- After records for Equities (440 of S&P500 have reported so far & Q3 Earnings up 41% overall) & a 1-yr high for USDIndex to conclude a huge data week, news flow over the weekend weighs on markets to start the trading week.

- Tesla CEO Musk, via a Twitter poll, asked if he should sell a 10% stake (USD 21bln) in Tesla; 57.9% voted “Yes” with over 3.5mln total votes.

- US House voted to pass $1.2tln bipartisan infrastructure bill late on Friday & sent it to President Biden for signing.

- Chinese trade data showed a larger-than-expected trade surplus & strong exports, but USD-denominated imports missed estimates.

- Some China Evergrande unit offshore bondholders have not received interest payments due Saturday.

- UK reportedly prepared to trigger Article 16 of NI agreement & ditch customs checks before Christmas, EU sticking to deal.

———————————————————————————————

- USD (USDIndex 94.22) down from Friday’s 1-yr high 94.62 – post NFP – holds the bid.

- US Yields (10yr crashed into close at 1.453) lifted a tad overnight to 1.46%.

- Equities at all-time highs Friday – USA500 +17 (+0.37%) at 4697 (DOW -0.75%) – Big movers – PFE +10.86%, AirBnB +12.98%, DIS +3.14% – USA500.F back to 4683. Asian equities weaker.

- USOil – bounced Friday from Thursday’s low at $77.15 – rallied again today as ARAMCO increases prices – trading back to $81.00 now from $79.75 close on Friday.

- Gold recovers further from Friday’s breach & break of $1800 as yields remain weak. Touched $1820 today back to $1816 now.

- FX markets – EURUSD 1.1550, Cable 1.3478, USDJPY now 113.57.

European Open The December 10-year Bund future is down 9 ticks, U.S. futures are also losing ground. Markets are still finding a new equilibrium after central banks did their best to slap down overblown tightening expectations for the coming years last week. ECB’s Lane in an interview with a Spain’s El Pais also argued again that the current spike in prices will be temporary and that the central bank should not overreact, as inflation is still projected to undershoot target in the medium term. The DAX and FTSE 100 futures are currently down -0.2% and -0.1% respectively, with a -0.4% correction in the NASDAQ leading US futures lower.

Week Ahead – All about inflation data this week, with FED (and most other CBs) behind the curve – will they have to do more, more quickly, or are they correct in their assessment of the “transitory” nature of inflation? A plethora of central bankers will have the platform this week – kicking off today with 4 from the Fed.

Today – EZ Sentix Index, Fed’s Powell, Evans, Harker, Montgomery; ECB’s Lane

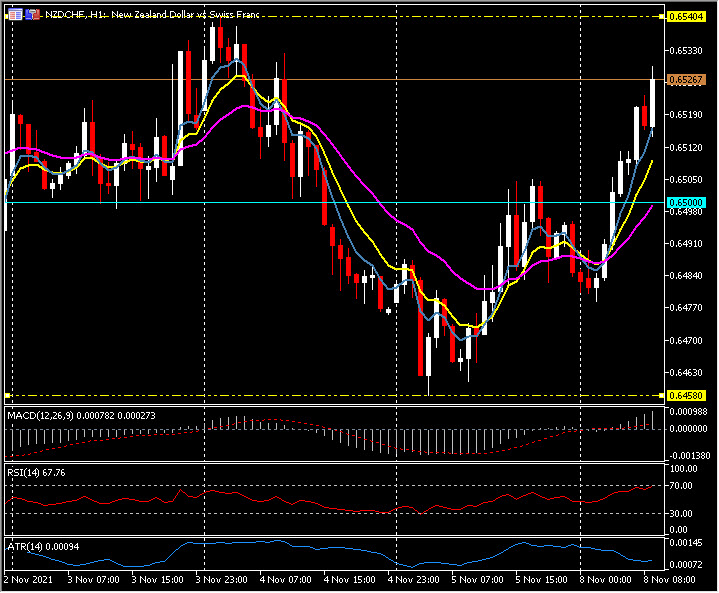

Biggest FX Mover @ (07:30 GMT) NZDCHF (+0.63%) Recovering from Friday low at 0.6460 continues. Strong move over 0.6500 today to test 0.6530. Faster MAs aligned higher, MACD signal line & histogram rising& over 0 line, RSI 67 & rising. H1 ATR 0.0010, Daily ATR 0.0052.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.