The stock market drop since late September appears to have ended in the start of the year. After the USA500 reached its peak at 2934, it has subsequently reached a low of 2315, after which it bounced due to positive news on the US-China trade talks.

Overall, the markets are beginning to realize that the rate hikes are not the real reason behind the drop in production and that the US economy is, at the moment, more likely to experience a slowdown than a recession. Justification for such a prediction can be found by simply looking at the banking sector’s behaviour over the past few quarters.

As I’ve mentioned in the past, the US should aim to fix the trade war issue and adjust its fiscal spending in order to ensure continuous expansion. However, a slowdown may actually be useful for the US, especially as more people realize that their debt burden may still be somewhat excessive.

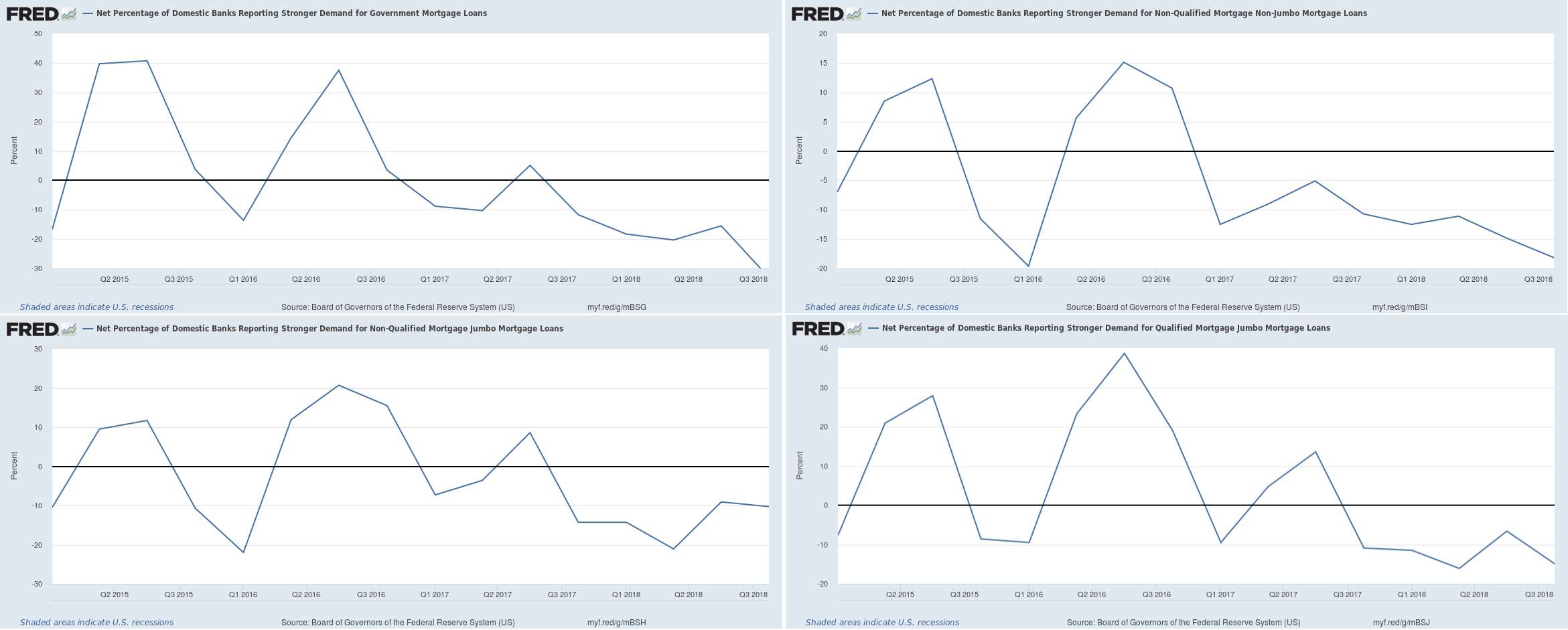

Data support this conclusion: demand for the majority of loan categories (auto, real estate, industrial and commercial, credit card) has been declining as the top figure shows. In addition, demand for mortgage loans has also been declining since 2017. Even though a decline in demand does not necessarily suggest negative demand, it is interesting to observe that 2017 marked the first year since 2009 that loans-to-GDP declined.

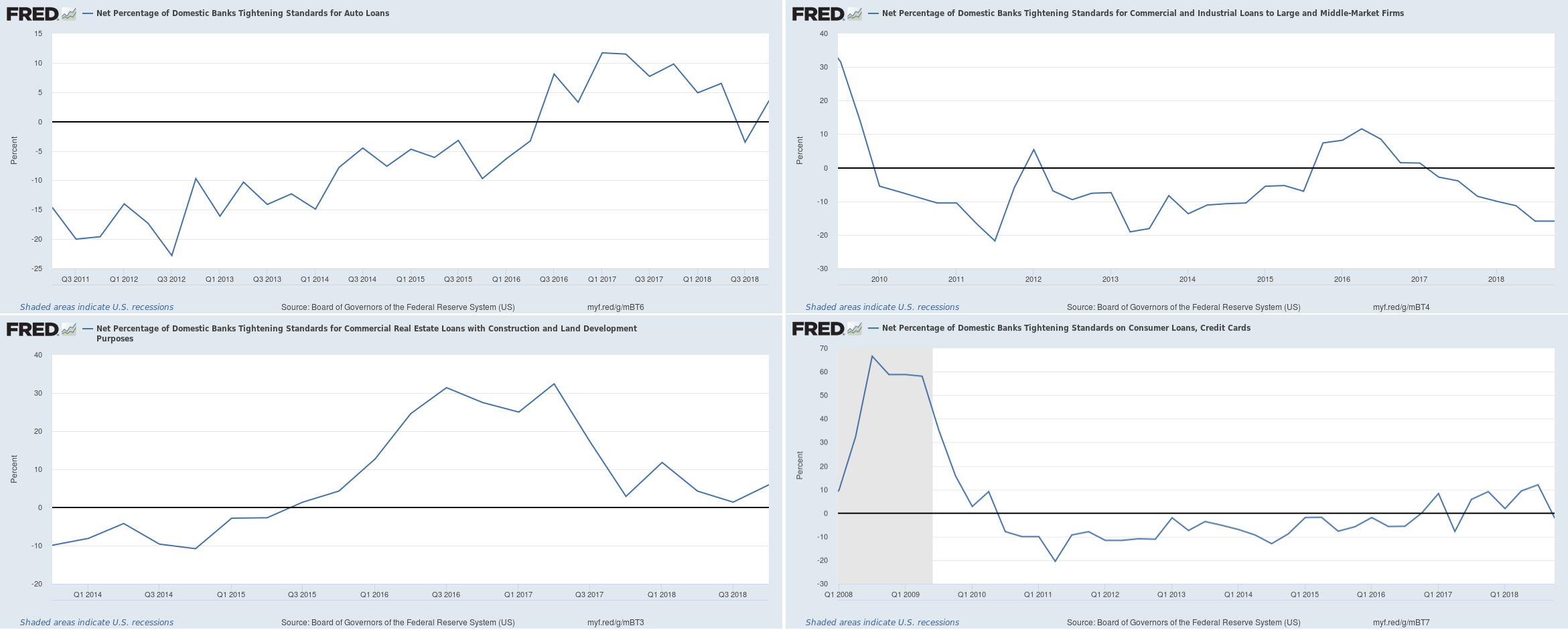

This deleveraging process appears to have happened with some assistance from lending standards, i.e. the banks’ appetite to lend (figure below). These appear to have registered a mixed response, as they have tightened for real estate and auto loans (first column), while they are flat for credit cards and looser for commercial and industrial loans. While a tightening of lending standards could be expected given the interest rate hikes since 2017, banks appear to be much more reasonable than before as they prefer to fund loans for productive purposes (commercial and industrial) while consumption loans are becoming harder to obtain. These effects are the essence of monetary policy which aims to discourage lending in order to prevent the economy from overheating.

This deleveraging process appears to have happened with some assistance from lending standards, i.e. the banks’ appetite to lend (figure below). These appear to have registered a mixed response, as they have tightened for real estate and auto loans (first column), while they are flat for credit cards and looser for commercial and industrial loans. While a tightening of lending standards could be expected given the interest rate hikes since 2017, banks appear to be much more reasonable than before as they prefer to fund loans for productive purposes (commercial and industrial) while consumption loans are becoming harder to obtain. These effects are the essence of monetary policy which aims to discourage lending in order to prevent the economy from overheating.

The effects from this deleveraging process are also positive given that debt service payments, as a percentage of disposable income have been decreasing, despite the interest rate increases, largely due to this deleveraging phase of the economy. Note that the deleveraging is only relative: loans are increasing but at a rate slower than the increase in national income, allowing the debt burden to decrease.

The effects from this deleveraging process are also positive given that debt service payments, as a percentage of disposable income have been decreasing, despite the interest rate increases, largely due to this deleveraging phase of the economy. Note that the deleveraging is only relative: loans are increasing but at a rate slower than the increase in national income, allowing the debt burden to decrease.

This is precisely what the US economy needs at the moment, but this should be viewed in the prism of the national economy and not take international developments into consideration. The relative deleveraging phase started in 2017, long before the trade war and the fiscal shutdown. While it is convenient to view the economy as a machine, the fact is that like every machine, it does not operate in a vacuum and international pressures such as the trade war could potentially have a larger impact than expected.

Summing up, the relative debt reduction, i.e. a slower increase in loans than GDP growth, stemming from the realization that debt should be reduced in order for consumers to continue being able to repay their loans, could cause a slowdown in US economic activity. However, the end of this short-term debt cycle is not the real threat for the US economy as it merely acts as a growth drag.

On the other hand, the effects from the trade war, while not so severe if they just increase inflation and decrease corporate profits, despite the negative effect they would have on the stock market, could cause real economic damage if they hurt imports. This appears to have already begun though, and the overall developments could be catalytic for the US economy’s performance next year.

Click here to access the HotForex Economic Calendar

Dr Nektarios Michail

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

{kind=link}