")

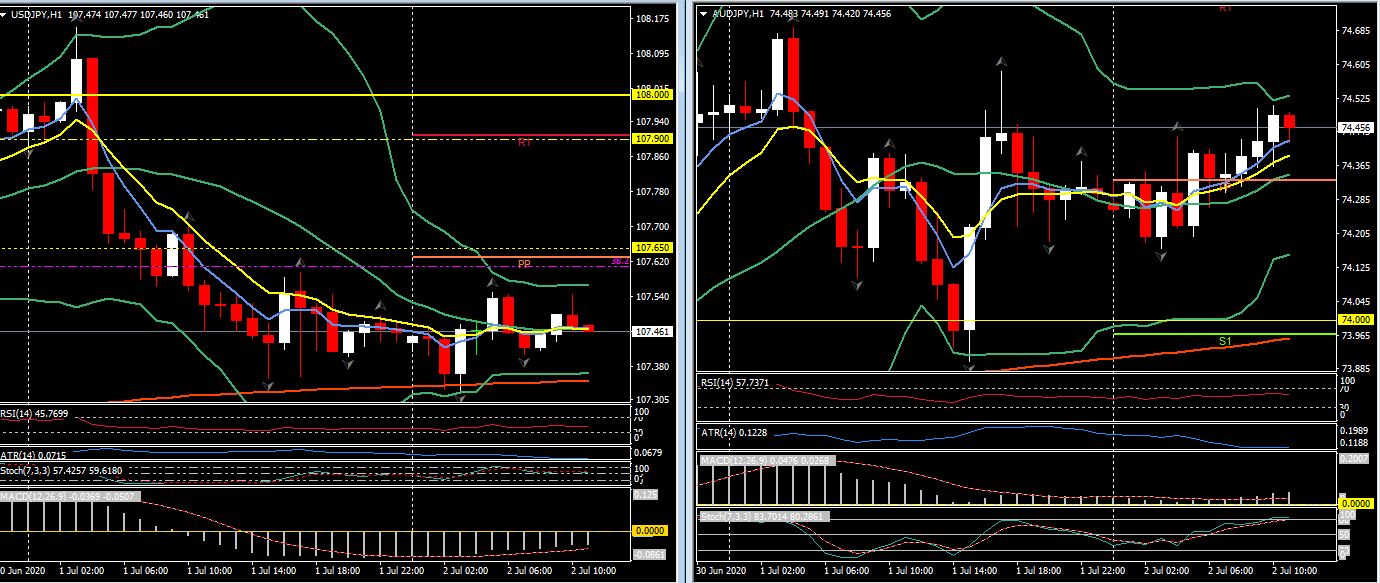

USDJPY, H1

The Dollar and Yen have traded moderately softer against most other currencies. USDJPY has settled in the low-to-mid 107.00s after dropping back from the three-week high that was seen early yesterday. Other Yen crosses, including the risk-sensitive AUDJPY cross, have seen a similar price action, with the Yen losing safe haven demand as global stock markets stage a tentative rebound on hopes about a vaccine for the coronavirus. Pfizer and Germany’s BioNTech, developing two of the 150-plus candidate vaccines, report good results in early-stage human trials.

Markets are also looking for a strong rebound in US employment in today’s June payrolls report, despite a sub-forecast rise in yesterday’s June ADP private jobs report. Consensus for the June nonfarm payroll gain is at 3.090 million, as nearly every measure of economic activity has moved notably higher since the May BLS survey week, though with disappointingly modest improvement in the initial and continuing claims figures. The jobless rate should improve to 12.3% from 13.3% in May, on the assumption that distortions from prior months are maintained at proportional levels. Expectations are for a 1.5% June hours-worked increase with a 34.5 workweek, while hourly earnings give back more of the 4.7% April pop with the shift in the composition of jobs, as more low-paid workers return to work. Assumptions are for a -1.0% decline as seen in May. There is a wide range around the headline figure with a range of 1.5 million to 7 million. The May headline overshot the median by 10,674 after a 2.213 million overshoot in April, a 601,000 undershoot in March, a 103,000 overshoot in February, and a 62,000 overshoot in January.

Markets have, however, become somewhat desensitized to good May and June data, which continue to fill out a picture of strongly rebounding economies from the April lockdown nadir. New highs in the infection rate in many states in the US, where the coronavirus is now spreading at an exponential rate in over half the country’s 50 states, and in many areas in other reopening economies, remains a concern for investors.

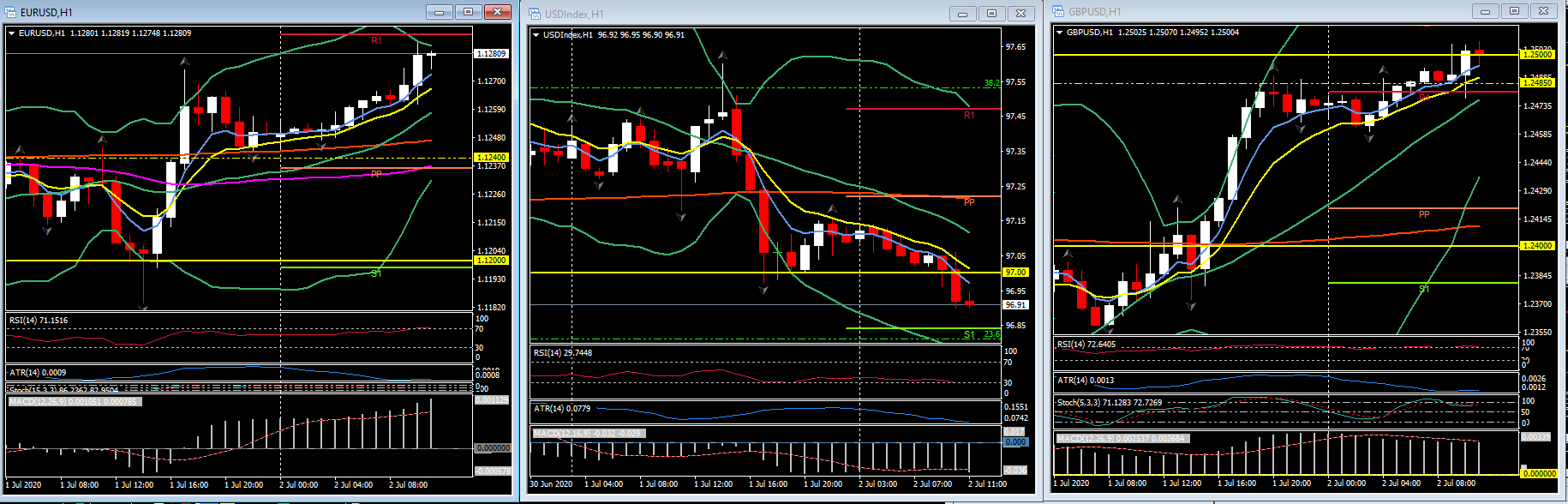

Elsewhere in the currency realm, EURUSD lifted to a 1.1280 for a new three-day peak. The narrow USDIndex (DXY) tested yesterday’s eight-day low at 97.03 and then broke below to 96.92. Cable pegged an eight-day high at 1.2506, contributing to sterling’s rebound after recent underperformance. USDCAD edged out a two-day peak at 1.3612, with the oil-correlating Canadian dollar trading softer despite the cautious risk-on backdrop in global markets. Front-month USOil prices have settling near $40.00, below the nine-day high that was seen yesterday at $40.58. Gold slipped from new 8-year highs yesterday at $1789 and trades down, pivoting around $1770 in European trading.

Join us live later today on our Facebook and YouTube channels as we analyse the NFP data and possible market scenarios.

Click here to access the HotForex Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.