FX News Today

- USDJPY and Yen crosses have remained heavy, although above recent lows, with the Japanese currency buoyed by safe haven demand as the global stock rout took another turn lower today in Asia.

- AUDJPY carved out a 16-day nadir at 81.27. EURJPY has already traded heavy, although like USDJPY has remained just above recent lows.

- 10-year Treasury yields declined -2.5 bp, back below 3%, and 10-year JGB yields dropped -0.5 bp to 0.051% as stock markets sold off.

- Topix and Nikkei are down -1.82% and -1.915 respectively. The Hang Seng lost -2.85% so far, the CSI 300 is down -2.15% and Shanghai and Shenzhen Comps are down -1.67% and -2.06% respectively. The ASX outperformed but is also down -0.19%.

- Most of the negative reactions were based on the news that Huawei’s CFO has been arrested in Canada, reportedly on suspicion of violating US sanctions.

- The concern is that the arrest will complicate the trade talks between the US and China. The US has been telling allies not to use Huawei products and developments have dampened hopes of a trade truce amid mounting concerns about the outlook for US, with investors still fretting about the potential recessionary signal of the recent inversion at the short end of the US yield curve, and world growth. Taiwan’s central bank governor also said that US-China war may last one to two years, which chimed with a theme in market narratives that both sides remain on a different page in their trade dispute, despite officials having sounded out positive mood music.

- Oil prices fell back below the USD 53 per barrel mark ahead of the OPEC meeting, with source stories suggesting that the monitoring committee of OPEC and its allies agreed to cut output next year, but there are concerns that this will turn into a general declaration of intent, rather than a firm commitment to actual cuts.

- BoJ’s Kuroda said median- and long-term inflation expectations are not rising, reaffirming the widespread view that ultra-accommodative monetary policy will remain for a considerable time yet.

Charts of the Day

Main Macro Events Today

- US Labour Market Data – US Initial Jobless Claims are expected to come out less than last week, while Continuing Jobless Claims are forecasted to be lower than last week. NonFarm Productivity is expected to have grown by 2.3% in Q3, while Unit Labour Costs are expected to have grown by 1.1% during the same period.

- BoC Governor Poloz Speech – The BoC Governor is set to speak about the economic outlook in Canada’s financial system and the December interest rate decision.

- US PMIs and Factory Orders – Markit Services PMI is expected to come out at the same level as October, while the ISM Non-Manufacturing PMI should have decreased to 59.2 in November. Factory Orders are expected to have declined by 0.2% in October, compared to 0.7% in November.

- Canada PMI – The Canadian PMI is expected to have decreased to 59.7 in November compared to 61.8 in October.

- Fed Powell Speech.

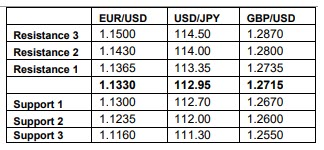

Support and Resistance

Click here to access the HotForex Economic Calendar

Dr Nektarios Michail

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.