Bank jitters continue to ease lifting sentiment & Asian markets despite US stocks closing in the red. The USD eased another 0.3% and Yields gained with the 2-yr regaining 4%. Alibaba surged 14.3% in US trading and was up 16.3% at one point in Hong Kong after it announced it will split into 6 separate entities. Other Chinese tech companies (Tencent & JD.com)) are stronger. The YEN continues it’s volatile week as year end looms, AUD is lower on weaker Inflation, European & US Futures are higher. US Consumer Confidence was better than expected, the Fed’s Barr called SVB “not well managed” and that the $142 billion of withdrawals in first week of March represented 81% of 2022 deposits.

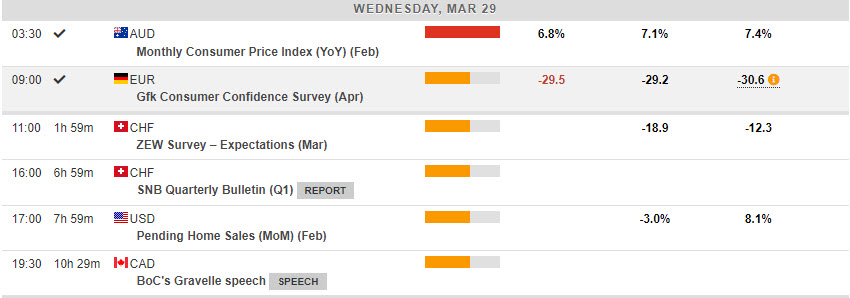

Overnight: AUD CPI missed (6.8% vs. 7.2% & 7.4%) and adds to prospects of RBA pausing rate hikes at next week’s meeting. German GfK Consumer Climate in-line (-29.5% vs -29.5% & -30.6%).

- FX – USDIndex drifted 0.3% lower yesterday to test 102.00 before a bounce to 102.25. EUR rallied from 1.0800 to 1.0850 now. JPY continued its volatile week back to 132.00 now after lows of 130.40 yesterday, Sterling rallied over 1.2300 to 1.2340 and holds at 1.2325 now.

- Stocks – US markets lower (-0.12% to -0.45%) Major movers outside the Chinese tech stocks were OXY +4.29% & LYFT -7.6%. US500 –0.16% (-6.26) to 3971, US500 FUTS +0.37% higher at 4026 now.

- Commodities – USOil – Futures recovery continued again yesterday from $70.00 to hold over $73.00 and test $74.00. EIA Inventories today. Gold – dipped to $1950 once again, rallied to $1975 and trades at $1960 now.

- Cryptocurrencies – BTC has recovered to $28k today after testing $26.5k again. SBF faces new SEC charges that he tried to bribe Chinese officials with a $40 million payment.

Today – US House Financial Services Committee re. SIVB, Speeches from Fed’s Barr, BoE’s Mann, ECB’s Schnabel.

Biggest FX Mover @ (07:30 GMT) USDJPY (+0.79%). Volatility continues. Tested down to 130.40 after weak inflation yesterday, testing 132.00 today. MAs aligned higher, MACD histogram & signal line positive & rising, RSI 71, OB & rising, H1 ATR 0.216, Daily ATR 1.910.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.