FX News Today

Asian Market Wrap: Treasury yields moved back up from lows, 10-year JGBs are also slightly higher as the stock sell off started to fade during the Asian session. 10-year Treasury yields are now up 0.5 bp on the day at 2.886% and 10-year JGB yields are up 0.7 bp at 0.026%. The escalating round of trade and investment restrictions continue to hang over markets, but at least for now investors seem to be taking a breather. Japanese stock markets reversed early losses as gains in banks offset declines in technology and telecoms. Topix and Nikkei are up 0.25% and 0.12% respectively. The Hang Seng gained 0.21% and while the CSI 300 is still down -0.57%, the Shenzen Comp is up 0.66%. US stock futures are also moving higher after sharp losses on Wall Street yesterday. Oil prices are up and the WTI is trading at USD 68.30 per barrel.

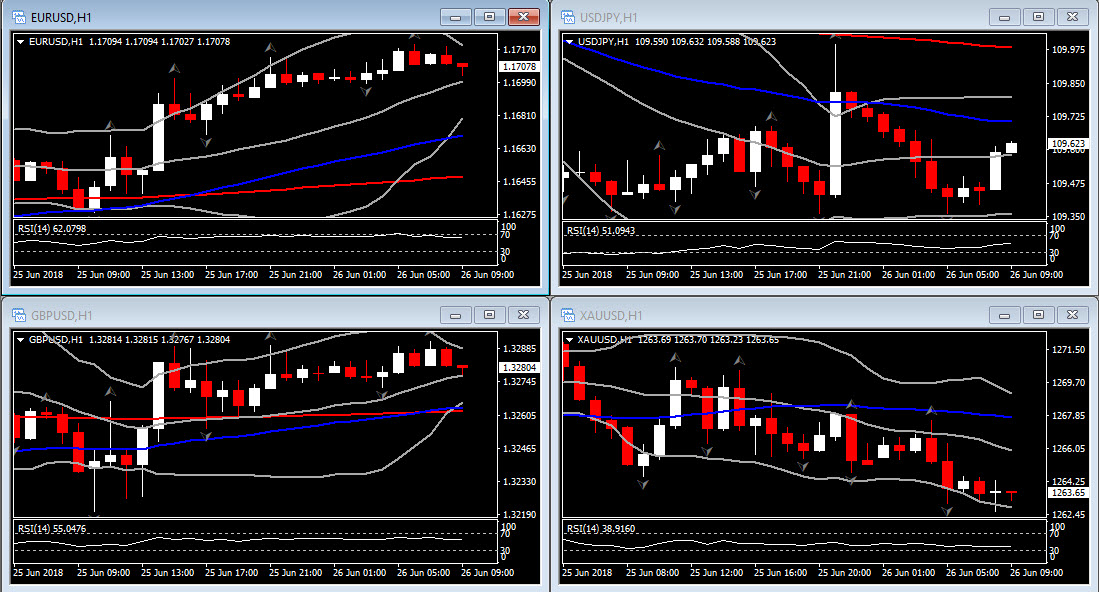

FX Update: The main currencies are showing little net change ahead of the London interbank open. EURUSD edged a fresh 12-day high, at 1.1721, before ebbing back to near net unchanged levels nearer 1.1700. USDJPY has become directionally stuck near 109.50, above the 2-week low that was pegged yesterday at 109.37. The yen’s safe-haven bid of yesterday ran out of puff, while BoJ board member Sakurai said, also yesterday, (from Rome) that it remained “essential” for the central bank to conduct monetary policy “under the current framework for the time being.” By “current framework” he meant a short-time interest rate target of -0.1% and pegging of the 10-year JGB yield at near 0% (the curve control policy), alongside its QQE program. The stock market sell-off has abated in Asia. Japan’s Nikkei 225 managed to close with a fractional 0.2% gain, while S&P 500 futures are showing modest gains. President Trump’s trade advisor Navarro said that the Trump administration just wants “free, fair, and reciprocal trade…the mission here is to defend our technology and IP.”

Charts of the Day

Main Macro Events Today

- MPC Member Haskel and McCafferty Speech

- US CB Consumer Confidence – Expectations – to inch up to 128.5 in June, from 128.0 in May and close to a 17-year high of 130.0 in February. Additionally, S&P Case-Shiller home prices are seen rising to 211.2 in April from 208.0, while the Richmond Fed index may dip to 15 in June from 16.

- FOMC Member Bostic and Kaplan Speech

- NZ Trade Balance – Expectations – is seen narrowing to NZD100 mln in May from NZD263 mln in April.

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/06/26 14:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Andria Pichidi

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.