USDJPY rebounded sharply last week, garnering a +1.29% lead that was largely won on Friday. The Yen weakened further on Friday, after stronger-than-expected July US payrolls data triggered a spike in T-note yields. The divergence in the US-JPN bond yields weighed on the Yen further, after the 10-year JGB bond yield fell to a 4-month low on Friday of 0.166% and the 10-year T-note yield rose to a 2-week high of 2.867%.

Japan’s leading index of economic data for June fell -0.6 to a 4-month low of 100.6. Meanwhile, Japan’s June household spending rose strongly for the 5th month by +3.5% y/y, above expectations of +1.5% y/y. However, these two data have not had an effect on currency movements, because attention immediately turned to next week’s data.

Hawkish comments from FOMC members over the past week have lifted the pair and the jobs report gave it another push higher. The pair’s direction is still heavily influenced by the difference in US and Japanese interest rates.

No major events regarding the Japanese economy are expected this week. There is a public holiday (Mountain Day) on Thursday 11 August.

Technical Overview

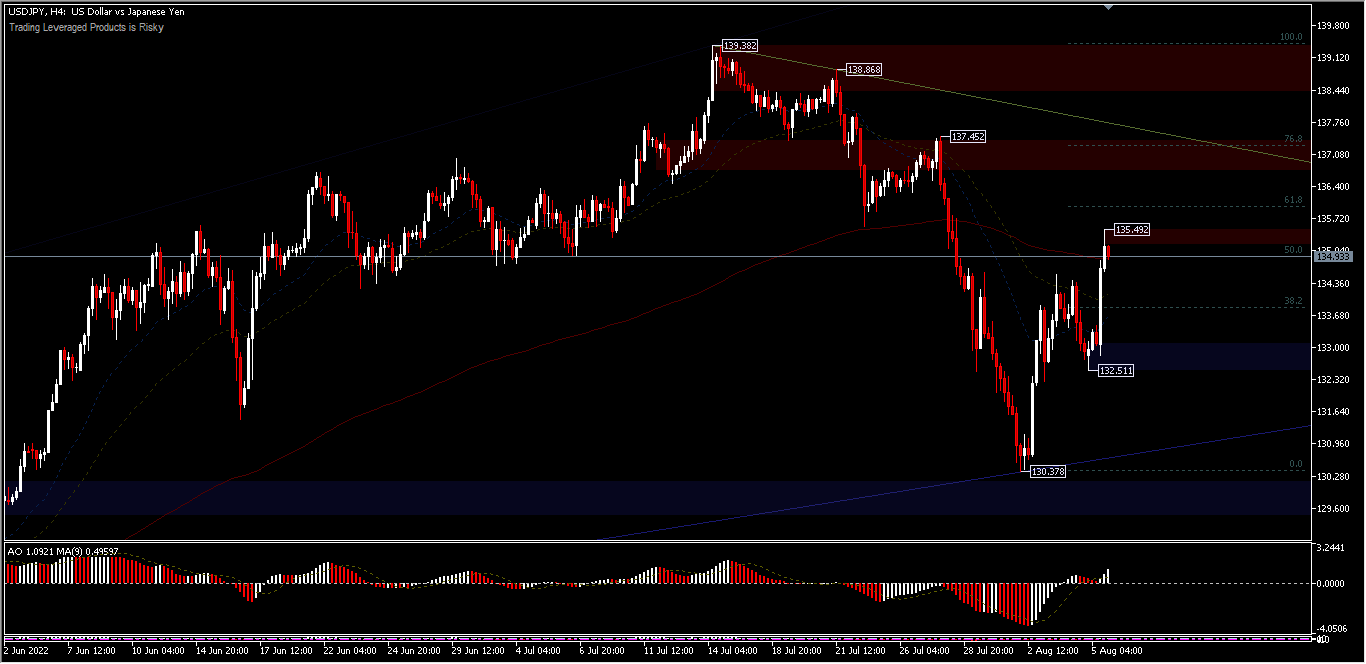

USDJPY has continued to strengthen to near the 61.8% FR level, after recording a correction to 130.37 last week due to political tensions in the Taiwan Strait. Now the pair is trading near the area of the July opening. The intraday bias slightly increased earlier in the week, with chances to test the 61.8%FR (136.00) and 76.8%FR (137.45) levels. The gains should be capped at a peak of 139.38 to bring the downside.

On the downside, a price move below the 132.51 minor support will continue the 139.38 decline towards 130.37 and the 126.35 structural support. The current price position is at the 200-period EMA and AO which validates the rebound is still in the buy zone.

Click here to access our Economic Calendar

Ady Phangestu

Market Analyst – HF Educational Office – Indonesia

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.