EURUSD, H1

Eurozone HICP inflation hit 3% in August, up from 2.2% y/y in the previous month and indeed a much higher number than anticipated. Excluding energy, prices lifted 1.7% y/y, after 0.9 y/y in July, while core inflation moved up to 1.6% y/y from 0.7% y/y. The highest annual rate in nearly 10 years, but much of the overshoot remains due to special factors, not just from energy prices, but also Germany’s temporary cut to the VAT rate last year and other virus related effects, including global supply chain disruptions, which have added to a mismatch between supply and demand that is likely to be temporary. The annual rate is expected to decelerate again, but against the background of the inflation jump and with activity expected to reach pre-crisis levels a tad earlier than initially anticipated, expectations are that the central bank to at least start taking the foot off the accelerator and scale back monthly purchase levels slightly.

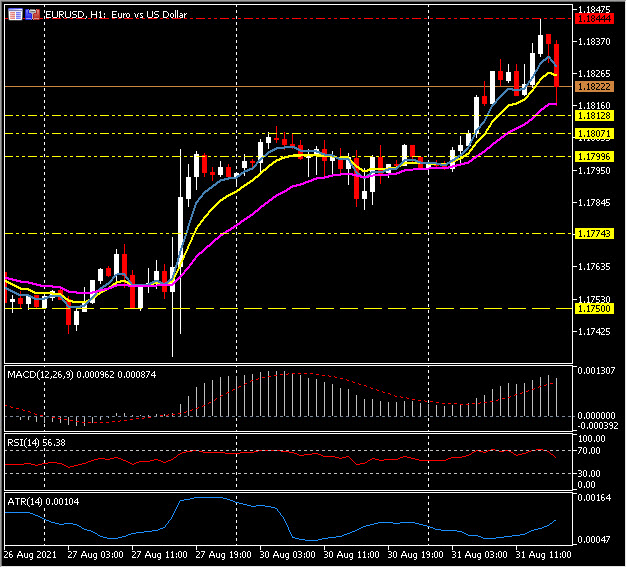

EURUSD printed a 25-day high at 1.1844 and Cable made a two-week high at 1.3801 before reversing to 1.1820 and 1.3775 currently. This has come with the US T-note yield versus Bund yield differential narrowing by about 2 bp this week, even despite the advent of perky August inflation data out of the Eurozone.

The combination of buoyant global asset markets and an accommodative Fed is a Dollar negative circumstance. Fed Chairman Powell, to recap, refrained from signalling a policy tapering schedule at the keynote Jackson Hole address last Friday. While still acknowledging tapering could be “appropriate” this year, Powell downplayed the risks of inflation, seemingly pushing back against the increasingly vocal hawks who had been out in force last week. In the Eurozone, preliminary August inflation readings out of France, Spain and Germany have shown a renewed pick up in headline rates. ECB’s Villeroy yesterday stressed that there are no signs of underlying inflation running hot while dismissing price spikes as being temporary, though data will still support the more hawkish board members and fits our view that the ECB will scale back monthly QE purchase levels slightly at its September policy meeting before discussing the future of the emergency PEPP program at its December review. We still see longer-term risks remaining to the downside for EURUSD, given the favourable expected US growth rate and the associated larger fiscal stimulus levels compared to the Eurozone.

Canada’s GDP rose 0.7% in June following the -0.5% decline in May, in line with expectations. Statistics Canada’s preliminary estimate is for a 0.4% drop in July GDP. The separate Q2 GDP measure fell -1.1%, missing expectations, after a 5.5% growth pace in Q1. Consumption in Q2 rose 0.2% from a revised 2.6%. A lot of the weakness was in business fixed investment, which declined -2.2% after the 18.7% rate of growth in Q1, with residential structures contracting -12.4% versus the 42.1% Q1 surge. Exports of goods and services shrank -15.0% from the prior 6.0% (was 3.3%) gain.

USDCAD rallied to 1.2612 from near 1.2580 following the big miss in Canada Q2 GDP; the pairing had traded to a two-week low of 1.2569 earlier. EURCAD touched a 4-day high at 1.4925 up a single tick shy of a whole number from yesterday’s 5-day low at 1.4826.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.