Once again the FAANGs excluding Netflix plan to report their earnings the same day within 30 minutes of each other. FAANGs illustrate 20% of the S&P500’s total value. Even though most of them face increasing antitrust scrutiny, all posted an impressive rally this year as their shares have surged and sustained close to record highs as the pandemic reckoned with online services such as shopping, streaming, clouds.

Hence in addition to our earnings articles, today we will focus also on Alphabet’s third quarter earnings for 2020 which will be reported along with the rest of the giants. Just a quick reminder, Alphabet Inc. is a holding company and Google’s parent company. The company’s businesses include Google Inc. (which is the largest one) and its Internet products, such as Access, Calico, CapitalG, GV, Nest, Verily, Waymo and X. The company’s segments include Google and Other Bets.

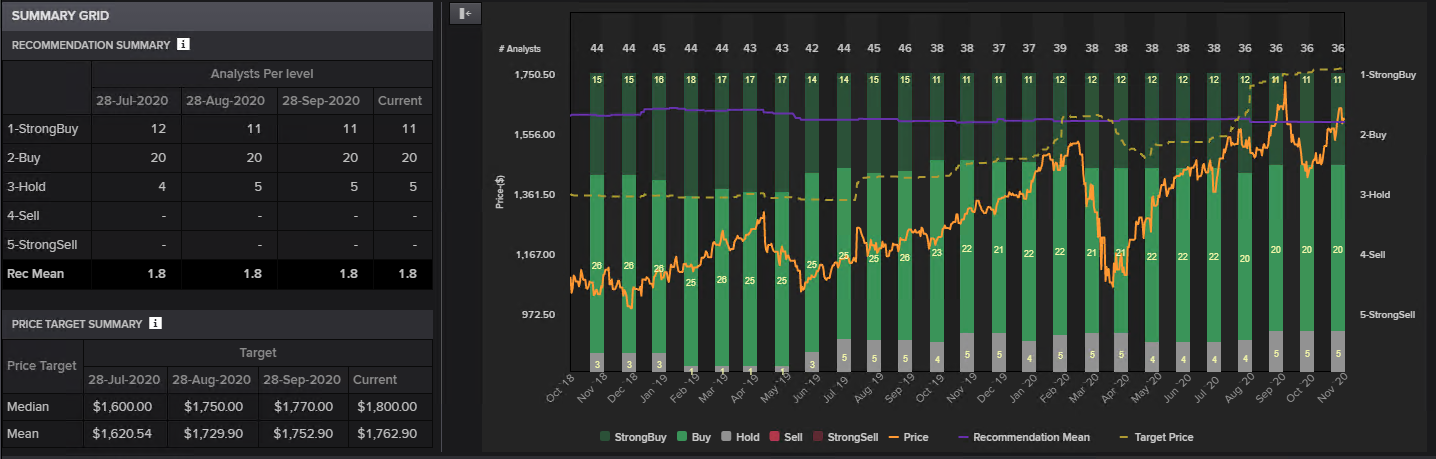

Alphabet’s report will be key after its first year-over-year revenue decline in company history in Q2 as a result of the lack of advertisement demand from the majority of businesses amid the economic slowdown globally. However the forecasts for Q3 have the company well positioned with the consensus recommendation “strong buy”, corresponding to the majority of the consensus recommendation from Reuters Eikon, as 31 out of 37 analyst firms recommend “buy” and “strong buy”, while only 5 recommend ‘hold’. Hence, no analyst firm is making a “sell” or “underperform” recommendation for the company.

| 1 Year | 3 Year | 5 Year | |

|---|---|---|---|

| Sales % | 18.30 | 21.49 | 19.65 |

| EPS (TTM) % | 12.49 | 20.82 | 19.92 |

| Dividend % | — | — | — |

According to Zacks Investment Research and Reuters Refinitiv, the information service is expected to have $11.33 in earnings per share during the third quarter of 2020, which represents a yearly rise of 12% since the reported EPS for the fiscal quarter ending September 2019. Focus should also turn onto the revenues number which is projected to hit a 6% yoy spike, to around $42.8 billion, from the $40.49 billion reported last year. Net sales meanwhile are seen at $35.26 billion.

- Google Search & Other (ad revenue, dominated by Google Search) – consensus of $24.96 billion*

- YouTube ads – consensus of $4.38 billion*

- Google Network (ad sales on third-party websites/apps) – consensus of $5.07 billion (down 4%)

- Google Cloud – consensus of $3.32 billion*

- Google Other (Play Store, hardware, YouTube subscriptions) – consensus of $5.11 billion*

- Other Bets (Google Fiber, Verily, Waymo, etc.) – consensus of $153 million (down 1%)

Despite the huge diversification of its portfolio, Alphabet Inc earns nearly 71% of its revenue from advertising. Hence even though, the travel sector is still weak the majority of the analysts remain bullish on the advertisement services of Alphabet into Q3 given the slightly ‘temporary as it seems’ recovery that we have seen as the pandemic eased over the summer and business began reopening. Morgan Stanley stated also that they came into earnings season positive about the online ad market recovery but grew more optimistic following Snap’s blowout ad revenue beat and better-than-expected ad results from Verizon subsidiary AOL, Sirius-owned Pandora, and Interpublic Group.

The positive consensus for Q3 could also be driven by the shift of Alphabet to Google Play and YouTube to help its partners support their businesses. The majority of the analysts believe that we could see strength in YouTube ad pricing and the return of brand spending in its channel checks.

Alphabet CEO Sundar Pichai however highlighted in his latest statements GOOGL’s focus on non-advertising segments. Like tech giant and its cloudspace rival Microsoft Corporation (NASDAQ: MSFT), GOOGL has the capacity and resources to strategically pivot, from a large “legacy” company to an aggressive emergent; in this case, from search to various ‘other segments’ offering potential growth.

Meanwhile, the risks that Alphabet faces ahead of the report is the solid competition from Amazon in advertising business and cloud services but also the cold headwinds on the earnings front in addition to emerging regulatory challenges. Coming off a not-so-stellar Q1 reporting season, GOOGL fell short in Q2, reporting its first ever year-over-year quarterly decline.

Earlier this week, the Justice Department, along with 11 Republican state attorneys general, filed an antitrust lawsuit against Google, alleging an unlawful monopoly on search services and advertising. US Deputy Attorney General Jeffrey Rosen called GOOGL, “the gateway to the internet” and said the company “has maintained its monopoly power through exclusionary practices that are harmful to competition.”

At this stage, we have to point out that a consensus recommendation, similarly to economic data forecasts, has a significant effect on the near-term stock price, as it represents a company’s wealth picture. Hence on every earning report, stock price is highly influenced by the comparison between the outcome and the expectations. The market tends to react positively if the outcome comes in better or at least in line with the forecast, while the price moves lower if the reported earnings miss expectations.

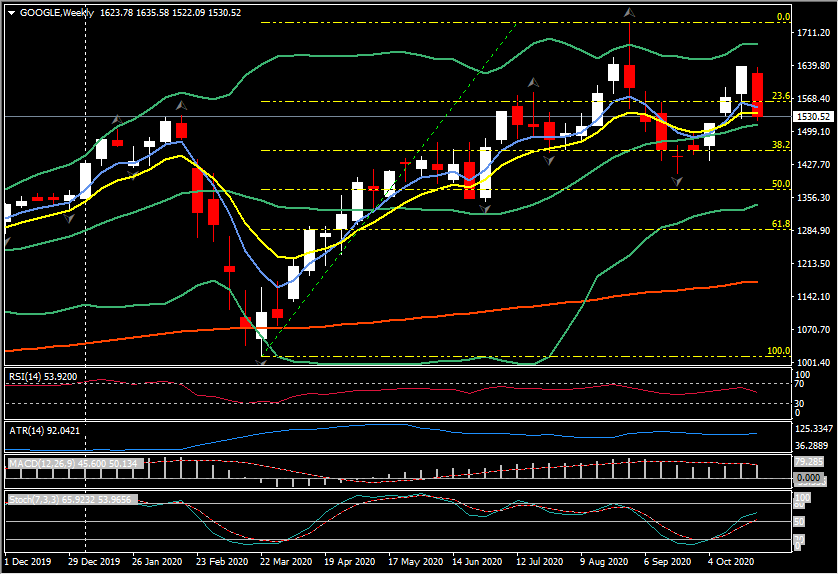

Technically, the current Google price action has posted a sharp rally since the March panic with the stock rebounding from the $1,000 area to record highs at $1,732.41. Currently the asset is traded at the $1,524 area which is just a 23.6% loss from all-years highs. The overall bias remains strongly positive even though medium term momentum indicators signal a potential pullback lower.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.