There’s a big risk-off trade in the market that has sent equities sharply lower. European bourses have dropped over -3% while US equity futures are down more than -1%. Asian shares are all in the red, though Japan was on holiday. Bonds are firming on the flight out of stocks with longer dated Treasury rates about 5 bps richer.

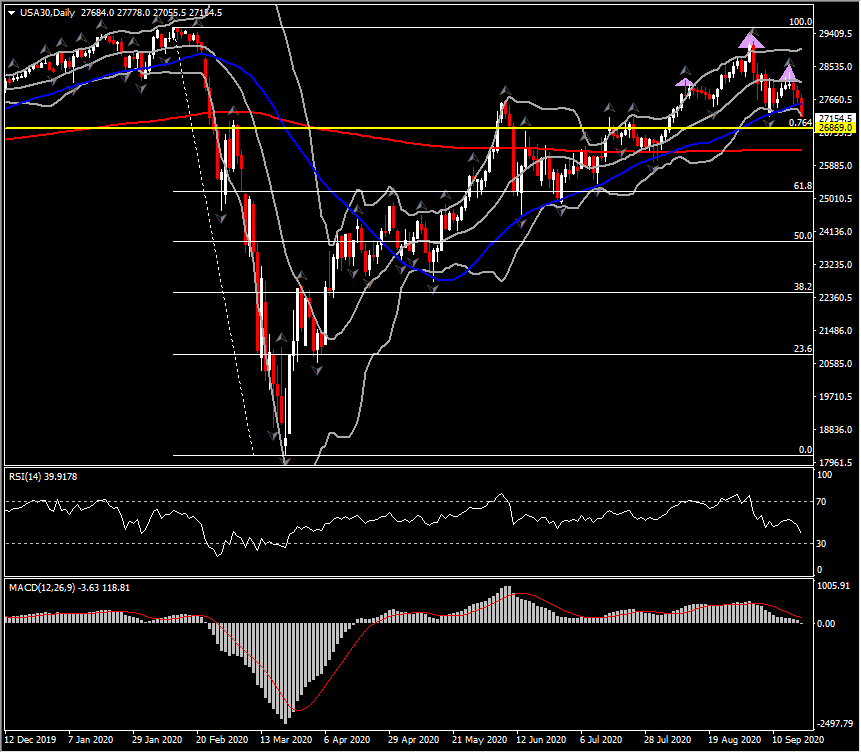

A resurgence of the virus across Europe has revived worries over a tightening of virus restrictions. An already very contentious US election was thrown for a tailspin with the passing of Justice Ginsberg, amid ongoing disappointment over a lack of more fiscal stimulus. US equity futures have tumbled as risk appetite has been undercut by a variety of factors. The USA30 has sunk -2.1%, the USA500 has lost -1.7% and the USA100 has fallen -1.5% in pre-market futures trading.

Pressures on bank stocks in Europe added to the weakness in equities after a report over the weekend by the International Consortium of Investigative Journalists of an investigation that found banks moved money for people and entities they could not identify. The report alleges banks in many cases failed to file the required suspicious activity reports until years afterwards. HSBC, Standard Chartered, Deutsche Bank and Barlays are all underperforming in an overall weaker market, with GER30 and UK100 down -2.99% and -3.16% respectively with fears about the impact of resurging virus cases adding to the risk off backdrop this morning.

GER30 has declined significantly, breaking the 50-day SMA that has been supporting the asset since May, but also the upwards regression channel since since end of July. The odds of further drift rising as daily Bollinger bands pattern are getting wider. The breakout of September Support around 12,745 added an increasing pressure. Given the bull rejection last week at 13,390 area, a close today below 50-DMA and outside Bollinger’s would mean a reversal of 6-week gains. Meanwhile a breach of the 12,500 level would imply around -5,563 ticks from this week open, something that could suggest the risk of the first significant correction since the massive recovery kicked off back in March. This would certainly bring the Key June lows of 11,600-11,940 back into play. Only above 13,100 (20-day MA) could averts the potential decline.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.