FX News Today

- Treasury yields slip along with core EGBs after BoJ and looking to 25 bp Fed cut and dovish stance.

- BoJ kept policy on hold but promised to act aggressively with additional easing measures if its policy goals are threatened.

- European stock futures are marginally higher, alongside gains in US futures after a largely positive session for stocks in Asia.

- US-Sino trade talks resume today.

- In Europe, a no-deal Brexit scenario is looking increasingly certain as the new PM in London steps up the hostile rhetoric and focuses on selling no-deal at home, while showing no interest in re-opening the lines of communication with Brussels.

- GBP losses accelerated on no-deal Brexit risk; hit major trend lows vs USD and others.

- The WTI future lifted to USD 57.20 per barrel.

- German GfK consumer confidence fell back to 9.7 in the advance August reading. With no improvement in manufacturing the improvements on the German labour market are running out of steam and ultimately that will also impact consumption going down the line.

Charts of the Day

Technician’s Corner

- USDJPY: The Yen has firmed moderately in the wake of the BoJ policy announcement. Market narratives have mostly taken the view that the central bank was a little less dovish than expected, especially with both the Fed and ECB heading to rate cuts. USDJPY drifted to near 108.50 from a 3-week high that was seen ahead of the data, following disappointing industrial production figures out of Japan, at 108.94. EURJPY and other Yen crosses saw a similar fall-from-highs price action. The BoJ kept its short-term interest rate target at -0.1% and its pledge to guide 10-year JGB yields around 0% while maintaining its asset buying programme. The central bank signalled its commitment to keep interest rates at current levels “for an extended period of time, at least through around spring 2020,” commenting that “the momentum for achieving 2% inflation is sustained, but lacks strength.” The forward guidance was pretty much unchanged from existing guidance, which seemed to cause a modicum of disappointment in forex markets, though JGB yields still dipped while the JPN225 closed with a 0.4% gain on the day. Overall, the balance of risks for USDJPY and EURJPY seem to the downside, with both the Fed and ECB having much more room to add monetary stimulus than in the case of the BoJ.

Main Macro Events Today

- Harmonized Index of Consumer Prices (EUR, GMT 12:00) – The German HICP inflation is expected to slip back to 1.3% y/y for July after it was revised up to 1.5% y/y in June.

- Consumer confidence (USD, GMT 14:00) – Consumer confidence is expected to bounce to 128.0 in July from 121.5 in June, versus another 16-month low of 121.7 as recently as January and an 18-year high of 137.9 in October. Overall, confidence measures remain historically high.

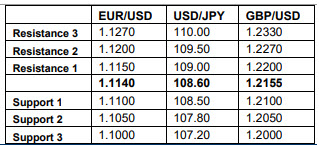

Support and Resistance levels

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.