FX News Today

Asian Market Wrap: 20-year Treasury yields are up 0.4 bp at 2.943%, the 10-year JGB yield underperformed and climbed 1.0 bp to 1.03% as stock markets moved mostly higher across Asia, with trade quieter than usual as the summer lull sets in. Bourses in mainland China outperformed and the CSI 300 rose 1.64%. Nikkei managed gains of 0.65%, despite a stronger Yen, which was underpinned by a Reuters report suggesting BoJ had considered hiking rates this year. Earnings reports and a higher Oil prices had already underpinned a higher close in the US and the positive mood spilled over into the Asian session, although trade jitters and geopolitical concerns continue to lurk in the background. Meanwhile, the ASX underperformed and lost -0.42% despite RBA held its interest rate steady once again while maintaining a tightening bias, although with the inflation forecast cut slightly, RBA is expected to remain on hold well into next year. US stock futures are moving higher and the WTI future is also up with the September contract trading slightly above USD 69 per barrel.

RBA left the cash rate unchanged but tweaked the inflation outlook. The decision to leave the cash rate at 1.50% had been widely anticipated. On inflation, RBA Governor Lowe’s statement said that CPI is likely to be lower than previously expected in 2018, at 1.75%, below the 2%-3% target band, but at the same time inflation is seen rising more than previously forecast in 2019 and 2020. RBA said that it expects GDP growth to average a little more than 3% in 2018 and 2019. It stated that the unchanged policy is consistent with meeting the CPI target over time. Slower Chinese growth was noted. Market focus will now turn to upcoming release of the Statement on Monetary Policy (SMP), this Friday, for details on the forecast tweaks. The Australian Dollar initially dipped on Lowe’s statement before more than reversing the losses.

Charts of the Day

Main Macro Events Today

- Canadian Ivey PMI – Expectations – It is expected at 64.2, higher from 63.1 in June.

- US JOLTS & Consumer Credit – Expectations – Job openings anticipated to rise slightly at 6.74M in June, while Consumer credit is expected to rise $16.0 bln in June, following a $24.6 bln surge in May.

- NZ GDT Price Index

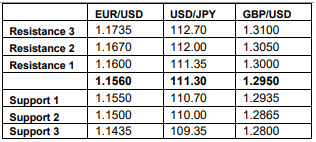

Support and Resistance levels

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/08/07 14:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Andria Pichidi

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.