Economic Indicators & Central Banks:

- Treasuries were hit by stronger than expected ISM data and yields climbed sharply in a bear steepener. – US manufacturing unexpectedly expanded for the first time since September 2022 & input costs climbed.

- The latest ISM data indicates that the US economy continues to display strength despite elevated interest rates. This bodes well for the stock market, as it has the potential to fuel profit growth for businesses. However, it also raises concerns about inflationary pressures.

- Wall Street took its lumps to start Q2 amid the eroding Fed view and the pop in interest rates. The broader indexes closed with losses, though from fresh record highs last Thursday.

- FED: Expectations are moving toward fewer cuts this year as well, from the 3 that have been in for priced in much of 2024 to date, consistent with the FOMC’s dots, to 2, 1, or even none. A couple of key Fed officials, Waller and Bostic, have indicated their preferences for fewer than 3 cuts this year. Now there is a 61% chance of the Fed cutting rates in June.

- UK Nationwide house prices unexpectedly dropped -0.2% m/m in March, after rising 0.7% m/m in the previous month.

Market Trends:

- The Dow dropped -0.6% and the S&P 500 slid -0.2%. The NASDAQ managed a 0.11% rally.

- European stock futures are slightly higher in early trade, with the FTSE 100 outperforming. The Hang Seng rallied overnight, as Hong Kong’s markets re-opened after the extended holiday weekend and investors reacted to the better than expected Chinese PMI reports.

Financial Markets Performance:

- The USDIndex climbed back over the 105 level thanks to the strength in the data, closing at 105.019 and hitting the highest closing level since mid-November. Underpinning the move has been the hotter inflation data and resilient growth that have been shifting outlooks on the FOMC’s rate cutting trajectory, pushing back the timing of the first move toward July rather than June.

- The Yen was steady higher at 151.70. Focus is now fixed squarely on the BOJ’s bond-buying operation scheduled for Wednesday.

- Gold managed to hit a fresh peak at $2251.44 per ounce and a second close over $2200.

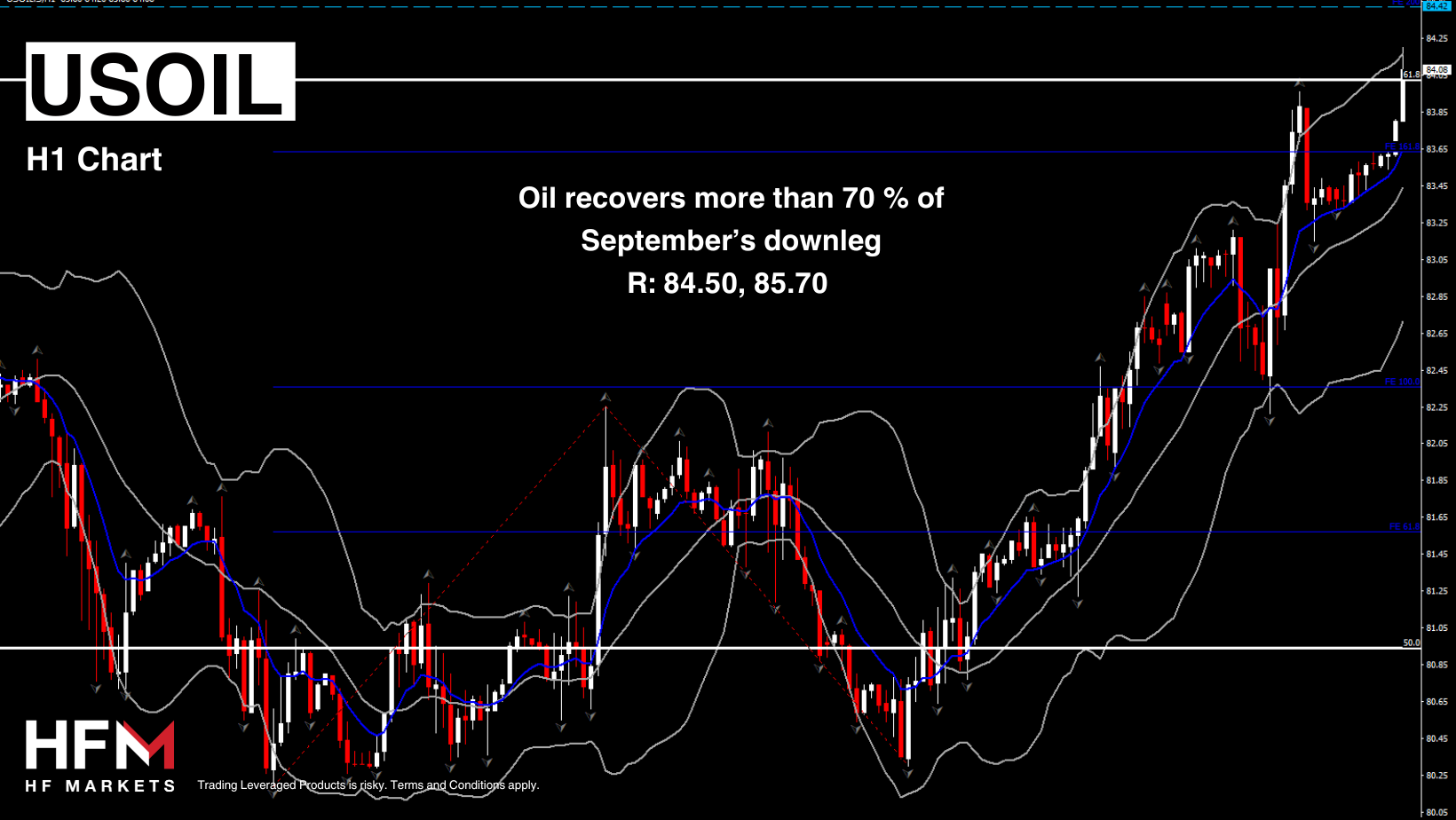

- USOIL breached 61.8% Fib. level since the September downleg, at $84.14. (Rising geopolitical risks in the ME & tighter supply from Mexico helping to buoy prices.)

- Bitcoin drifted back to $67k amid cooling demand for dedicated US ETFs and ebbing bets on looser Fed policy. – 10% down since $73,798 highs in mid-March.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.