FX News Today

European Fixed Income Outlook: The 10-year Bund yield is down -0.8 bp at 0.484% in early trade, amid a broad dip in Eurozone long yields and in tandem with a -1.5 bp decline in 10-year JGB yields. The start of the new quarter didn’t bring an improvement in stock market sentiment and Eurozone stock futures are selling off in catch up trade, after the long Easter weekend and a fresh sell off on Wall Street yesterday that saw the NASDAQ closing with a loss of -2.74%. Asian markets also corrected further overnight, albeit less so. Treasuries are also underperforming today and the 10-year up 1.1 bp on the day at 2.741%. German retail sales at the start of the session unexpectedly declined and manufacturing PMIs out of the Eurozone and the U.K. are also expected to show waning confidence, thus adding to concerns that the recovery is fizzling out.

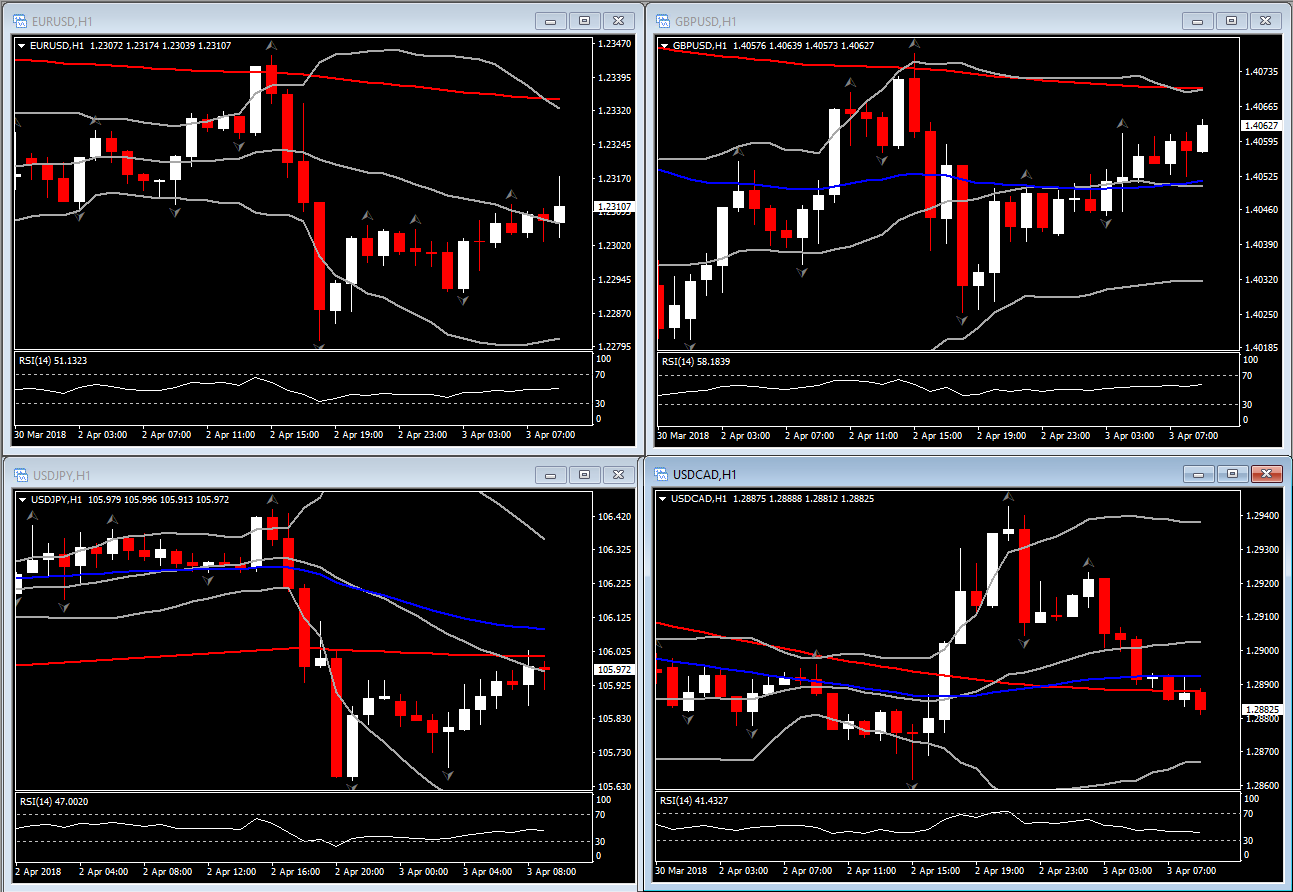

FX Update: The dollar majors continued to ply narrow ranges as markets returned to full force following the long weekend in European and elsewhere. EURUSD continued in a narrow range around the 1.2300 mark, and has been unmoved by unexpected weakness in German retail sales data. USDJPY lifted to a intraday high of 106.03 amid general, albeit moderate, yen softness, which occurred as stock markets in Asia pared intraday losses. This put in a little space from yesterday’s low at 105.66. Data and news developments were thin on the ground in Asia today, while market participants remain weary about trade wars and tech sector woes. All three of the major U.S. indices yesterday closed more than 10% below January highs. The RBA held its cash rate on hold at 1.50%, as had been widely anticipated, and the statement didn’t bring any surprises, largely being a repeat of the last one, noting improving growth prospects but with inflation expected to remain benign and repeating the view that any appreciation in the Australian dollar would result in a slower pick up in economic activity and inflation.

Charts of the Day

Main Macro Events Today

- Eurozone manufacturing PMI – The March Eurozone manufacturing PMI is expected to be confirmed at the 56.6 preliminary report, and is down from the 60.6 December print.

- UK Manufacturing PMI – expected to come in with a headline reading of 54.7 after February’s 54.5.

- German Manufacturing PMI – expected to remain unchanged at 58.4.

- Fedspeeches – The dove Kashkari will be at a regional economic forum, while Governor Brainard speaks on financial stability.

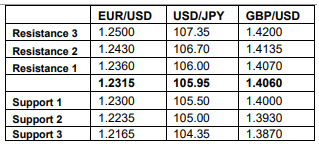

Support and Resistance level

Click here to access the HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE! The next webinar will start in:

[ujicountdown id=”Next Webinar” expire=”2018/04/03 11:00″ hide=”true” url=”” subscr=”” recurring=”” rectype=”second” repeats=””]

Andria Pichidi

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.