GOOGLE and AMAZON

Amazon

Corporate earnings and concerns about the impact of new localized lockdown measures due to spikes in coronavirus infections, alongside geopolitical tensions, have been in the mix for nearly a month. Markets remained and will remain glued for the rest of the week to the ongoing stream of earnings reports, as some of the tech giants are reporting today. Yesterday the Tech leaders testified in Washington with the CEOs of Amazon, Apple, Alphabet and Facebook appearing together before Congress for the first time, after 13 months of investigation by lawmakers into the market power of Big Tech .

Even though the testimony is crucial, the earnings releases for the Q2 of 2020 will likely dominate the market. All four companies’ earnings reports are due to come out today after the US market close, who together have a market capitalization value of almost $5 trillion. Amazon, however, is the company that is expected to experience a big surprise in its Earnings Per Share (EPS) as the Surprise Prediction tool has posted a +107.82% increase recently on the expected EPS after an estimate revision from Zacks. In fact, Zacks’s Most Accurate Estimate tool for the current quarter is currently at $3.64 per share for Amazon, compared to a broader Zacks Consensus Estimate of $1.75 per share. This suggests that analysts have very recently bumped up their estimates for Amazon, giving the stock a Zacks Earnings ESP (Surprise Prediction tool) of +107.82%. According to Refinitiv, Amazon is expected to post a revenue of $81.6 billion, which reflects an increase of more than 14% on revenue on a quarter-over-quarter basis.

Despite lockdowns due to pandemic there are a number of factors in favor of Amazon in Q2. The company’s retail sales strategies were very efficient, with huge investments in its infrastructure, something that could prove profitable in this earning report but also the future ones.

In general however, ecommerce firms (i.e Ebay, Amazon etc) have likely benefited the most from the “stay at home” measures and the closure of retail stores, as a more than 78% spike in online shopping was identified in May. According to Adobe Analytics the pandemic led to $52 billion in extra online spending, based on actual spend versus prior projections, while May generated $82.5 billion in total online spending, with ecommerce shopping levels tracking above the heavy spending period of November and December 2019. Online shopping in the future could be adopted as the “new normal”.

Additionally, ecommerce demand boosted Amazon in growing its advertising platform and benefiting from advertisements, something that could add up to a strong Q2 and a strong 2020 in general. Especially after the advertising boycott against Facebook that started in July. ( The widely publicized advertiser boycott against Facebook has less than a week to show it has become a global coalition solid enough, and strong enough, to take on the social media giant.)

Even though the pandemic caused a spike in Amazon’s customers while other businesses either closed or struggled to stay afloat, the company had to spend at huge levels in order to adjust its infrastructure according to Covid-19 restrictions. The spending is rumored to have been given for hiring, delivery infrastructure, delivery vans, safety measures, air fleet expansion for international delivery services etc. The company’s emphasis on drive-in grocery delivery, such as the AmazonFresh Pickup, and Amazon Go, its first brick-and mortar grocery store, helped in garnering a strong band of customers.

But was the spending reasonable? And how much needs to be spent to get AMAZON back to its pre-pandemic normal?

Last in my list of positive factors of potential Amazon success is of course its revenue stream which so far looks to be impressive with or without the pandemic. During the to-be-reported quarter however, the number of Prime memberships has strengthened significantly due to:

- Prime Free One Day service, Prime’s same-day service,

- AmazonFresh service,

- Two-hour delivery service of natural and organic products such as meat and seafood,

- International delivery services expansion (Amazon extended its partnership with the Air Transport Services Group (ATSG) to lease 12 additional Boeing 767-300)

- Additionally, Amazon Prime allows customers to access Prime Video, which is its streaming media service. More Prime subscriptions could be seen also due to the increase of content and the overall portfolio on Prime Video.

In summary, the concern could be only on the amount of expenses that the company paid as a response to Covid-19, and whether it significantly exceeded its latest call of $4 billion on infrastructure.

Alphabet (Google)

Alphabet Inc. is a holding company and Google’s parent company. The company’s businesses include Google Inc. (which is the largest one) and its Internet products, such as Access, Calico, CapitalG, GV, Nest, Verily, Waymo and X. The company’s segments include Google and Other Bets.

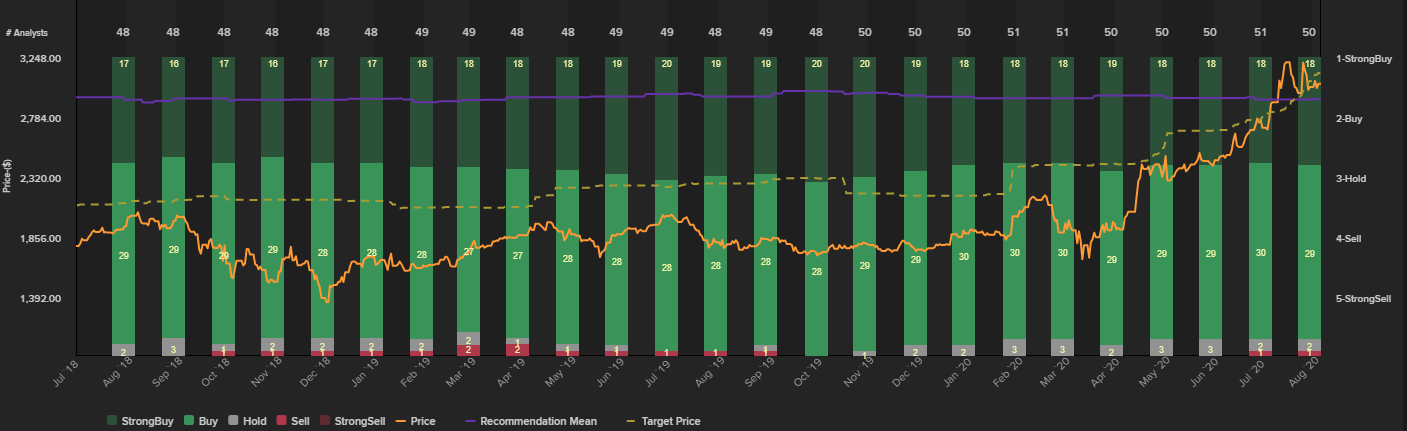

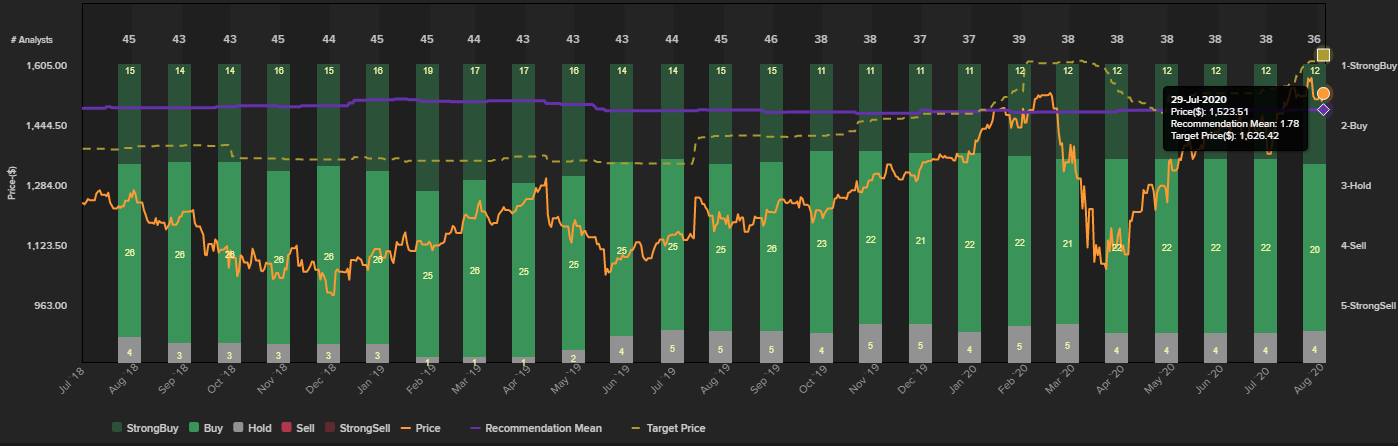

Alphabet’s second quarter earnings for 2020 will be reported along with the rest of the giants. The consensus recommendation for the company is “buy to strong buy”, corresponding to the majority of the consensus recommendation from Reuters Eikon, as 20 and 12 out of 36 analyst firms recommend “buy” and “Strong buy” respectively. Hence, no analyst firm is making a “Sell” or “underperform” recommendation for the company.

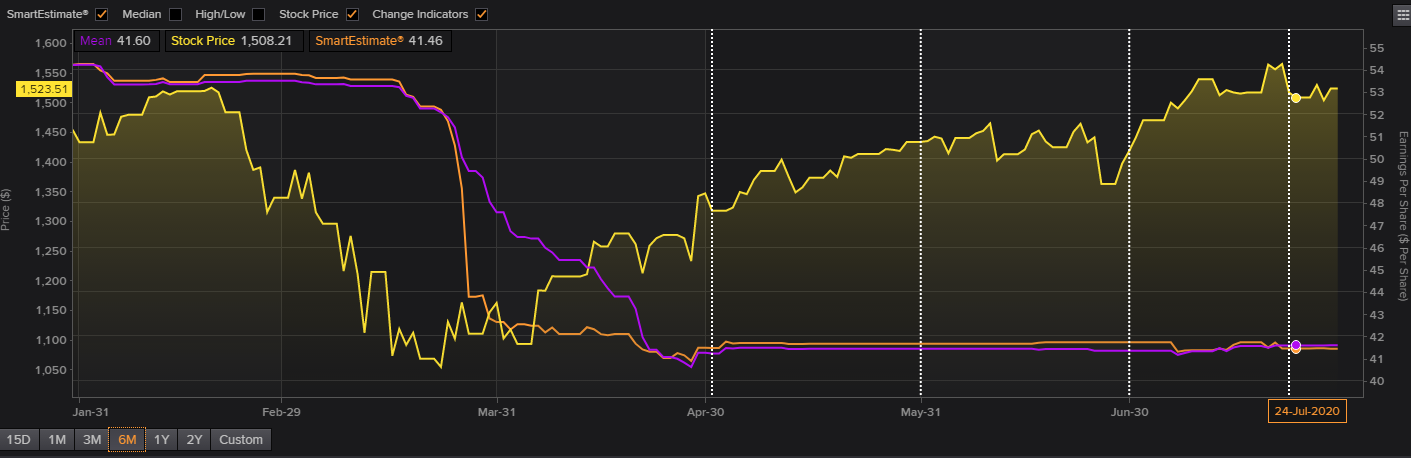

According to Zacks Investment Research and Reuters Refinitiv, the information service is expected to have $8.21 in earnings per share during the second quarter of 2020, which represents a yearly drop of 42% since the reported EPS for the fiscal quarter ending June 2019. Focus should also turn on the revenues number which is projected to hit a 46% yoy decline, to around $37.37 billion, from the $38.94 billion reported last year (and the $41.16 billion reported in the first quarter of 2020).

Alphabet has faced some serious legal difficulties during the year, with the federal government and almost every state attorney general having begun antitrust inquiries into Google. The feds are concentrating on bias in searches, on advertising and on the deployment of Google’s Android operating platform.

However, if we focus on the earnings report for Alphabet Inc, things could turn more optimistic than expected as the pandemic boosted the search giant’s quarterly profits due to a boost to the advertising sector similar to Amazon’s and due to the growing advertising boycott against Facebook. More precisely, its YouTube business is the one that is expected to strengthen the company’s financials in Q2 but also the second half of the year.

As analyst Brent Till stated: “A combination of positive pricing and demand trends, YouTube’s size and reach in connected TV (CTV) advertising, and relatively strong positioning in “brand safety” — ensuring that advertisements aren’t shown on offensive content — make YouTube an attractive place for ad buyers. A good chunk of unspent political advertising budgets should also flow to YouTube ahead of the upcoming elections. “

The new features in the advertising business by Google are the ones that are increasing momentum in this sector, i.e. Local Services ads by Google, Local Opportunity Finder, local store information, smart campaigns and Grow My Store for retailers. Google also made enormous efforts in boosting its ecommerce services as well, by launching a new voice-based grocery shopping service, which allows Google users to voice order groceries with the help of the Google Assistant.

Further spending has been seen in Google Cloud in order to expand its revenue streams beyond advertising. Google Cloud generated $8.9 billion in revenue in 2019, a 53% increase over the previous year. Despite this being a highly competitive sector – and according to Bloomberg, in May the company had to cancel part of its plans for a major new cloud service in China and other markets deemed “sensitive” over geopolitical tensions and COVID-19 concerns – it managed to expand the cloud service portfolio and data centers within Q2.

During the quarter, the company announced additional plans which could eventually positively impact the upcoming results for 2020, such as:

- $2 billion investment to build a data center in Poland, which should add efficiency to the company.

- Official long-term partnership between Google and Deutsche Bank. “The partnership will enable Deutsche Bank to accelerate its cloud transition and build on the engineering capabilities of both companies. Together with Google Cloud, Deutsche Bank will transform its IT architecture and thus generate considerable value for its clients.“

- Partnership of Waymo and Volvo for the development of a new self-driving electric vehicle for use in a ride-hailing service. This deal along with the acquisition of Latent Logic strengthened its presence in the booming self-driving vehicles market.

Hence the risks that Alphabet faces ahead of the report is the solid competition from Amazon in advertising business and cloud services but also the increasing expenses which could affect the Q2 report.

At this stage, we have to point out that the consensus recommendation, similarly to economic data forecasts, has a significant effect on the near-term stock price, as it represents a company’s wealth picture. Hence on every earning report, stock price is highly influenced by the comparison between the outcome and the expectations. The market tends to react positively if the outcome comes in better or at least in line with the forecast, while the price moves lower if the reported earnings miss expectations.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.