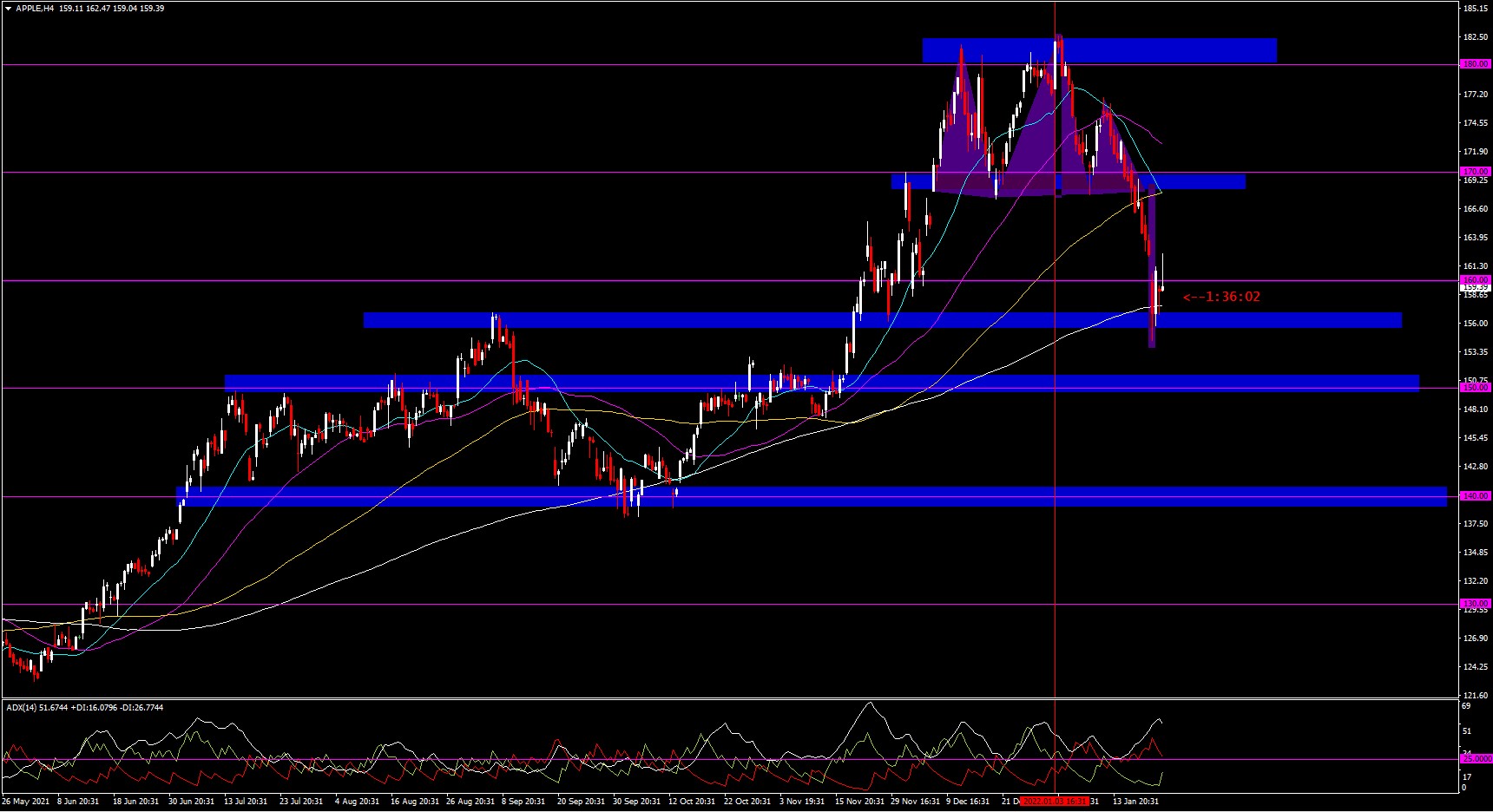

Apple shares had a strong bullish rally in October from the support of $140.00 to create two-month highs at $182.62. However, the price has fallen since the beginning of the year as after 3 tests and a false break they failed to hold above the $180.00 level making a test of lows and forming the head of a head & shoulders pattern in the price range from $182.33-$170.00. This was followed by the price pulling back to the 21-period SMA to form the second shoulder, and from here the price made a strong bearish push with its due pullback to the collarbone and launching the price to the target of the pattern at the 61.8% Fibo level of the upside momentum at $155.06, a move which tested the 200-period SMA where it bounced higher to the psychological price of $160.00.

The next major support aside from the 200-period SMA is in the range of the 78.6% Fibo levels at $147.57 to the psychological level of $150.00 and breaking that until the start of the momentum at the aforementioned lows. Regarding resistance, we have the psychological level of $160.00 which is being tested now, the 100-period SMA which is being pierced downwards by the 20-period SMA at $168.33 which is also equivalent to the 61.8% Fibo level of the bearish momentum and this close to the psychological level and ex-clavicle at $170.00.

ADX at 51.67 with a fatigue bias, with the +DI at 16.07 and -DI at 26.77 both heading to cross. Which could indicate a possible pullback to some resistance…to continue falling? or exceed the maximum? Perhaps the results will decide.

MasterCard Incorporated

#MasterCard Incorporated, the financial services multinational with a capitalization of $343,325B, is expected to announce its Q4-21 earnings on Thursday, January 27, before the market opens.

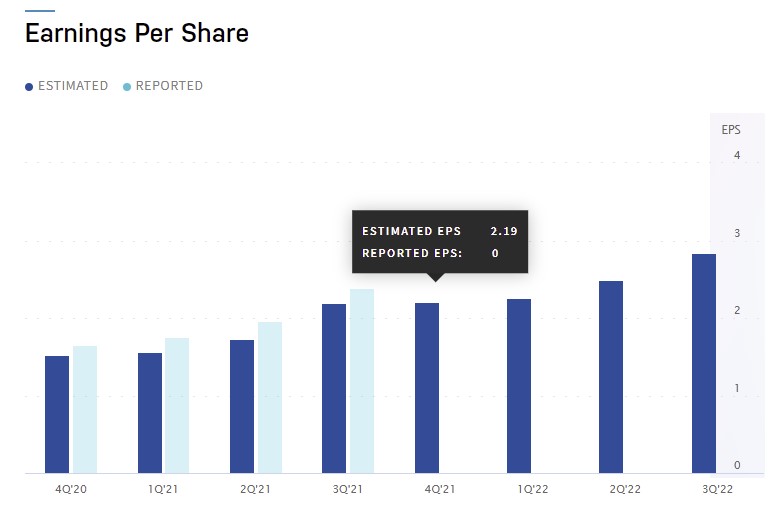

MasterCard is in the #3 Zacks “Hold” rank within the Financial Transaction Services industry rank in the Bottom 11% with position #226 / #254 and in the TOP 38% with position #6 / #16 within the business services sector. The report expects an EPS of $2.19, which would represent an annual growth of 32.9%, which was for the same quarter at $1.64, although the most accurate EPS is at $2.17 with an ESP of -0.91%. Revenues are positioned at $5.17 billion, which would be a growth of 25.5% year-on-year compared to $4.10 billion last year.

Mastercard has exceeded expectations in the last 4 quarters with an average above 10% which could give an idea that this quarter will also exceed it because it covers the holiday season, travel and Christmas shopping that represent up to 1/4 part of your income. However, if we look at the ESP for this quarter, it is not positive, which casts doubt on this theory.

We can expect an improvement in MasterCard due to the holiday season and the relaxation of the restrictions of the sanitary measures in 2021 due to Covid-19 and the massive vaccination campaign worldwide, which in turn increased consumer spending as well as retail sales thanks to personal savings from lockdowns and pent-up demand for goods (which still exists due to supply chain crises). This being so, it is logical to think of the increase in transactions that MasterCard presented, which is estimated at an increase of 24.9% year-on-year. On the other hand, cross-border spending returned to pre-pandemic levels in the last quarter. However, Nasdaq expects operating costs as well as rebates and incentives along with advertising, marketing and data processing costs to have increased. In addition to the recent acquisitions that have helped to grow in the market and create new sources of income, such as the acceleration in the use of electronic payments thanks to the pandemic, forcing a change towards a mostly digital model, including the latest addition to its products and services (but not only) is a Mastercard Track Instant Pay virtual card for fast and seamless business payments powered by Mastercard Track Business Payment Service B2B network, said card is created using AI machine learning capabilities and data science by automating business processes reducing time, costs and with an increase in efficiency, this implementation is already available in the US and with plans for international expansion. All these efforts in partnerships with strong organizations and investment to benefit B2B payments and facilitate everything globally.

In other news, the MasterCard board approved the repurchase of shares, thinking that they are undervalued, since November authorizing the repurchase of $8 billion in shares on the open market, which would be up to 2.5% of its total shares. In addition to this, the majority shareholder of MasterCard sold almost 91k shares of capital stock at an average price of $315.30 for a profit of $28,690,408.20 in December. Additionally, MasterCard CEO Michael Mieback sold 10,670 shares at an average price of $370.00, for a total of $3,947,900.00. It is estimated that a total of almost 650k shares of the company have already been sold for a value of $214,977,545.

Mastercard, H4

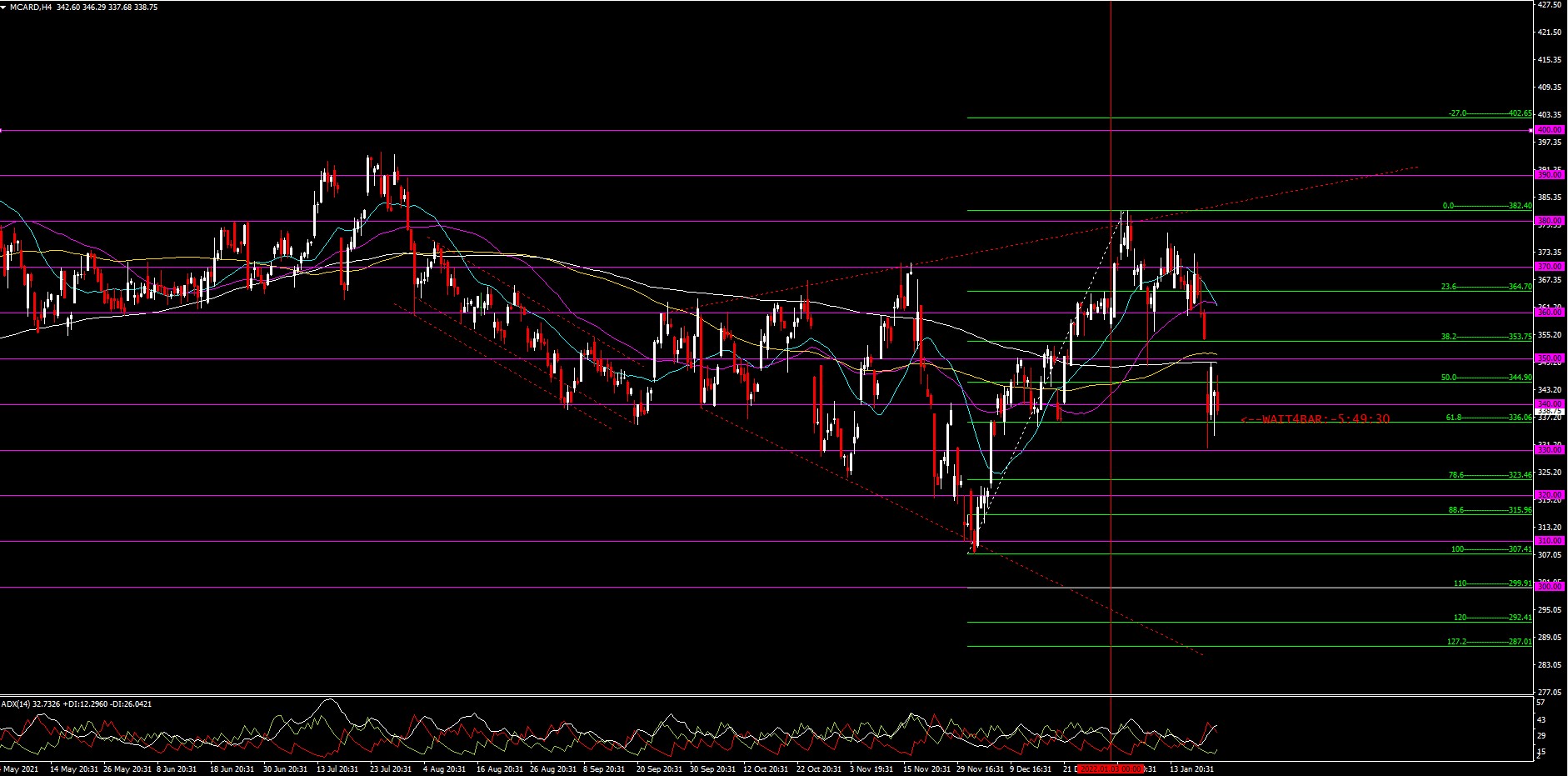

MasterCard started in September an expansive triangle that has oscillated around the $350.00 level and that, until the last bullish impulse, has expanded from the support of $310.00 with lows at $307.41 to leave highs at $382.40 without managing to close the candle above $380.00. From there, the price has marked a high failure from the beginning of this year, from there it has fallen to test the $330.00 level but closing the candle above $340.00 which is currently being tested, piercing the moving average of 20 periods, 200 periods, the last two moving averages pierced or rather jumped, are the one of 50 periods and 100 periods that has jumped the price thanks to a gap that goes from $353.75 to the moving average of 100 periods just below of the $350.00 which is still open. If the expansion continues, the next low should be close to $310.00-$300.00 and the next high in the range of $390.00-$400.00, with the $350 level being the central orbit of the price.

ADX is at 24.45 with an upward bias, +Di at 14.67 and -DI at 29.13, which would mark the start of a downtrend. Where will the price launch the results?

Visa.Inc

#Visa, the other best-known financial services multinational, with a capitalization of $388.63B, is expected to announce its Q1-22 report on Thursday, January 27 after the market close.

Visa is in the #3 Zacks “Hold” rank within the Financial Transaction Services industry rank in the Bottom 11% with position #227 / #254 and in the TOP 44% with position #7 / #16 within the business services sector. The report expects an EPS of $1.69 with an ESP of 0.27% which would represent an annual growth of more than 19% that was priced at $1.42 for Q1-21. Revenue is expected at $6.79 billion, which would be a growth of 19.34% year-over-year. Visa has had 6 consecutive quarters of growth. Will this be the seventh?

Visa, like MasterCard, has benefited for almost the same reasons and has made almost the same movements, from taking advantage of the gradual reactivation of the pandemic, the improvement in consumer spending, the holiday and Christmas season, as well as adaptation to digital payments thanks to reliability and security in the face of the pandemic. In addition to the recovery in US domestic spending to pre-pandemic levels that represent almost half of visa payment volumes and a 23% year-on-year increase in card purchases.

The Zacks Consensus for total volume (cash + payments) is pegged at $3.578 billion which is an increase of 12.58% YoY. Transactions processed have also benefited for the same reasons with $47,183 million/+20% year-on-year and are expected to grow 19.3% in the first quarter. Like MasterCard, Visa has also had significant spending on technology investments that have strengthened its position in the market, as well as acquisitions and alliances with other companies.

“profits could be substantially higher if international tourism were to fully recover” – James Faucette, Morgan Stanley.

Visa has seen a recovery in consumer spending in recent quarters, but Visa CEO Vasant Prabhu cites the easing of restrictions in Asia as a key variable for domestic and cross-border spending, the latter in contrast to Mastercard, Visa are at 85% (except in Europe) of pre-pandemic levels in the last quarter and growth is expected in the first quarter of 26.5%. In addition, a worldwide growth of total volume of payments of 15.2%. However, for Visa, the decline in cash volume in Asia Pacific and Europe in addition to high operating expenses and incentives for clients, may weigh on it.

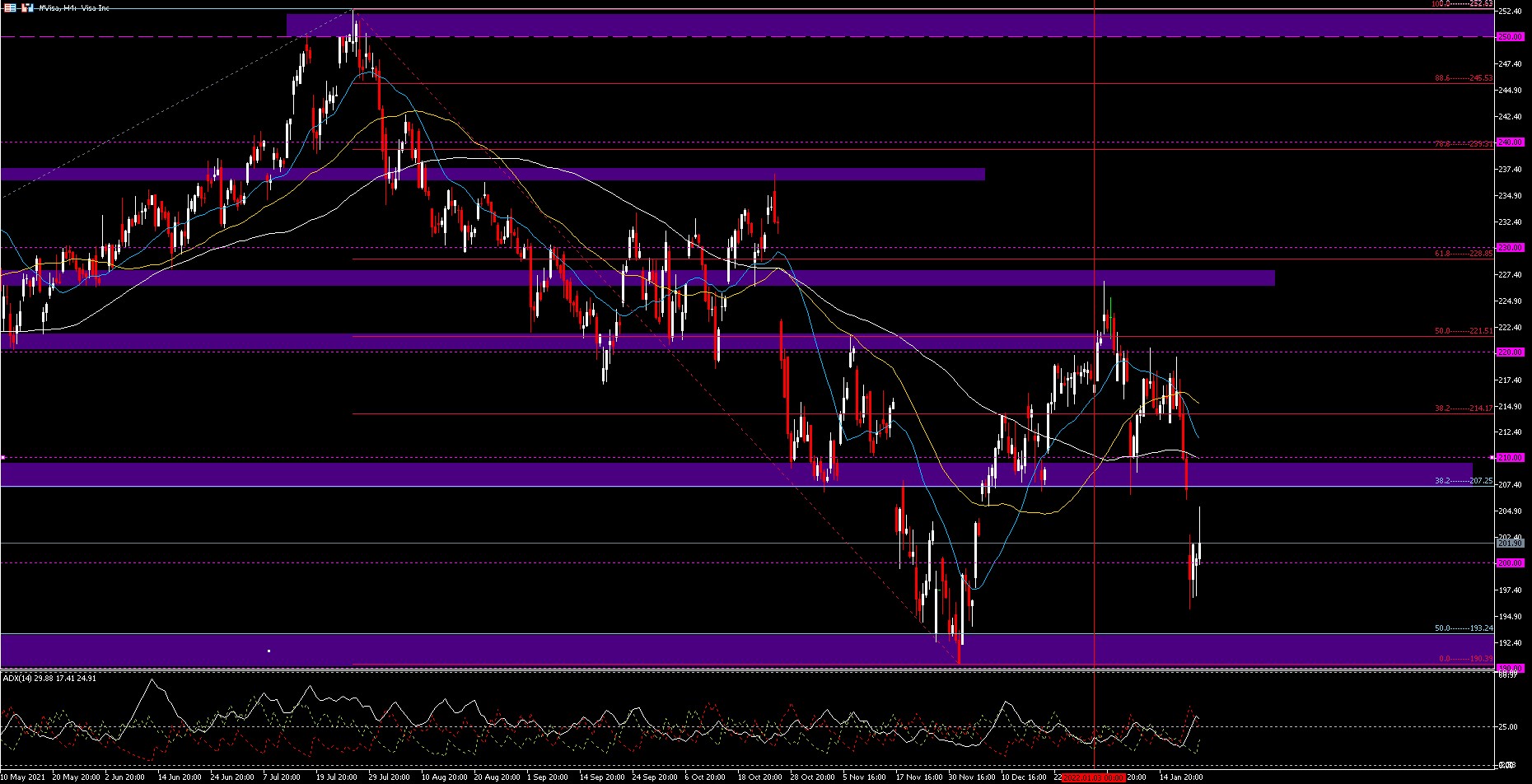

VISA, H4

Visa has posted a strong bullish rally since March 2020, going from lows of $133.84 to record highs of $252.63 during July 2021, we are currently in a pullback that is below the 38.2% level of this momentum with a test of support which goes from the 50% Fibo level at $193.24 to the psychological level of $190.00.

Price has rebounded since this test marking the aforementioned low ending the bearish momentum and pulling back above the 50% Fibo level marking a high at $226.63, forming a kind of crown pattern, with collarbone at the 38.2% level. bullish momentum, which was broken down by a gap that jumped the price from $207.00 to $200.73 and then fell to test the psychological level of $200.00 which is still currently being tested.

We have supports at the lows of $190.00 and if we break them we would fall to the October lows that are at the psychological level of $180.00. If we fall, we would be talking about going down to 78.6% Fibo levels at $159.26, just below the psychological level of $160.00. The resistances are at the 38.2 Fibo that sees from $207.25 to the psychological level of $210.00, the 38.2 Fibo of the bearish momentum at 214.17 and even at the aforementioned highs of $226.00, which if broken we would look for the range of the 61.8% level of $228.85 to the level psychological price of $230.00, which would be the maximum for October.

ADX at 29.88 with an upward bias, +DI at 17.41 -DI at 29.91, which would mark the start or resumption of the downtrend.

Aldo Zapien.

Market Analyst – HF Educational Office – México

Fuentes:

Apple

- https://www.zacks.com/stock/quote/AAPL

- https://www.nasdaq.com/es/market-activity/stocks/aapl

- https://www.bloomberg.com/news/newsletters/2022-01-02/what-s-apple-aapl-releasing-in-2022-iphone-14-airpods-pro-2-imac-pro-ipads-kxxmcej5?cmpid=BBD012322_POWERON&utm_medium=email&utm_source=newsletter&utm_term=220123&utm_campaign=poweron

- https://9to5mac.com/2022/01/24/apple-supply-constraints-continue-ahead-of-q1-2022-earnings-report-on-thursday/

- https://www.techspot.com/news/88200-apple-app-store-saw-18-billion-spending-during.html

- https://www.wsj.com/articles/apple-buys-virtual-reality-streaming-upstart-nextvr-11589503071?mod=article_inline

- https://www.wsj.com/articles/chip-makers-contend-for-talent-as-industry-faces-labor-shortage-11641124802?mod=djemalertNEWS

- https://www.bloomberg.com/news/articles/2021-05-18/apple-readies-macbook-pro-macbook-air-revamps-with-faster-chips?sref=9hGJlFio

- https://9to5mac.com/2022/01/23/gurman-apple-preparing-to-launch-its-widest-array-of-new-products-ever-this-fall/

Mastercard

- https://www.zacks.com/stock/quote/MA

- https://www.nasdaq.com/es/market-activity/stocks/ma/earnings

- https://www.nasdaq.com/articles/can-rising-operating-costs-hurt-mastercard-ma-q4-earnings

- https://www.nasdaq.com/articles/mastercard-ma-earnings-expected-to-grow%3A-what-to-know-ahead-of-next-weeks-release

- https://www.marketbeat.com/instant-alerts/nyse-ma-earnings-date-2022-01-2-3/

- https://www.nasdaq.com/articles/earnings-season-scorecard-and-analyst-reports-for-mastercard-pfizer-citigroup

- https://www.zacks.com/stock/news/1857113/mastercard-ma-unveils-solution-to-speed-up-supplier-payments?art_rec=quote-stock_overview-zacks_news-ID01-txt-1857113

Visa