FX News Today

- German industrial production better than expected at 0.3% m/m. The unexpected expansion in August comes despite ongoing contraction in orders and a deterioration in business sentiment.

- European Outlook: European stock markets closed with broad gains, despite mounting signs that U.K. PM Johnson is positioning for a failure in Brexit talks with the EU, which shouldn’t come as a surprise, but makes the risk of a no-deal scenario ever more tangible as Johnson lays the ground for a “people-versus-parliament” election. European stock futures are moving higher in tandem with U.S. futures after a positive session in Asia.

- World Bank warns Brexit, European recession will hit world growth; The head of the World Bank warned global growth could come in lower than the 2.6% predicted in June amid “Brexit, Europe’s recession and trade uncertainty”.

Charts of the day

Technician’s Corner

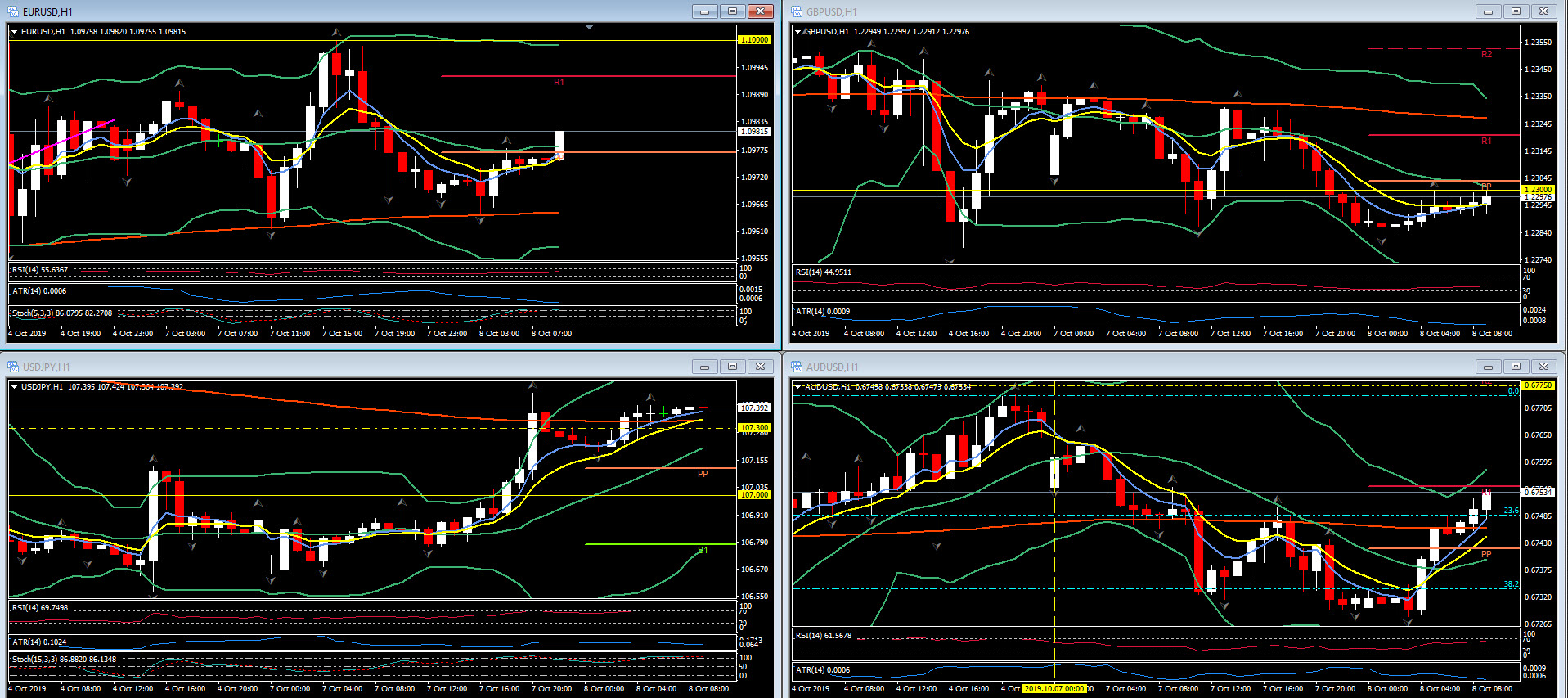

- EURUSD traded sideways through the NY morning session, ranging between 1.0982 and near two-week highs of 1.1000, in the Asian session the pair fell back to 1.0966. The Dollar overall appears to be showing signs of peaking, with incoming U.S. data last week showing significant indications of economic slowing. Europe has its own growth issues as well of course, though with markets pricing in another Fed rate cut at the end of October, EURUSD may have some room to run to the upside in the coming sessions.

- USDJPY topped at 107.07 in US session following comments from White House advisor Kudlow, who said that a US-China deal was possible and negotiators could make progress this week, and Washington is open to looking at China’s proposals. The comments came after China over the weekend indicated it is not open to a broad scale trade agreement. USD strength continued overnight with the pair touching 107.44.

Main Macro Events Today

- Producer Price Index (USD, GMT 12:30) – The Headline PPI is expected to drop at -0.2% for September, with a 0.2% rise in the core index. As expected readings would result in a y/y gain of 1.5% for headline PPI, versus a 1.8% pace of August. We see y/y headline readings in a 1.0%-2.3% range over coming months, while core prices should oscillate in a 2.0%-2.5% range.

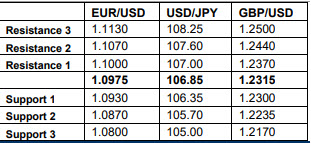

Support and Resistance levels

Click here to access the Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.