FX News Today

Asian Market Wrap: 10-year Treasury yields pared some of their earlier gains and are down -0.2 bp on the day at 2.844%, 10-year JGB yields are still up 0.1 bp but at 0.088% also down from earlier highs as the buoyant mood on equities starts to fade and the Yen strengthened against the Dollar. Asian stock markets still benefited from hopes for a bilateral trade deal between the US and Mexico and mostly extended yesterday’s gains after a strong close on Wall Street. Questions over where the deal will leave Canada seem to limit the room for further gains however, as investors clamour for detail. Topix and Nikkei are still up 0.26% and 0.19% respectively, but off highs. The Hang Seng managed to hang on to a modest 0.17% gain, while mainland China underperformed with CSI 300 and Shanghai Comp down -0.19% and -0.12% respectively. US futures are slightly higher, Oil prices fell back from highs above USD 69 per barrel.

FX Update: USDJPY flipped back above 111.00, continuing an oscillation of this level for a third consecutive session, holding below the three-week high that was printed on Friday at 111.48. Yen crosses have been more buoyant, with EURJPY and AUDJPY, for instance, posting respective 4- and 3-week highs during the Tokyo AM session, although both crosses have since come off by between 20 and 30 pips. The Yen’s overall weakness has been concomitant with the USA500 closing at a record high yesterday and generally upbeat tone in global equity markets. Yield differentials remains a fundamental bullish driver for USDJPY, but the risks being posed by the US-China trade war, which doesn’t so far show any signs of cooling in the wake of the US-Mexican agreement in principle, has been capping upside potential in recent months, which is expected to remain the case. Regarding the US-China trade situation, Trump in the wake of his stage-managed Mexico announcement) that “it’s just not the right time to talk right now.” USDJPY has resistance at 111.48-50 and 112.15, and support at 110.93-95

Charts of the Day

Main Macro Events Today

- S&P/Case-Shiller Home Price Indices – Expectations – expected to remain unchanged at 6.5% y/y for June.

- US Consumer confidence – Expectations – Consumer confidence should rise to 127.0 in August, from 127.4 in July. Confidence readings remain at elevated levels, close to the 17-year high of 130.0 registered in February and we expect this trend to continue over the coming months, despite the noise from trade and politics.

- US Goods Trade Balance – Expectations – The advance indicators for July should show a deterioration in the Trade Balance for Goods to -$70.5 bln (-$68.5 bln) after widening for the first time in four months to -$67.9 bln in June.

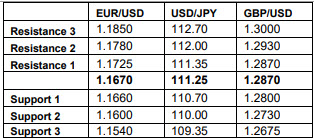

Support and Resistance levels

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/08/28 14:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Andria Pichidi

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.