- USD (USDIndex 93.89) – first rate hike was pushed up to June, with two quarter point tightenings priced in for 2022. Wall Street firmed too on the back of strong earnings with more new record highs on the USA500 and the USA30. Also underpinning sentiment are expectations that the fiscal package will make it out of Congress.

- Fed Chair Powell warned that inflation could be higher and more persistent than previously expected.

- US Yields – 10yr backed up 0.9 bp overnight to 1.64%.

- Equities mixed – USA100 paced the advances though, climbing 0.9% amid support from the slip in yields – 4582. USA100 bounced to 15602.

- Facebook reported mixed third quarter earnings on Monday, slightly missing revenue estimates but continuing to grow its user base. FB +2%.

- TSLA (+12.6%) joins the$1 trillion market cap group after 11 yrs – took AMZN 22 yrs. It’s bigger than the combined value of the next 9 biggest car makers but it sells less than 1% of world car sales. Elon Mush added $36BN to his net wealth yesterday alone. UBS beats on revenue – but sales are mixed.

- USOil holds up again on supply concerns & trades close to 7-year highs at $82.50.

- Gold spiked at $1808.

- FX markets – EURUSD 1.1600, Cable bounced 1.3778, USDJPY – reversed from 113.97 highs to PP at 113.86.

European Open The December 10-year Bund future is down -20 ticks at 168.45, underperforming versus US futures, although in cash markets the US 10-year rate is down from overnight highs, but still up 0.4 bp at 1.63%, as a 0.5% gain in the USA100 is leading US stock futures higher. GER30 and UK100 are posting gains of 0.2% and 0.1% at the moment, after a somewhat mixed session across Asia.

Today – Upcoming central bank decisions will remain in focus, with ECB and BoJ set to announce their decisions on Thursday. Earnings: Microsoft, Alphabet, Visa, Eli Lilly, Novartis, Twitter, General electric, UBS, Robinhood. Today’s economic calendar will be of interest as well, and features October consumer confidence and September new home sales.

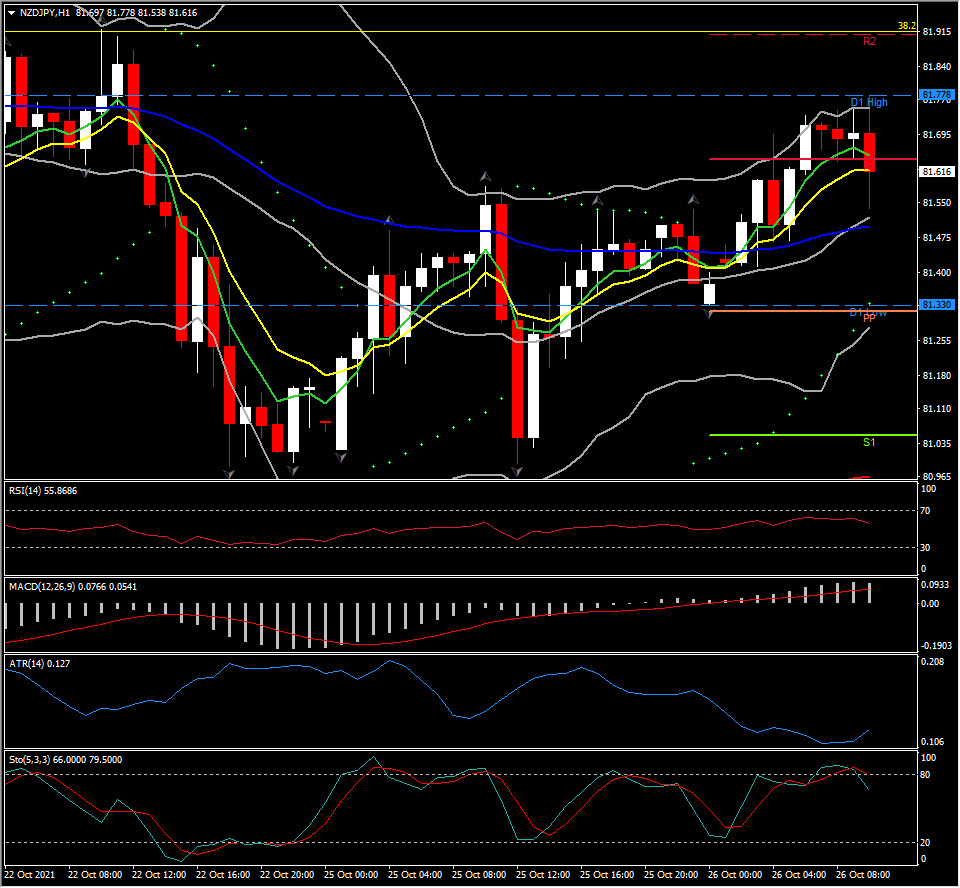

Biggest FX Mover @ (06:30 GMT) NZDJPY (-0.28%) Reversed overnight gains from 81.88 high tp currently 81.50 area. Faster MAs, RSI & Stochastic turned lower, while in contrast MACD signal line & histogram keep rising, implying to a potential limited pullback.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.