- USDIndex – volatile day – new 20-yr highs at 109.20 declined to 108.00 after weak PMI & Housing Data before Kashkari “biggest fear is inflation will be more persistent”.

- EUR – Weighed by weak PMI & energy crisis and 3 day shutdown of Nord Stream 1, 3rd day under Parity (1.000) at 0.9940.

- JPY holds between 137.00 & 136.00

- GBP also weighed by weak PMI data, energy crisis, weak government & widening strike action.Trades at 1.1800

- Stocks US stocks flat into close. (S&P500 -9.26pts (-0.22%) 4128) – Biggest movers – Oil stocks +4-6%, TWTR -7.32% & ZM -16.45%.

- Oil continued to rally, moved +4% Tuesday to $94.00 following Saudi “CUTTING production” comments.

- Gold – support at $1736 trades at $1745

- BTC – ranging between 21k & 21.5K.

Overnight – Asian equity markets fell for an eighth straight day. European FUTS also lower.

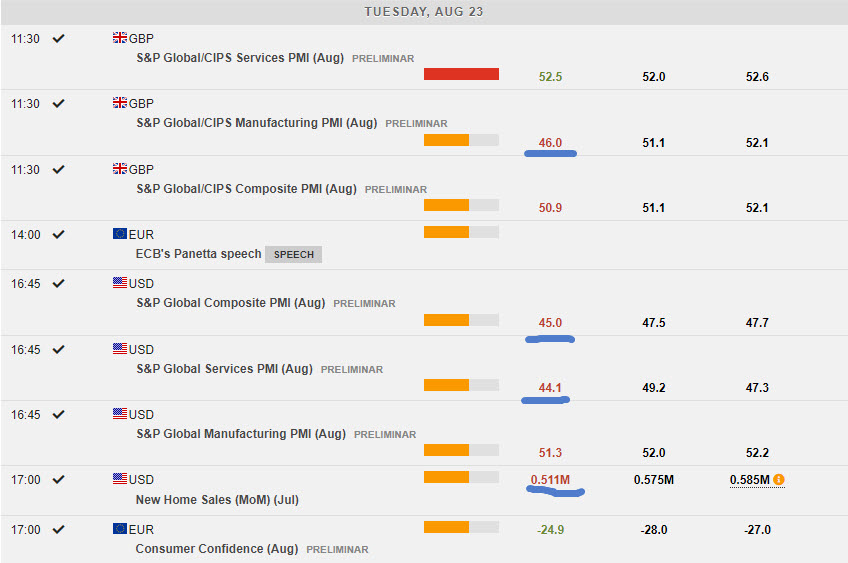

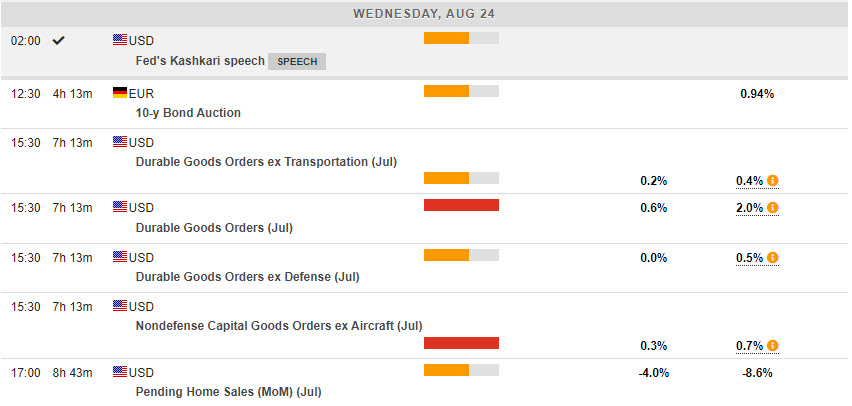

Today – US Durable Goods.

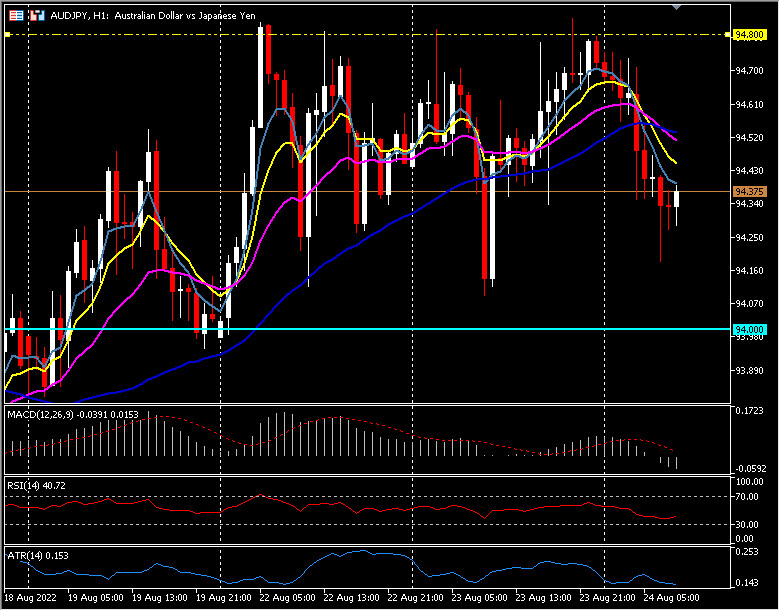

Biggest FX Mover @ (06:30 GMT) AUDJPY (-0.45%). Rejected 94.80 again yesterday and trades under 94.40 now. MAs aligning lower, MACD histogram negative & signal line falling, RSI 40.36 & falling, H1 ATR 0.153, Daily ATR 0.96.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.