")

- The USD Index slipped further to test 110.00 yesterday, a -2.65% decline from Thursday’s high at 113.00, trades at 110.25 today. Stocks rallied another +1.00%, Yields moved higher again (10-yr 4.163%) and the Commodity Complex cooled from Fridays rally as Beijing reaffirmed its strict pandemic rules. Overnight the Crypto Complex has tanked with BTCUSD down from $21k to under $19.5k.

Markets are pricing in a “lame-duck” President Biden for the final 2-yrs of his administration as Republicans are likely to take control of the House of Representatives, with likely curbs on the debt ceiling, spending cuts and action to support energy companies, as inflation bites into businesses and households. A loss of the Senate too for President Biden would completely restrict any political actions regarding immigration, additional support for Ukraine and environmental policies. TRUMP “Big announcement” November 15.

- EUR – continued to rally yesterday and breached the hugely psychological parity 1.0000 level.

- JPY – dipped to 146.10 lows from 147.50 and remains capped by 147.00 today.

- GBP – Sterling rallied over 200 pips again yesterday from 1.1300 to over 1.1540, but has since sunk below 1.1500.

- Stocks – Wall Street closed higher, tech led again META +6.53%, (job cuts) GOOG & MFST over +2.2% and TSLA –5.01%. US500 closed +36.25 (+0.96%) at 3806, FUTS trades at 3808 now.

- USOil – spiked over $93.00, yesterday before slipping to close at $92.00 and lower again now at $91.40.

- Gold – once again tested Friday’s close at $1680 before drifting to $1675 into close and $1670 now.

- BTC – drifted from $21.2k, top Monday to $20.5k at close, before tanking to $19.3k lows today as FTX CEO Sam Bankman-Fried and Binance CEO Changpeng Zhao trade allegations. It traces back to FTT coin, which is FTX’s token and a report from CoinDesk that says Bankman-Fried’s trading company Alameda Research has about $6 billion of its $14.6 billion assets in the coin, which his other company created.¹

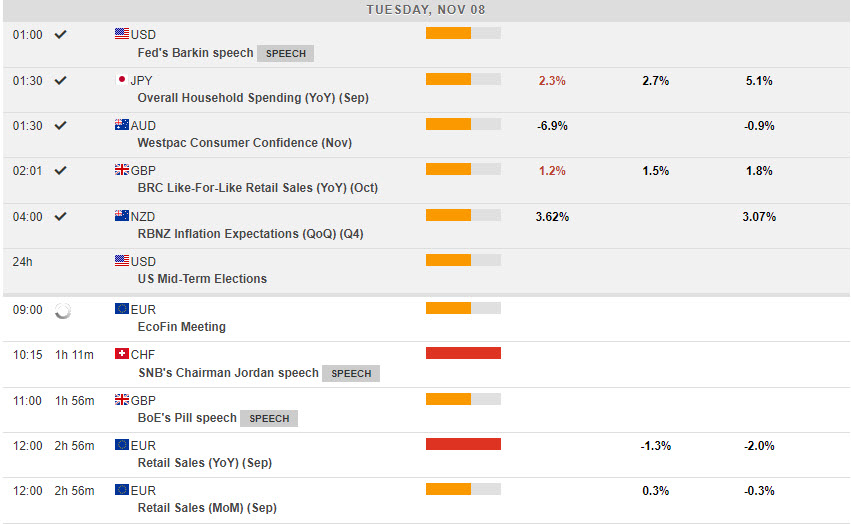

Today – EZ Retail Sales, US Midterms, Speeches from BoE’s Pill (x2), Fed’s Williams, ECB’s Nagel & SNB’s Jordan.

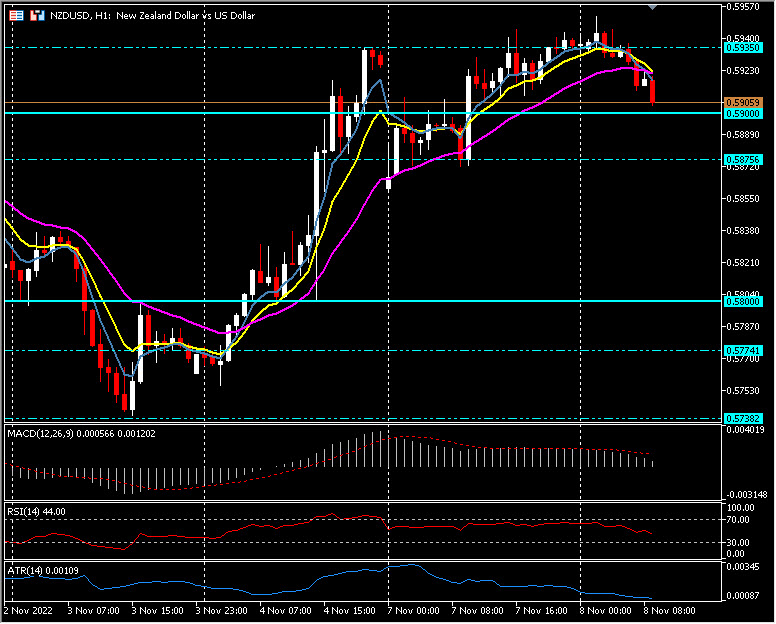

Biggest FX Mover @ (06:30 GMT) NZDUSD (-0.47%) rallied yesterday from an initial dip, beyond Friday’s high to 0.5952, to 0.5900 now. MAs aligned lower, MACD histogram & signal line positive but falling, RSI 41.42 & falling, H1 ATR 0.00114, Daily ATR 0.01091.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.