A a no-deal Brexit outcome is now a much greater risk.

The London Times have reported that senior members of Prime Minister Johnson’s party are warning him about the risks of a no-deal exit from the EU’s single market, and that the plan to unilaterally dilute the Withdrawal Agreement is a risky move. Johnson’s move may be tactical, aimed at turning a weak negotiating position into a strong one before political leaders become involved in the Brexit endgame, which is set to happen between now and the EU leaders’ summit in October.

But, the view that Johnson’s cabinet are Brexit ideologues, and are serious about blowing up trade talks and prepared to exit the single market at year-end without a deal, is now much strengthened. As Robert Peston, a generally well regarded ITV political journalist, puts it in an opinion piece, the real reason Johnson’s government is sacrificing the prospect of a trade deal boils down to the desire to subsidise British industry — to “have the discretion to invest without fetter in hi-tech, digital, artificial intelligence and the full gamut of the so-called fourth industrial revolution.”

The Brussels position is that the UK can only have a trade deal if it adheres to the EU’s state aid regime, or at the least follow very similar rules, which constrains governments from subsidizing industry to prevent unfair competition. The Internal Market Bill, which is the legislation that will unilaterally unpick parts of the Withdrawal Agreement, published by the government today, is specifically designed to enhance the UK’s state aid autonomy rather than constrain in.

This fits the Singapore model that has been must touted by Johnson and his allies during the Brexit debate.

The UK government knows full well the impact that this will have in relations with Brussels. EU Commission President von der Leyen in a tweet this week stressed that the Withdrawal Agreement is “an obligation under international law and prerequisite for any future partnership.” A senior minister admitted yesterday that the Bill breaks international law, while the head of the UK government’s legal department quit in disgust. This proposed legislation has greatly raised the odds for the UK leaving the EU’s single market without a new deal.

The Internal Market Bill, coupled with a finance bill planned for later in the year, will give ministers the power to tweak protocols that affect Northern Ireland trade with the rest of the UK, and will also enhance the UK’s state aid autonomy — which is be inharmonious with the EU’s regime for limited state aid. This has put the UK on a crash course with Brussels.

The Pound is likely to drop much further than it already has if markets see the odds of a no-deal Brexit getting much greater than before. Leaving the frictionless trade of the single market without a mitigating trade deal means UK trade shifting to much less favourable WTO terms (think tax and regulatory friction). The UK won’t just be leaving the common market, but also the 40 trade agreements the EU has with global economies.

Additionally, the continued ramping up in coronavirus testing in the UK, meanwhile, is producing a noisy surge in positive results. The shear volume in testing means that even a 1% rate of false positives may be producing scary looking 1,800 new “cases” per day. Along with the approach of winter, the ‘case-demic’ — rising numbers of positive tests in juxtaposition to a lack of corresponding rises in hospitalisations/deaths (which was seen in the 2009 swine flu episode) — is maintaining the media-driven coronavirus psychosis.

The economic impact of this should not be underestimated.

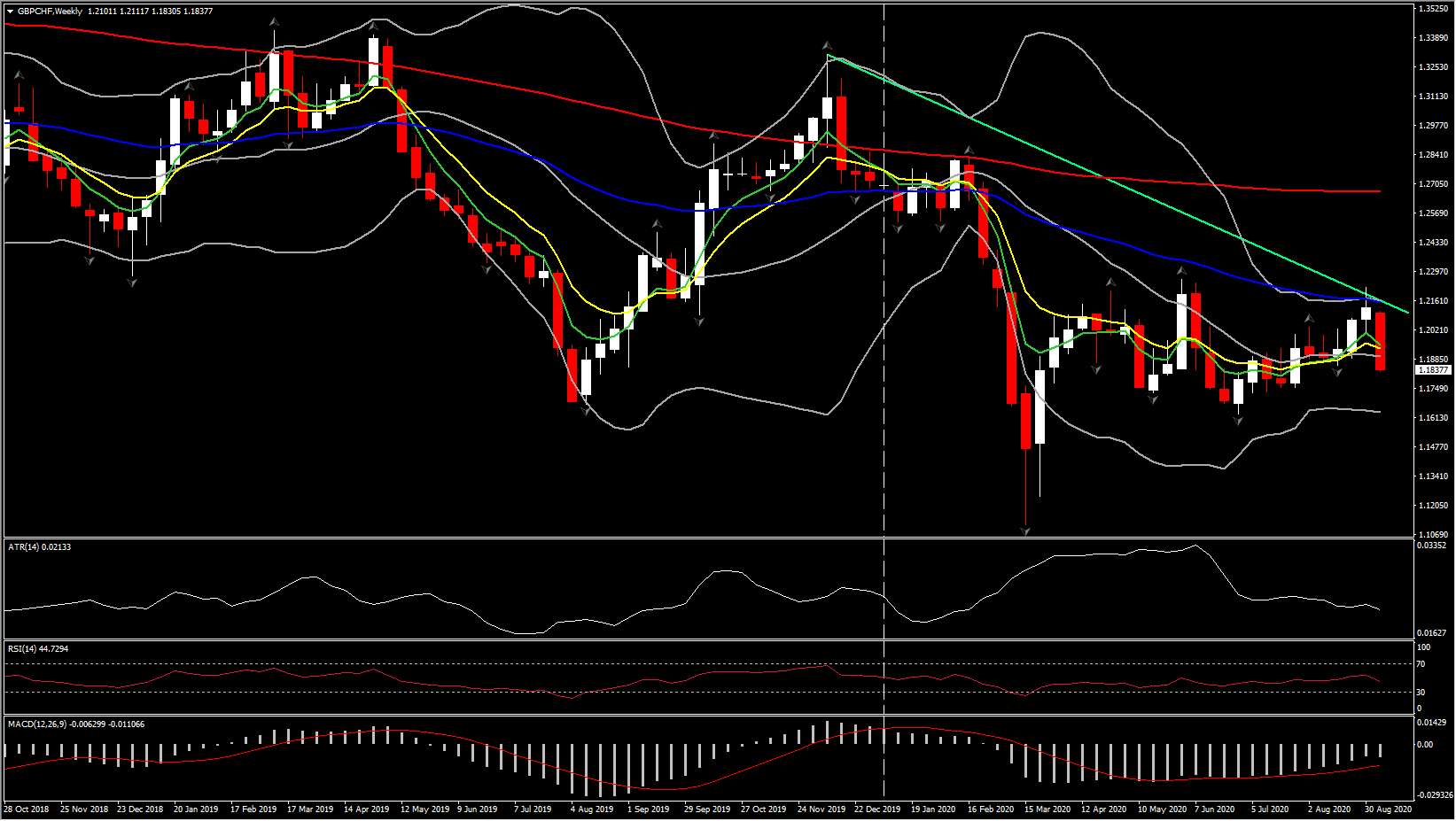

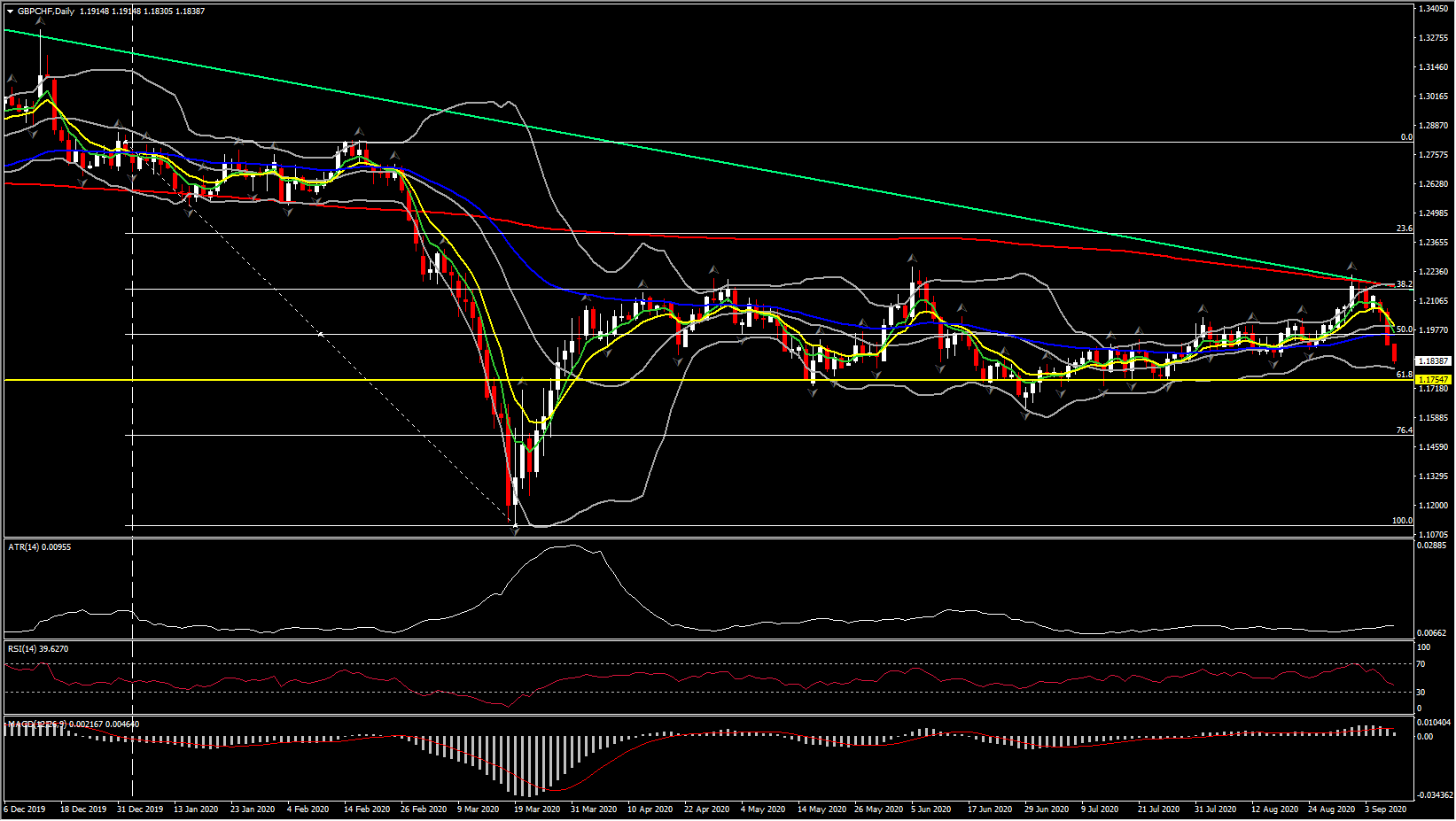

Gatherings of more than six people are now being banned in the UK. Currently however, Sterling has hit fresh 6-week lows against the Dollar, Euro and Yen. The low in Cable is 1.2883, which marks a 4%-plus decline from the last week’s nine-month high at 1.3484. However the biggest underperformer this year is the GBPCHF , with a dive up to 7.6%. This selling pressure came coincided with a strong risk-off vibe in global markets as big tech and energy stocks suffer significant losses, affected by unrealistic tech valuations and plunge in oil prices.

Meanwhile, the Swiss Franc, an historic low-beta safe-haven currency, periodically correlatives inversely with global stock market direction, along with sentiment about the EU (Switzerland’s biggest trading partner). Hence the GBPCHF move has retreated from 200-DMA down to 1.1800 area, breaking the key support band 1.1850-1.1900 and the 50% Fib level from 2020 downleg, with further downside today.

Momentum is increasingly corrective, with RSI into the 40s, whilst MACD accelerates below its signal line. The inference is that near and medium term negative bias is increasing. A closing breach of 1.1850 would imply further downside towards a previous breakout Support at 61.8% Fib. level, i.e. at 1.1755. If latter rejected, the next Support level comes to the lows 1.16s.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.