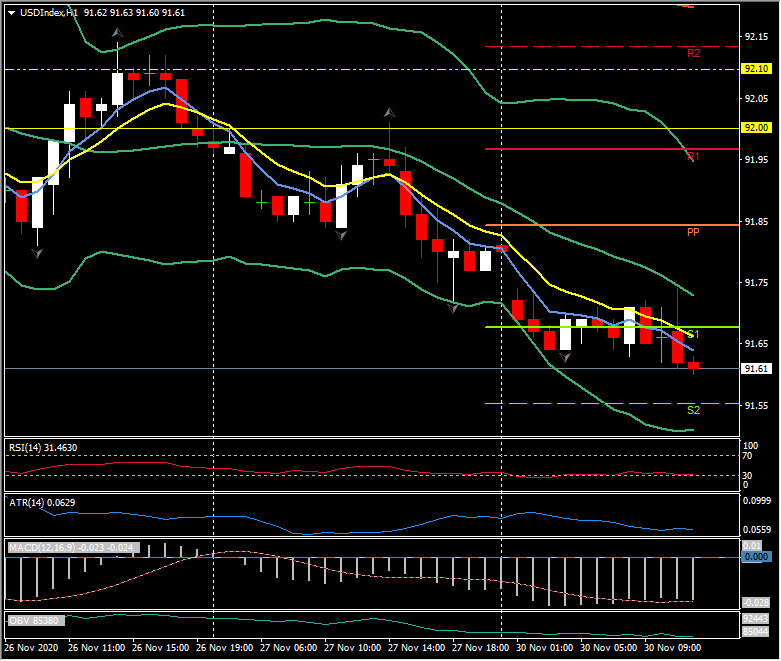

USDIndex, Daily

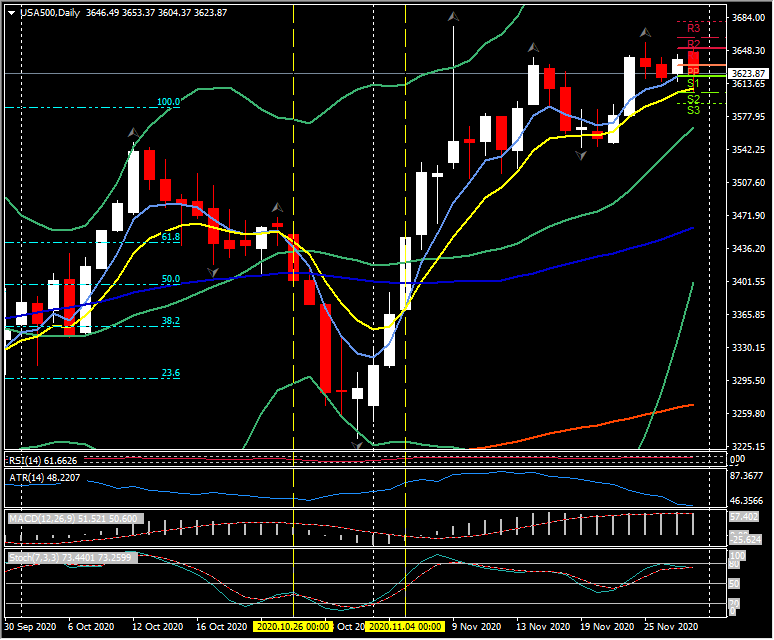

The DXY dollar index edged out a 32-month low at 91.66, and is set to close out November with its second biggest monthly loss in almost two years. The decline has run in parallel with the vaccine-optimism rally in global asset markets, which catalysed a rotation in cyclical stocks and industrial commodities. The MSCI World Index is set for a record gain in November. Many European equity markets are also set to rack November up as a record month of gains, with Italy’s MIB up nearly 26% and France’s CAC up 21%, beating even Japan’s Nikkei, which closed out the month of November earlier with a net 15% advance. High tech stay-at-home growth stocks, after surging for much of the year, underperformed. The Nasdaq is up 11% in November, while the FAANG stocks are up by less than 7%.

Sovereign bond yields have perked up, and would ‘normally’ be a lot higher if not for being reined in by central bank asset purchase programs. While stock markets have turned lower today, copper futures have still rallied to a fresh seven-year high, while aluminium prices posted a new two-year high, and zinc an 18-month peak. This came with China’s official manufacturing and non-manufacturing PMI for November coming in above expectations at 52.1 and 56.4, respectively, with both rising on the October readings. The manufacturing figure was at its highest since September 2017 while the non-manufacturing number was the best level seen since July 2012, highlighting the strong recovery in the Chinese economy from the Covid pandemic lows.

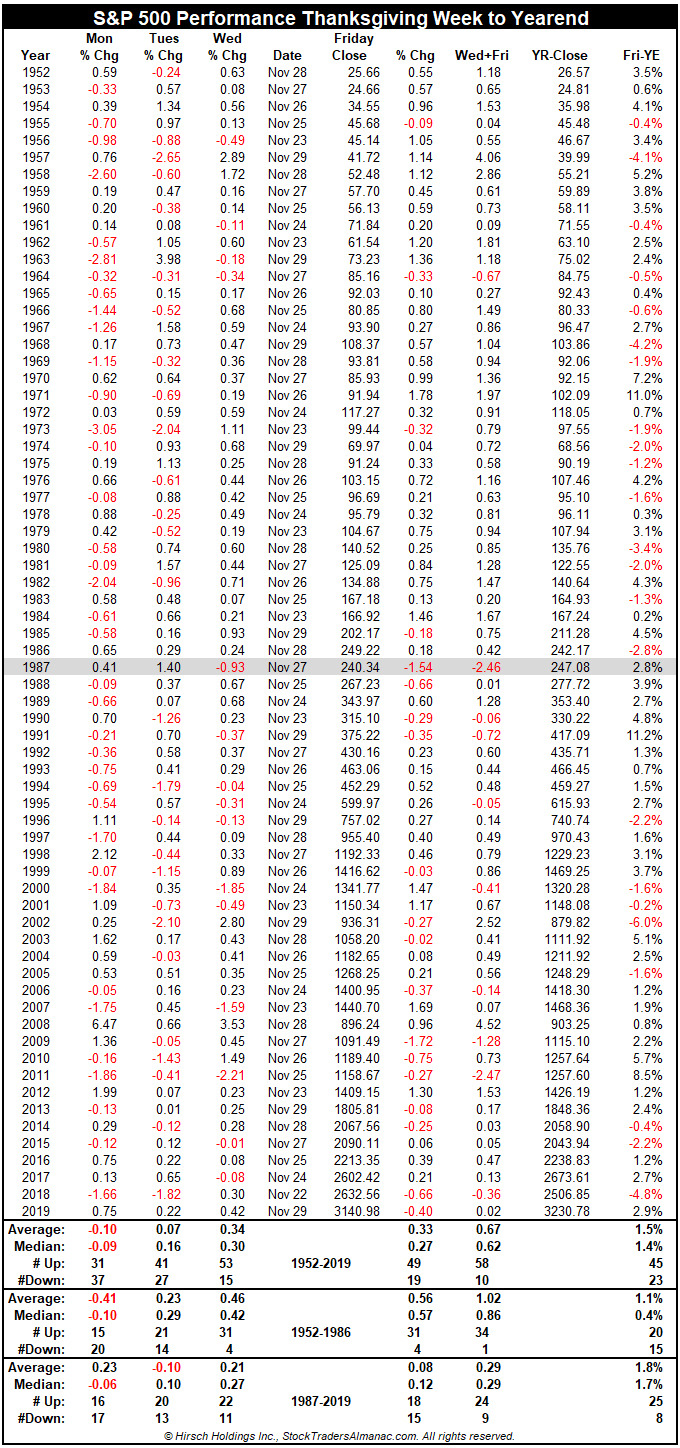

Ahead in December, there is potential for a pause in the global asset rally, with the latest BoA global fund managers’ survey finding that cash holdings at fund managers are now down to pre-pandemic levels. December has a reputation for being a down month, too, due to year-end capital tax gains (although this pattern hasn’t held up too well in recent years, with 25 of the last 33 seeing a positive yearend compared with the Friday after Thanksgiving).

A sharp focus remains on Brexit. The UK foreign secretary said on Sunday that the EU and UK are entering the “last week or so” of substantive negotiations, and that a deal was in “touching distance.” Fishing remains a key sticking point, though France’s insistence that the current arrangement remains in place, which gives the UK only 18% of the catch from its own waters, is seen as unreasonable by the UK, naturally, but also many other EU states.

Click here to access the Economic Calendar

Stuart Cowell

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.