FX News Today

Asian Market Wrap: Yields continued to move higher during the Asian session, confirming that reports of policy tweaks at the BoJ have reminded traders that major central banks remain on course to take out more stimulus. 10-year JGBs yields initially corrected some of yesterday’s gains but recovered losses during the later part of the session, and yields mostly moved higher elsewhere in Asia as stock markets rallied. 10-year Treasury yields by contrast fell back from earlier highs and are down -0.6 bp at 2.949%. The 10-year JGB yield is now up 0.3 bp at 0.077%. 10-year yields rose 3.3 bp in China as the Yuan fell sharply amid signs that China is shifting towards monetary expansion, as the government presented measures designed to boost domestic demand. Still, while this may be a reaction to signs that the trade war will worsen the economic slowdown, the slip in the Yuan also adds to risks that the trade war will turn into a currency war. For now though it has put a fire under Chinese equities in particular while rising yields aided financial companies. The CSI is up 1.55%, the Hang Seng gained 1.42%, and Topix and Nikkei are up 0.48% and 0.52% respectively. The ASX is also up 0.58%. US Stock futures are equally moving higher.

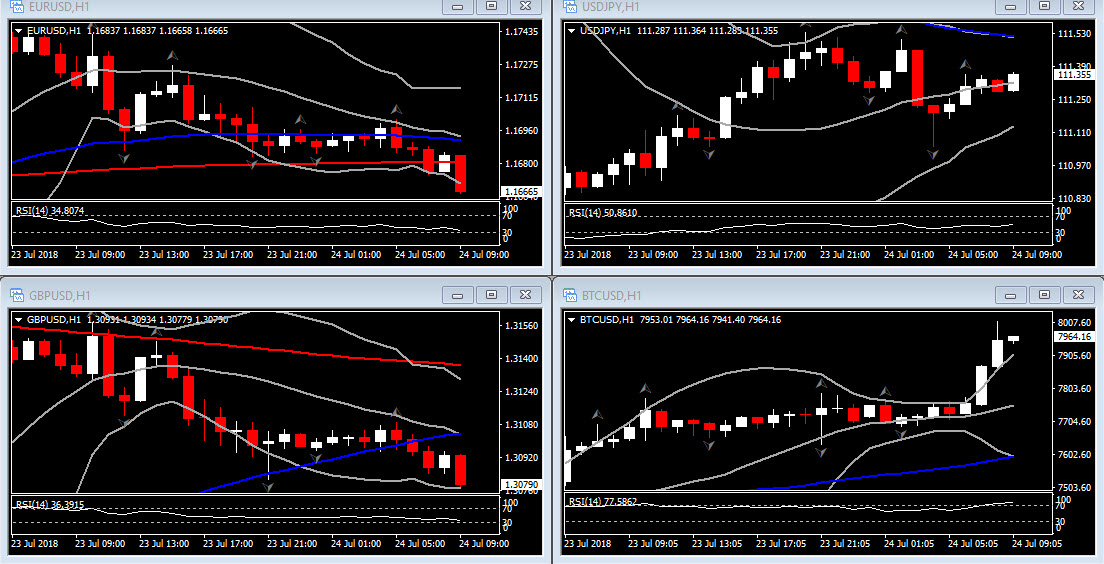

FX Update: The Dollar is showing modest gains versus most currencies heading into the London interbank open, underpinned by the further rise in US 10-year T-note yield yesterday, which lifted to 5-week highs, pushing towards the 3.0% level again amid market speculation that Friday’s advance US Q2 GDP report will top the median forecast for 4.1% y/y growth. The USD index (DXY) lifted to two-session highs, while EURUSD printed a two-session low of 1.1666. USDJPY, in contrast, has traded with little direction in the lower 111.0s after yesterday printing a 3-day low at 110.75. Japanese exporters were reported buying Yen during the early part of the Tokyo session today, which contributed to driving USDJPY to an intraday low of 111.06. The pair subsequently lifted back some amid a backdrop of rallying stock markets in Asia, led by Chinese bourses on reports that Beijing will adopt a more “vigorous” fiscal policy, including corporate tax cuts.

Charts of the Day

Main Macro Events Today

- German Markit PMI – Expectations – The Manufacturing PMI is seen falling to 55.5 from 55.9, and the services reading to 54.3 from 54.5

- Eurozone July PMIs – Expectations –The EMU Manufacturing PMI is seen falling to 54.6 from 54.9, and the services reading to 55.0 from 55.2.

- US Housing Price Index, Markit PMIs & Richmond Manufacturing Index – Expectations – FHFA home prices are forecast to rise to 264.1 in May from 262.5. Also the Markit flash PMIs are on tap, along with the Richmond Fed index seen dipping to 17 in July from 20.

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/07/24 14:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Andria Pichidi

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.