FX News Today

- 10-year Treasury yields corrected -2.7 bp to 2.567% and JGB yields are down -1.4 bp at -0.0033%.

- Asian bonds were generally supported, as stock markets sentiment turned sour again, with South Korean paper underperforming after the BoK left interest rates unchanged, but cut its growth and inflation forecast to 2.5% and 1.1% respectively.

- Record household debt was one of the factors holding the BoK back from cutting rates for now, and South Korea’s 10-year yield jumped 5.9 bp as the bank tried to calm recession fears.

- Stock markets generally corrected from the six months high seen yesterday with uninspiring corporate earnings and problems with a new Samsung phone preventing further gains for now.

- Topix and Nikkei lost -0.96% and -0.80% respectively, after Wall Street closed with slight losses.

- The Hang Seng is down -0.58%, CSI 300 and Shanghai Comp down -0.44% and -0.39% respectively. The ASX dropped -0.10% and US stock futures are also broadly lower, suggesting ongoing pressure on markets.

- The front end WTI future meanwhile is trading at USD 63.77 per barrel.

Charts of the Day

Technician’s Corner

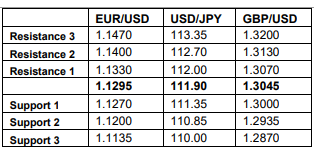

- EURUSD is still trading around the 1.13 level, and in a channel with key Resistance at 1.1320 and Support at 1.1279. Both are still strong after having bounced yesterday. Indicators are issuing mixed signals.

- GBPUSD has been stable around the 1.30 level, still unable to break through, fluctuating between the 1.3067-1.3026 Resistance and Support levels. Indicators are giving positive signals.

- USDJPY started the day below 112.00 mark, as indicators are suggesting a downwards movement. Support remains at 111.80.

- XAUUSD is trading at year-to-date lows, after breaking through the 1275 Support level. 1270 is the next Support level, with indicators are showing signs of stabilization.

Main Macro Events Today

- EU PMIs (EUR, GMT 08:00) – Manufacturing and Composite PMIs are expected to increase in April, to 47.9 and 51.8 respectively while the Services PMI is forecasted to have remained at 53.3.

- Retail Sales ex Fuel (GBP, GMT 08:30) – UK Retail Sales ex Fuel are expected to have increased to 4% y/y, compared to 3.8% y/y in March.

- Retail Sales ex Autos (USD, GMT 12:30) – Retail Sales are expected to have increased to 0.4% in March, up from the negative 0.2% surprise in February.

- Retail Sales (CAD, GMT 12:30) – Retail Sales are forecasted to have registered an increase in Canada as well, to 0.2% compared to 0.1% in January.

- Philly Fed Index (USD, GMT 12:30) – Philly Fed index is expected to have eased to 10.3 compared to 13.7 in March.

- Markit PMIs (USD, GMT 13:45) – Mixed signals are expected from the PMI release, as Manufacturing is expected to have increased to 52.8 from 52.4, while the Services PMI is expected to have declined to 55 from 55.3.

Support and Resistance

Click here to access the Economic Calendar

Dr Nektarios Michail

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.