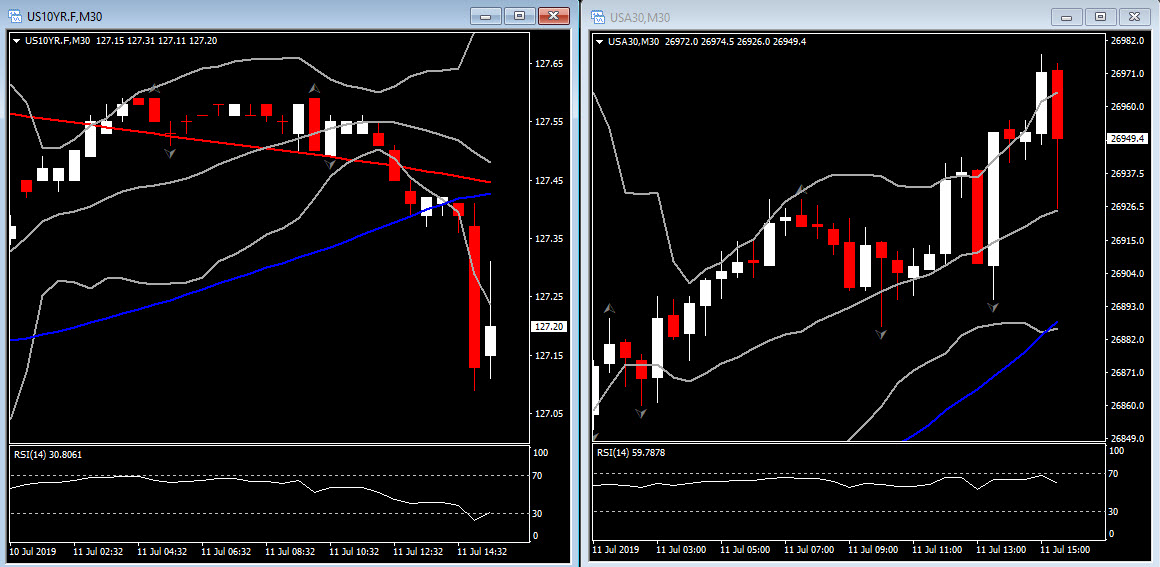

Treasury yields spiked on the stronger than expected CPI and jobless claims data, but have already slipped from the highs. The 2-year rate, more sensitive to the Fed outlook, jumped to 1.858%, but has dipped back to 1.832%. The 10-year ran up to 2.09% and is back to 2.073%. Meanwhile, US equities continue to extend yesterday’s gains, as the market basks in the glow of Chair Powell’s appearance yesterday. The USA30 is leading the way with a 0.3% increase, the USA500 has risen 0.1% and the USA100 is also up 0.1% in pre-market trading.

The market is still pricing in a 25 bp rate cut at the end of the month.

The Dollar rallied following the mix of data, where CPI was slightly warmer than expected, and jobless claims came in below consensus. USDJPY headed to 108.32 highs from near 108.05, as EURUSD dipped to 1.1265 from 1.1280. Meanwhile, Pound and Kiwi remain the biggest gainers so far against US Dollar.

Cable is showing the biggest movement on the day out of the Dollar pairings, presently a little off highs but still showing a 0.5% gain. The move reflects about half general Pound firmness and about half general Dollar weakness. A 4bp-plus rise in the 10-year Gilt yield, taking it back above the prevailing 0.75% repo rate, has been concomitant with Sterling’s ascent today. BoE Governor Carney reaffirmed earlier that UK banks would be able to withstand a no-deal Brexit scenario (which still warns of material economic disruption in such an eventuality).

GBPUSD posted a 6-day peak at 1.2571, extending the rebound from the 27-month low seen earlier in the week at 1.2439. On the break of the 3-session Resistance at 1.2571, GBPUSD could face Resistance at 1.2590-1.2600 area. GBPUSD has support at 1.2520-1.2530.

US Data Review

US initial jobless claims dropped 13k to 209k in the July 5 week after falling 7k to 222k in the June 29 week (revised from 221k). The bigger than forecast decline was likely impacted by the July 4 holiday. The 4-week moving average fell to 219.25k from 222.5k. Continuing claims climbed 27k to 1,723k in the week ended June 29, after rising 2k to 1,686k in the week ended June 22. The initial claims number is better than projected, consistent with the strength seen in the June jobs report.

US CPI rose 0.1% in June, while the core rose 0.3%, hotter than expected. There were no revisions to the 0.1% gains in May. On a 12-month basis, headline prices slowed to a 1.6% y/y pace versus 1.8% y/y, and excluding food and energy, the pace increased to 2.1% y/y versus 2.0% y/y. There was strength in apparel prices which climbed 1.1% following unchanged. Housing costs rose 0.3% versus the prior 0.1% gain, with medical care up 0.3% too, as it did in May. Services rose 0.2% versus 0.1%. Food/beverage prices edged up 0.1% after a prior 0.3% gain. Energy prices dropped 2.3% versus -0.6%, while transportation costs slid -0.7% from -0.3%. Commodities were down -0.2% from unchanged.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.