Market News Today – US Equities closed at new all-time highs, (Service PMIs at record, TSLA beats delivery targets – shares up +4%) USD and 10-yr yields cool. No change to rates (0.1%), bond buying or outlook from RBA, AUD unfazed. Yellen suggests global minimum tax rate, Credit Suisse announces $4.7bn hit from Archegos margin call. Overnight JPY earnings better, spending worse, CNY Services PMIs beat. UK shops pubs & restaurants open from April 12, NZ-Aus flight corridor April 19. Globally 658 million vaccines administered across 151 countries. The EU vaccine roll-out and new infections in India & Brazil remain areas of concern.

RBA – Governor Lowe stressed that the “board is committed to maintaining highly supportive monetary policy conditions until its goals are achieved” and that the cash rate won’t rise “until actual inflation is sustainably within the 2-3% target range”. “For this to occur, wages growth will have to be materially higher than it is currently”. At the same time, Lowe warned that “given the environment of rising housing prices and low interest rates, the bank will be monitoring trends in housing borrowing carefully and it is important that lending standards are maintained”. AUD house prices increased the most since 1988 in February.

Week Ahead – RBA (6th) EU PMIs & FOMC Minutes (7th), ECB Minutes, Weekly Claims & Powell speech (8th), CAD Jobs & US PPI (9th).

The Dollar has found its feet after taking a tumble in thin markets yesterday. The bullish case for the Dollar remains strong, given the outsized fiscal stimulus coursing through the US economy alongside the relatively advanced states of Covid vaccination progress in the US and likelihood for further widening in the US Treasury yield differential versus peers. The March jobs report was a blowout, while the ISM services index surged to a record peak. Wall Street also scaled to new record highs yesterday. The only blot on the bullish dollar landscape is the uber accommodative stance of the Fed, which has been downplaying the scope for runaway inflation risks, although the relatively high Treasury yields, among low- and sub-zero yielding peers, will offset this. The USDIndex has lifted to the upper 92.0s after yesterday posting a 12-day low at 92.52. EURUSD has concurrently tested the waters below 1.1800 after making a 12-day peak at 1.1820. USDJPY has lifted back above 110.00. AUDUSD has dropped back from one-week highs, while Cable has tipped back under 1.3900 after earlier pegging an 18-day high at 1.3920. The Pound yesterday printed a 14-month high versus the Euro, which although occurring in holiday-thinned trading reflects the contrasting fortunes of the reopening UK economy with the re-restricted economies across the Channel. The rate of new Covid cases is now 4% of what it was at the peak seen in early January, despite a more than doubling in testing over that time, while the death rate is less than 3% of what it was at the highs.

Today – EZ unemployment, ECB asset purchases, US JOLTS.

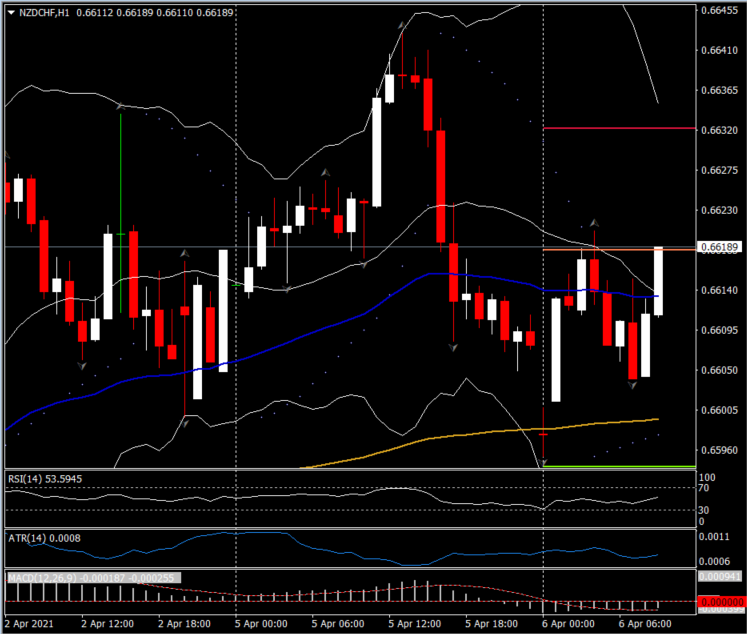

Biggest (FX) Mover @ (07:30 GMT) NZDCHF (+0.20%) rallied from test of 200MA on open, (0.6600) to PP at 0.6620 and over 50 MA. Yesterday declined from 0.6645 high. Faster MAs remain aligned higher, RSI 53 and rising, MACD histogram & signal line aligned higher but under 0 line from open after yesterday’s fall. Stochs rising. H1 ATR 0.0008 Daily ATR 0.0046.

Click here to access the HotForex Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.