It could perhaps be suggested that our analysis is developing a fixation with Australia. However, data releases are supportive of thesis our previous articles are presenting.

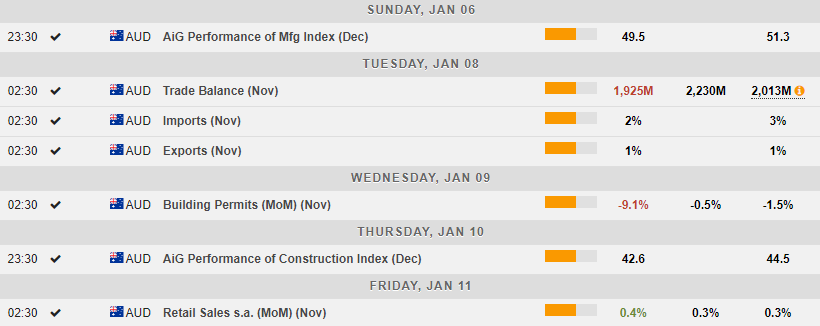

Take the last couple of days for example: the AiG Manufacturing Index crossed 50, suggesting a contraction in the sector, the trade surplus declined on account of China’s worse than expected economic performance, building permits declined by 9.1%, and the construction sector continues to be in the red for the fourth consecutive month. Retail sales are growing a bit but then PCE was also positive for the US until mid-2008, almost halfway through the recession.

Despite its large size, it is usually the case that Australia and its currency do not receive much attention from the markets or the media. However, this argument does not appear valid once we take the Aussie’s behaviour through the past year into consideration.

Despite its large size, it is usually the case that Australia and its currency do not receive much attention from the markets or the media. However, this argument does not appear valid once we take the Aussie’s behaviour through the past year into consideration.

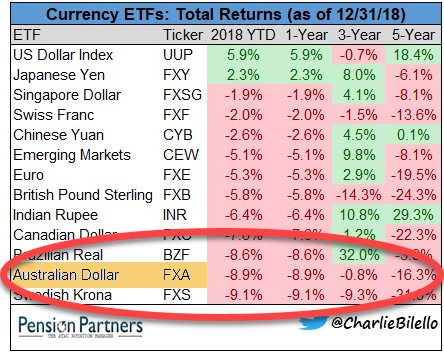

The currency has significantly weakened over the year, as markets have been heavily discounting it: from the market close value in the last week of 2017 to the market close value in the last week of 2018, the Aussie lost 10.1% of its value against the Dollar, 4.7% against the Euro, 14.7% against the Yen and 3.6% against the Brexit-ridden Sterling. The AUS200, while not completely reliable as it followed the overall stock market trends in the world, also lost 7.4% of its value through the year. The Aussie was the worst overall performer throughout the year, second only to the Swedish Krona, accumulating an 8.9% loss.

It’s true that we’ve published articles on the above before, more than once actually, but let’s reiterate it once more: Australia’s housing sector is in trouble, and this will likely affect its banks. There is still time until the ultimate bust, but 2019 will definitely be a very interesting year for the country.

Once the economy goes into recession, things will get tough. Ironically, the RBA interest rate is already too low for any meaningful action (plus the recession will be supply- and not demand-driven), so it will have to resort to QE, which will not really help the economy given that banks will be unwilling to lend. Thus, the only other option would be a bail-out (or a bail-in, but that’s more extreme). More on this in the future.

Click here to access the HotForex Economic Calendar

Dr Nektarios Michail

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.