Chinese New Year celebrations – many centres are closed in Asia. Treasuries sagged to end on a bearish week. USDIndex at 101.30 low as the market continued to price out a 25 bp rate hike on February 1 & BoJ’s latest attempt to keep a lid on yields, along with some profit taking. Wall Street (US100 +2.66%), 10-year Treasury yield is at 3.48%. Options expirations likely helped support the advance. A report of big layoffs at Alphabet added to recession fears and weighed initially, but signs of cost cutting enticed dip buying. Goldman Sachs slipped on reports of a DoJ probe into its consumer unit.

- The USD Index sagged at 101.32.

- EUR – is flirting with the 1.09 mark.

- JPY – sold off and USDJPY lifted to 130.21, although the USD corrected against most other currencies.

- GBP – slipped to 1.2400 again after the data this morning. The UK consumer confidence is finally improving. The FT reported that the Deloitte Consumer Tracker rose 0.6 points – the first improvement in five consecutive quarters.

- Stocks – The US100 surged a heady 2.66%, with the US500 up 1.89% and the US30 1.0% higher. The Nikkei rallied 1.3%, the Topix added around 1%. The ASX managed a 0.1% gain and European stock futures are higher. GER40 +0.5%, UK100 +0.2%.

- Citadel breaks records with $16bn profit. Ken Griffin’s hedge fund charged its investors $12bn in fees and expenses in 2022.

- USOil – tops at $81.40, as USD supports crude prices.

- Gold – retested $1,937 highs but turned to $1,920 lows since then.

- BTC – spikes to 22,800 area (September’s peak) – Risky trades?

Today – ECB’s Lagarde and Panetta speech. A quarter of the S&P 500 report this week starting with Microsoft on Tuesday.

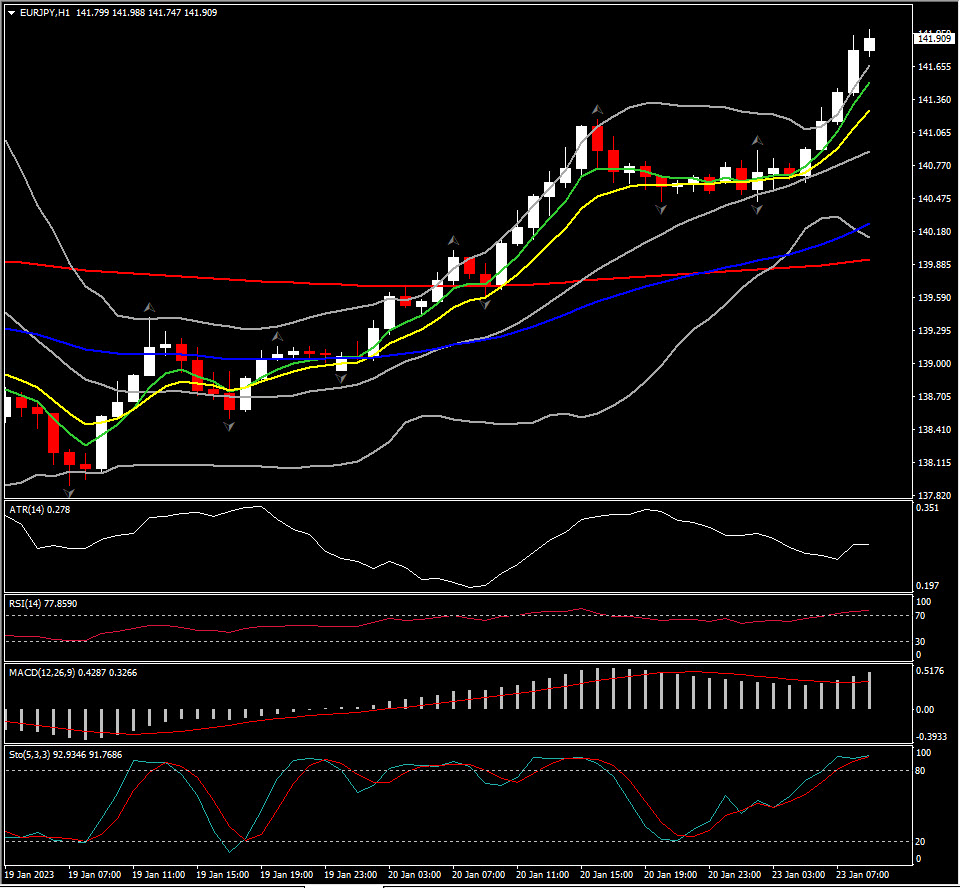

Biggest FX Mover @ (07:30 GMT) EURJPY (+0.87%). Rallied to 141.90. MAs aligned higher, MACD histogram & signal line positive & rising. RSI 77.85, OB & rising, H1 ATR 0.278, Daily ATR 1.834.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.