FOMC hiked rates 75 bps, 10-1 vote; further increases likely appropriate. USD supported (USDIndex 104.80), Stocks higher despite Fed (NASDAQ +2.5%, Dow 1.4% & S&P +2%). Despite the Fed effecting the biggest increase in interest rates in 28 years, bonds and stocks rallied hard, underpinned by the fact Chair Powell said the 75 bps was an unusual move and would not be a common action, noting further hikes would be 50 bps or 75 bps. After hitting multi-month lows earlier this week, most regional currencies firmed on Thursday after US Bond Yields and the USD retreated from multi-year highs a day earlier as investors welcomed the Fed’s decision. It is clear that the Fed’s move will keep stagflation concerns alive. Asian markets traded mixed and US futures have pared earlier gains.

- USDIndex held above 104.40.

- Υields 10-year Treasury yield climbed 1.5 bp to 3.3% while Australia’s bonds also moved up.

- Equities – GER40 and UK100 futures are mixed with the UK100 down -0.2% ahead of the BoE decision, the GER40 up 0.3%.

- Oil settled to 115.76 after a steep drop, supported by tight oil supply (100k b/d highest since April 2020) and peak summer consumption, after the Fed sparked fears of slower economic growth and less fuel demand.

- Golds at $1830 – safe-haven demand & inflationary hedge buying VS a higher interest rate.

- Bitcoin down to $20,157.

- FX markets – EURUSD at 1.0409, USDJPY back above 134, Cable down at 1.2100 ahead of BoE.

BoE Preview: The BoE is still set to deliver another 25 bps rate hike this week, but stagflation risks are looking nowhere as serious as in the UK That should prevent the central bank from joining the “50 bp club” of central banks, but for now is unlikely to stop the BoE from sticking to the tightening path. The statement may sound somewhat more cautious now. Even the BoE’s own scenario suggests a technical recession next year and the latest batch of forecasts from the OECD and others highlight that the economy is under-performing, with the fallout from Brexit, the sanctions against Russia, and political turmoil all weighing on the growth outlook. PM Johnson managed to survive a confidence vote last week, but many feel that his days are numbered. Even within his own party the threat to unilaterally step back from the Northern Ireland protocol is not very popular and rather than uniting the nation behind Brexit, the government is facing an increasingly fragmented union. Nevertheless, with inflation running far above target, the BoE has little choice but to lift rates further for now, especially as house price inflation is also still running at double digits, and wage growth is picking up in tight markets.

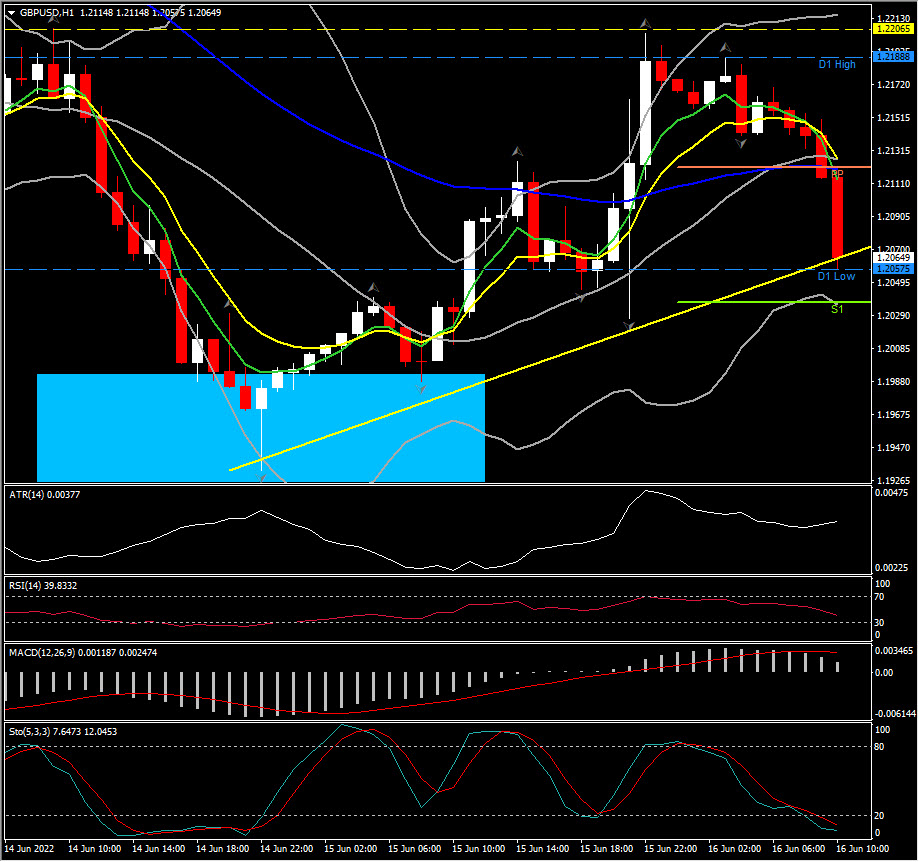

Biggest FX Mover @ (06:30 GMT) GBPUSD (-0.84%) down to 1.20 area again. Intraday, MAs bearishly crossed, MACD histogram declines but holds above 0, RSI 40 & sloping. H1 ATR at 0.00377 & Daily ATR at 0.01434.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.