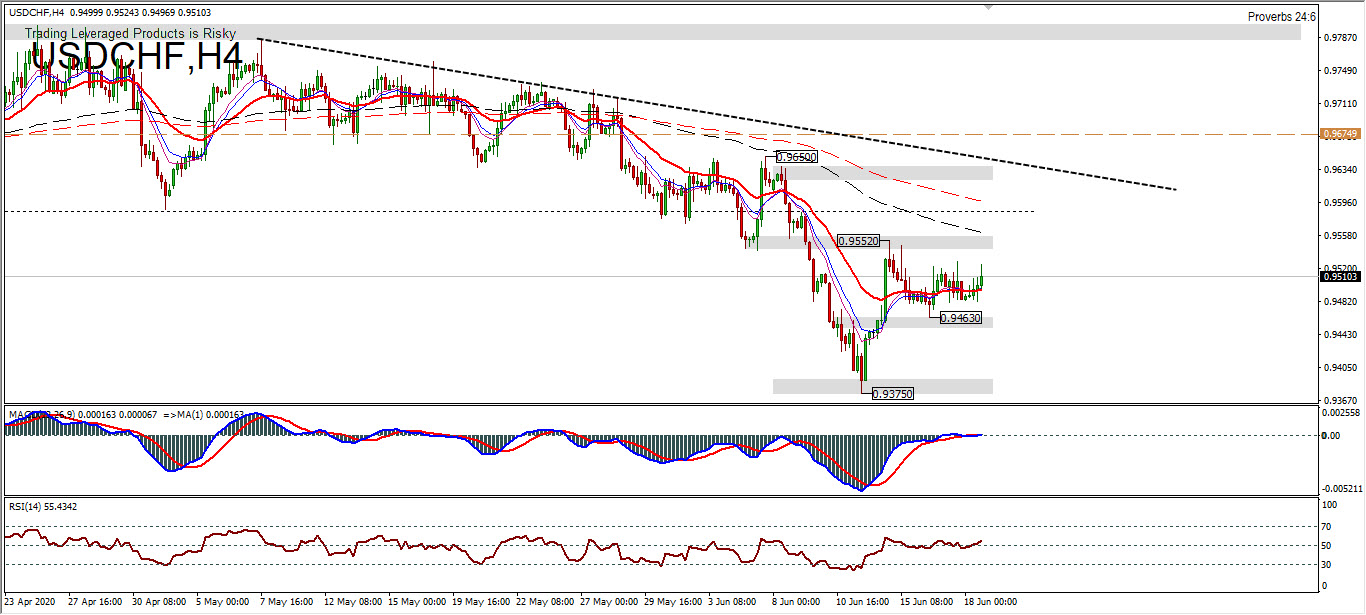

The intraday bias in USDCHF is still neutral today. On the upside, a break of 0.9552 will continue the rebound from 0.9375. A break would be sustained by testing 0.9650 resistance. While on the negative side, a break of 0.9463 will continue the decline with testing of support at 0.93750.

The price still looks sideways during the 4-day movement, with an indication that the MACD is likely to level off in the neutral zone, as well as the RSI that is leveled around the 50 level. EMA 120 and EMA 200 are still being rewarded for the pair’s rise.

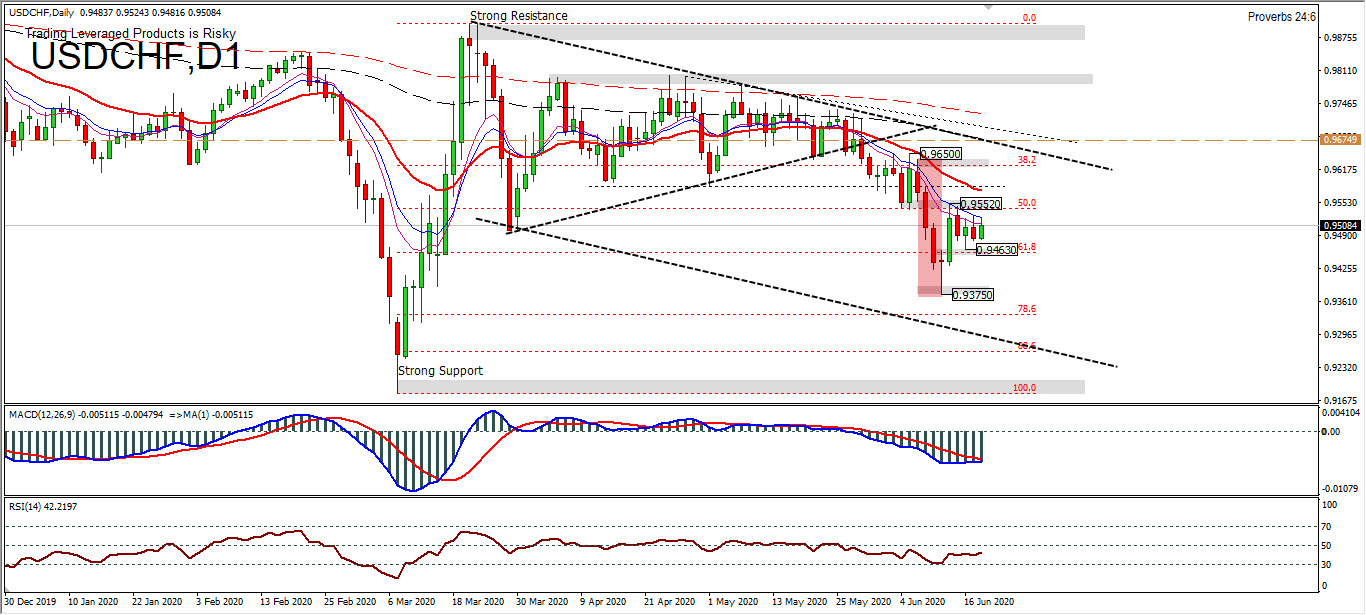

In the bigger picture, a decline that is able to pass 0.9375 will potentially equal the low position 0.9182. And a break of the strong support at 0.9182 will imply a strong downtrend as well. On the upside, the 0.9800 level becomes an important level, considering that there are reflections of the upper shadow of the past, so they are the focus of attention. If indeed the price is able to surpass it, then the test target is to equalize the high position of 0.9901 and the psychological level of 1.0000. Overall the price is still dominated by the sellers as seen from the price bias which is still below the EMA. MACD and RSI are still below the neutral zone.

If you look at the chart above, the last 3 months movement between April to June, prices are still in the range of highs and lows of the first quarter. The first quarter between Jan-Mar posted a low price of 0.9182 equaling the low price of Feb’2018 (0.9186) of only 4 pips , with a high price of 0.9900. So that the total movement reached 718 pip in the first quarter. In the second quarter, the movement reached 425 pips, at least to this day, with a low price of 0.9275 and a high price of 0.9800. You could say the recovery was sharply lower in March, the market moved choppy for 2 months until finally the pair dropped to a low of 0.9275. This decrease is certainly due to many factors, both fiscal stimulus factors and internal and external economic data.

Fundamental

Yesterday (18 June 2020), the SNB still maintained policy rates and deposit rates at -0.75%. The Franc is still highly valued, and the willingness to intervene in the foreign exchange market is still large, although not popular. The SNB is still maintaining the expansionary monetary policy of the pandemic, and the measures implemented to contain it have caused a severe decline in economic activity and a decrease in inflation both in Switzerland and abroad. However, this policy is needed to ensure that monetary conditions are as expected by the SNB.

Refinancing and Inflation

In addition, the refinancing facility (CRF) provides the banking system with additional liquidity, with the intention of supporting the supply of credit to the economy on favorable terms. The SNB’s expansive monetary policy helps stabilize economic activity and price developments in Switzerland. In the current situation, inflation and growth forecasts are still confusing in extremely high uncertainty.

The new inflation forecast is lower than March. This was mainly due to the significantly weaker growth prospects and lower oil prices. Estimates for the current year are negative (−0.7%). The inflation rate is likely to increase in 2021, but remain slightly negative (−0.2%), before returning to positive territory in 2022 (0.2%). This estimate is based on the assumption that the level of SNB policy remains at -0.75%.

GDP

The pandemic has pushed the global economy into sharp recession. Measures to contain the virus have limited production and consumption on a large scale, which has caused a severe economic downturn in many countries in Q1 2020. The decline in global GDP will likely be more visible in Q2. Unemployment has increased in many countries, with short work schemes preventing a stronger increase in Europe.

Given the declining number of infections, many countries have temporarily begun easing lockdowns. The first indication that is seen is that economic activity has increased. Further easing of these steps will likely contribute to a significant economic recovery in Q3. The SNB anticipates that further waves of infection will be successfully prevented. However, in terms of consumption and investment, demand tends to remain moderate for now. Global production capacity may be underused for some time to come and inflation is likely to remain low in most countries. This baseline scenario is subject to a high level of uncertainty, both on the top and bottom. On the one hand, waves of infection or trade tension can disrupt economic activity. On the other hand, the Swiss economy is also experiencing a sharp recession. Accordingly, most economic indicators have deteriorated dramatically in the past few months. Unemployment is increasing rapidly and consumer sentiment has fallen to record lows. Although the decline only occurred in March, GDP was 2.6% lower in Q1 2020 than in the previous quarter. The lowest point of economic activity came in April. Therefore the decline in GDP tends to be stronger in Q2.

Signals indicate that economic activity has increased again since May. This positive development is likely to continue in the coming months. However, the SNB anticipates that recovery is only partial for now and GDP will not recover as quickly as before the crisis. Overall, GDP has tended to contract around 6% this year. This will be the strongest decline since the oil crisis in the 1970s. The economic revival in the second half of this year is likely to be reflected in more positive growth in 2021.

The SNB has provided around CHF 10 billion in liquidity with an SNB policy rate of 750.75% since the launch of the CRF. The banks receive this liquidity with a COVID-19 loan guaranteed by the federal/regional government. The federal government, SNB and banks thus ensure the right supply of credit and liquidity for businesses in Switzerland.

Click here to access the HotForex Economic Calendar

Ady Phangestu

HFI Indonesia Market Analyst

Disclaimer:This material is provided as general marketing communication with the aim of information only and not as independent investment research. This communication does not contain investment advice or recommendations or requests for the purpose of buying or selling any financial instrument. All information presented is from trusted, reputable sources. All information that contains indications of past performance is not a guarantee or a reliable indicator of future performance. The user must realize that all investments in Products with Leverage have a certain degree of uncertainty and that all investments of this kind involve a high level of risk for which the obligations and responsibilities are solely borne by the user. We are not responsible for losses arising from any investment made based on information provided in this communication. Reproduction or further distribution of this communication is prohibited without our prior written permission.