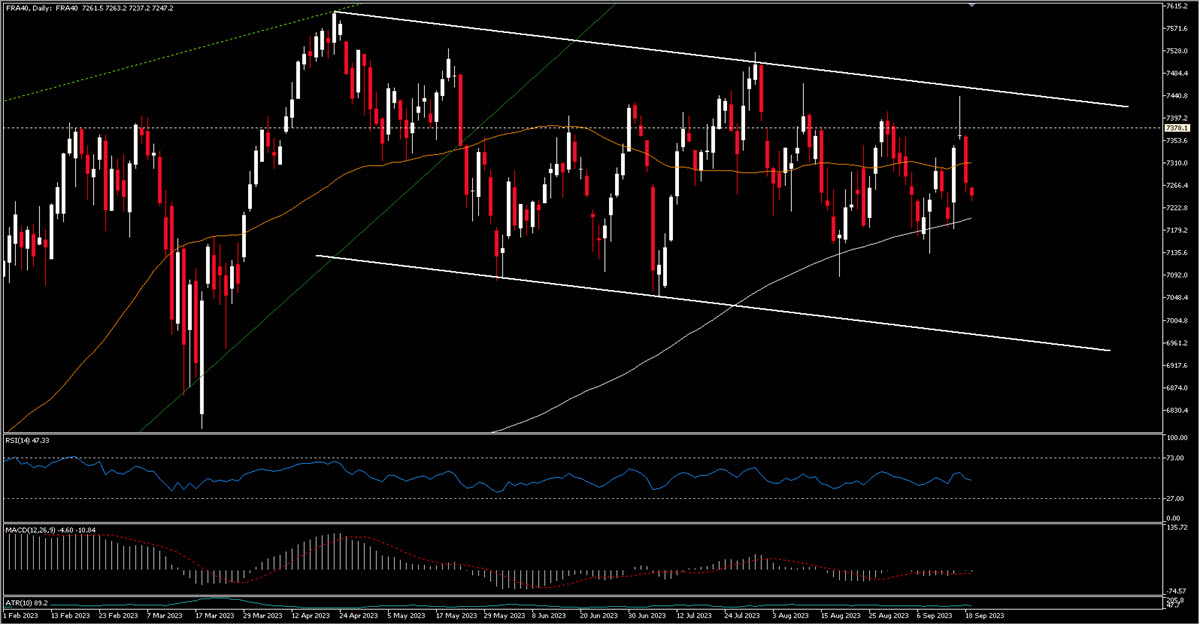

US Stocks barely budged yesterday, with all indices ending the session with tiny gains; volumes were muted too. On the other side of the ocean, we witnessed substantial losses among European indices, probably also weighed down by the ECB’s decision last week. The worst of all was the FRA40 after one of the largest domestic investment banks, Societe Generale, pledged to cut costs and tumbled 12.05%. It is not the first major investment bank to make similar pronouncements lately, with Goldman and Morgan Stanley planning to adjust their workforce next.

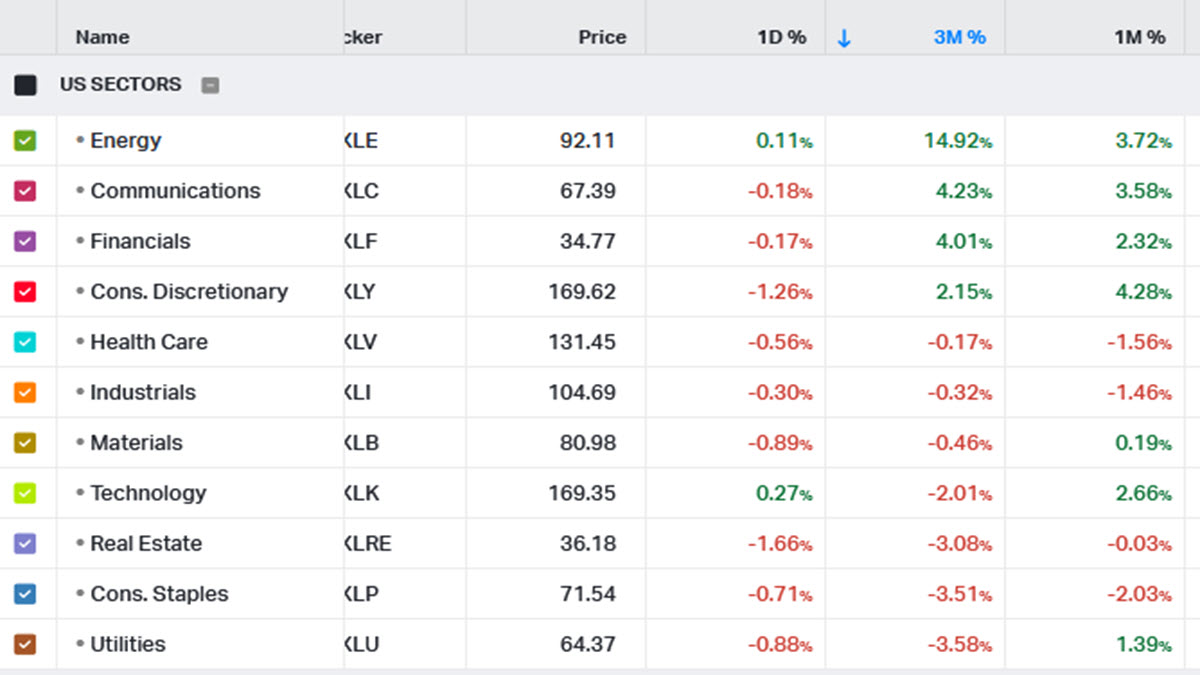

Back to America, strikes are hitting the economy with 4.1 million labor hours lost in August, the most in 23 years: perhaps another reason why the indices’ rally has come to a standstill with the Nasdaq – for instance – remaining at the level of three months ago. To be fair, yesterday the good performance of Apple and Meta helped it to gain +0.15%. Technology was the best sector for the day, along with Energy: however, it is striking to see how the latter has been the star performer in recent months – led by the oil rally – with the ETF tracking the sector (XLE) up 14.92% in three months versus a paltry +1% for the US500.

The RBA minutes this morning held few surprises and the AUD, like the USD, is little moved. Rates continue to push slowly upwards and the 2-year is close to its March high of 5.066%. The market believes that the Fed will not move tomorrow – 99% odds – but the Dot Plot predicts another hike this year: GS is convinced that this is just a ”bluff”. We shall see.

- FX – USDIndex flat at 104.86; AUDUSD -0.04% @ 0.6433, GBPUSD < 1.24 (1.2377, EURUSD -0.12% @ 1.0679. USDJPY just shy of 148 and USDCNH back at 7.30.

- Stocks – US Futures are inching lower (US500 -0.12%, US100 -0.25%, US30 -0.09%); EU futures are adding to yesterday’s losses. AAPL +1.69%, Square’s and Lonza’s CEOs to depart the companies (latter one -14%), second interesting IPO in a couple of days with Instacart valued $10B, 75% less than the previous Private VC valuation.

- Commodities – USOil +0.08% at $92.27, UKOil hit $95, now trading at $94.69, Wheat, Corn close to 2023 lows.

- GOLD – -0.13% @ $1931.

Today: Highlights include European HICP, Core HICP, US Housing Starts, Canadian CPI.

Interesting Mover: FRA40 -1.39% @7276 after testing the top of the channel with a perfect spinning top on high volumes, fell hard yesterday led by the slump of one of the largest French banks (SocGen -12%).

Click here to access our Economic Calendar

Marco Turatti

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.