- Economists expect inflation to rise from 3.2% to 3.4%, but the monthly incline to be lower than the previous month.

- The Dow Jones sees its worst week of 2024, but stocks rebound on positive employment data.

- The US economy added a further 303,000 more employed individuals and the unemployment rate fell to 3.8%.

- The US Dollar witnesses “mixed” price movement as investors wait for inflation confirmation and clarity on interest rates.

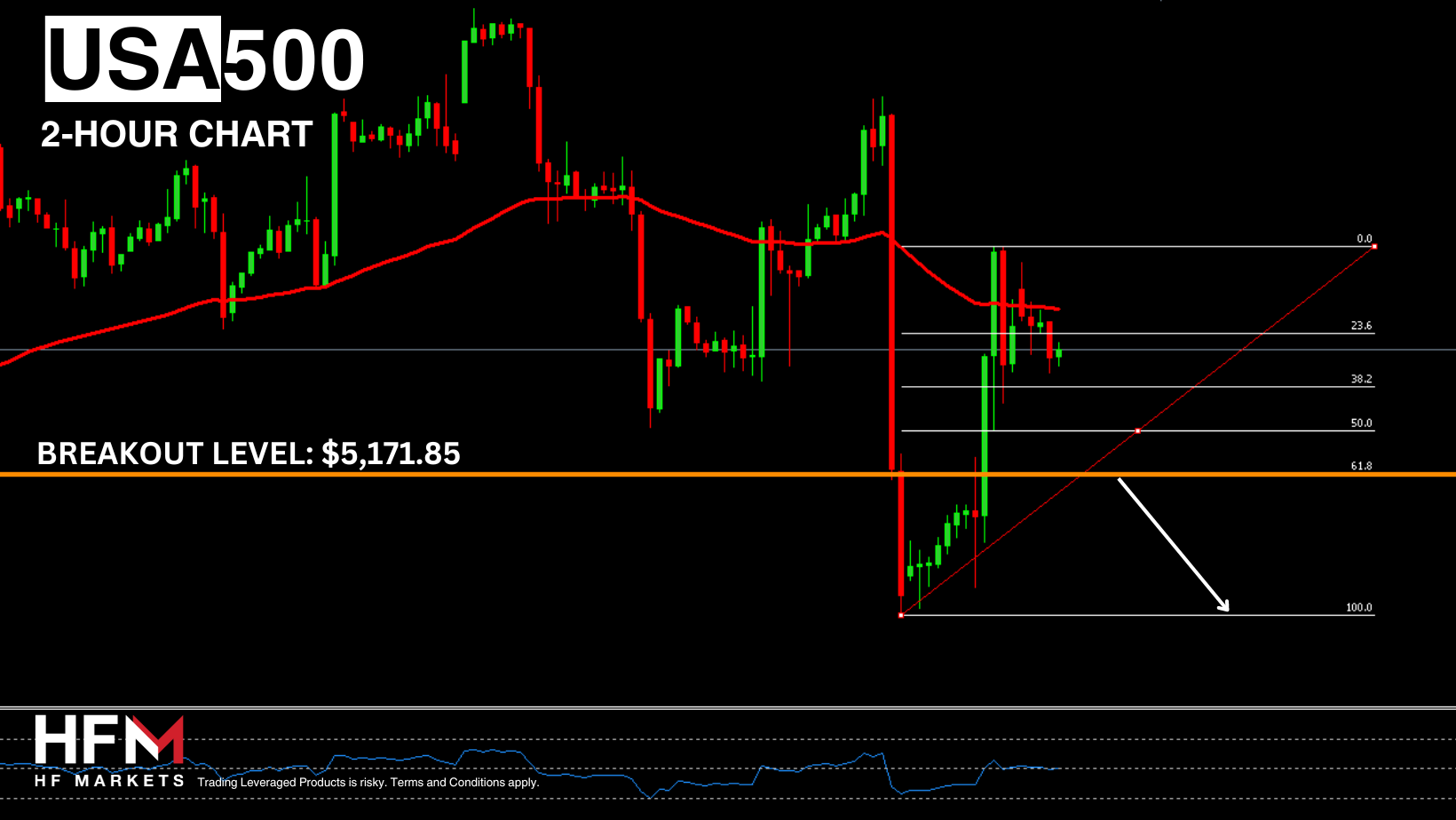

USA500 – Bond Yields Rise 50 Points Potentially Pressuring US Stocks!

The SNP500 is the index which is likely to be most influenced by this week’s earnings data. This is due to the index’s exposure to banking stocks. The price of the USA500 is technically still forming lower lows and lower highs which indicates a downward trend. However, corrective waves remain strong which indicate demand remains. Currently, the price is trading below momentum indications and below the “neutral” on oscillators. Therefore, the price is currently witnessing a weak “sell” signal. However, if the price drops below $5,197.16, indicators are likely to signal a stronger bearish signal.

To obtain further indication of the possible future price movement, investors will also be monitoring the global investor sentiment. Asian stocks are currently trading slightly lower, but the European Cash Open is yet to take place. If both Asian and European stocks decline, this could potentially back a low-risk appetite, which is negative for the USA500.

The employment data on Friday, reassured investors that the US economy remains strong and resilient to the current monetary policy. The NFP data read 43% higher than market expectations and average salaries rose more than the previous month. On the one hand, the data is positive as it indicates demand will remain high as will company earnings. However, on the other hand, if inflation also rises, the Fed will be unlikely to adjust interest rates.

Therefore, Wednesday’s Consumer Price Index will be key. If inflation reads higher than 3.4%, the stock market can come under immense pressure as the Fed are likely to become more hawkish. This is something which can already be seen from today’s rise in bond yields. The US 10-Year Treasury yields added 0.050% which is known to apply pressure to the stock market. If inflation reads in line with expectations, the release will be neutral. Furthermore, analysts expect the Core Inflation rate to fall from 3.8% to 3.7%.

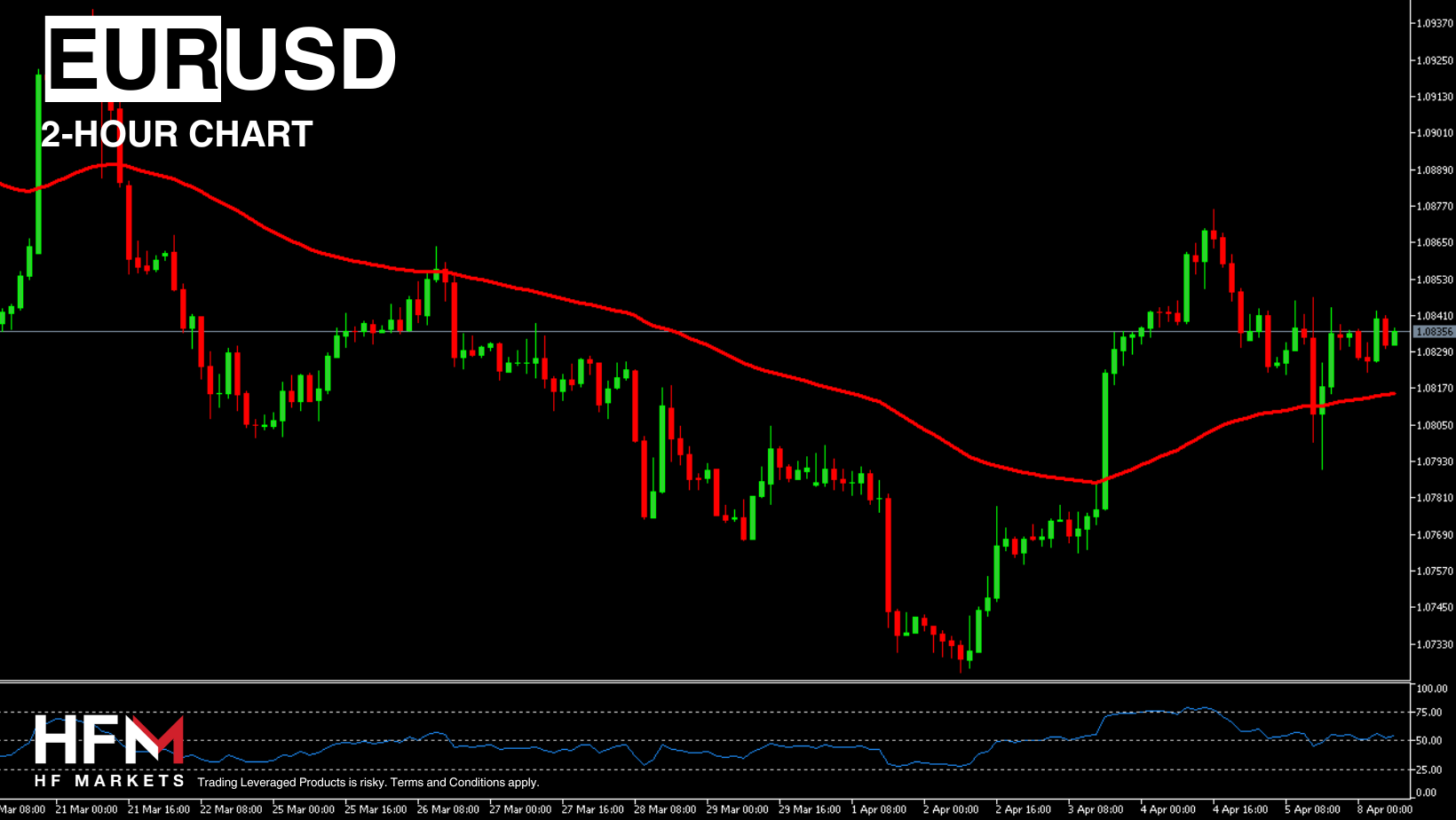

EURUSD – ECB To Indicate Next Cut!

The Euro is witnessing “mixed” price movement depending on the currency pair. Against the US Dollar the exchange rate is moving sideways, and the key price can be seen at 1.08426. Both the Euro and the US Dollar are likely to witness volatility throughout the week. The Euro due to the European Central Bank’s rate decision and press conference. The US Dollar due to Consumer and Producer Inflation.

Some economists believe the ECB may deem it too early to cut interest rates, but the general opinion is that the time to cut is very near for the ECB. Therefore, investors will closely be monitoring the President’s comments in the press conference on Thursday. The EU’s inflation rate has fallen to 2.4% and is the lowest amongst the G7. In addition to this, many EU economies have been witnessing prolonged stagnation and therefore will be keen to stimulate economic growth. The US Dollar on the other hand will primarily be determined by the CPI and PPI (producer inflation).

Michalis Efthymiou

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.